UK Macro Daily(Beta Mode)

Housing Slumps, Gilts Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,348.79 | -0.84% |

| FTSE 250 | 21,556.50 | -0.40% |

| GBP/USD | 1.34 | -0.08% |

| GBP/EUR | 1.15 | +0.14% |

| GBP/JPY | 212.70 | +0.65% |

| Brent Crude | 97.03 | +2.41% |

| Gold | 4,737.20 | -0.26% |

| UK Nat Gas | 2.72 | +0.04% |

| Bitcoin | 70,972.82 | -1.35% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Halifax House Price Index Month-over-Month | 0.30 | 0.10 | -0.50 |

| Halifax House Price Index Year-over-Year | 1.20 | 1.50 | 0.80 |

| S&P Global Construction PMI | 44.50 | 43.90 | 45.60 |

| RICS House Price Balance | -12 | -18 | -23 |

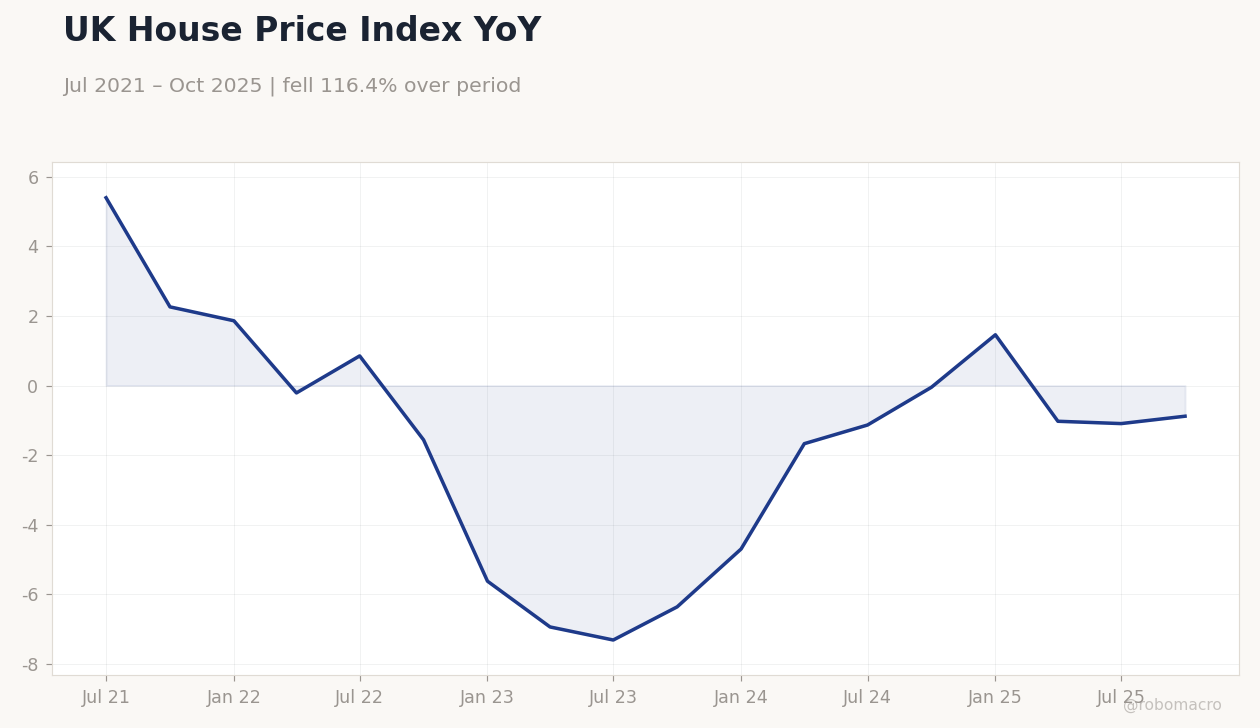

UK House Price Index YoY | Type: macro_line | House Prices Index: -0.8816 (2025-10-01) | Range: -7.308–5.391 | Trend(6pt): 5.391,0.8499,-7.308,-1.134,-1.094,-0.8816

UK House Price Index YoY | Type: macro_line | House Prices Index: -0.8816 (2025-10-01) | Range: -7.308–5.391 | Trend(6pt): 5.391,0.8499,-7.308,-1.134,-1.094,-0.8816

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK housing data disappointed with Halifax prices falling and RICS balance worsening, signaling sector weakness.

- Construction PMI beat expectations, offering some resilience amid broader slowdown fears.

- Markets reacted to global ceasefire with FTSE declines, sterling gains vs euro/yen, and lower gilt yields.

Yesterday's Recap

UK economic data released on April 8 showed mixed signals in the housing and construction sectors. The Halifax House Price Index dropped 0.5% month-over-month, missing the consensus of 0.1% and down from the previous 0.3%, while the year-over-year figure came in at 0.8% against expectations of 1.5% and prior 1.2%. The S&P Global Construction PMI rose to 45.6, beating the forecast of 43.9 and improving from 44.5, indicating a slight uptick in activity despite remaining below the expansion threshold.

The RICS House Price Balance deteriorated to -23, worse than the anticipated -18 and previous -12, highlighting ongoing pressures in the property market. Market movements reflected global influences, with the FTSE 100 closing down 0.84% at 10,348.79 and the FTSE 250 off 0.40% at 21,556.50, as investors digested ceasefire news. Sterling saw modest shifts, with GBP/USD dipping 0.08% to 1.34, GBP/EUR up 0.14% to 1.15, and GBP/JPY gaining 0.65% to 212.70.

UK 10-year gilt yields fell 0.42% to 4.43%, supporting a bond rally amid easing geopolitical tensions.

The Day Ahead

No major UK economic releases are scheduled for April 9, providing a brief respite for markets to absorb recent data and global developments. Attention may shift to any unscheduled Bank of England commentary or reactions to international events impacting sterling and gilts. Tomorrow, April 10, also lacks key data points, potentially keeping focus on broader macro themes like energy prices.

Traders should monitor sterling crosses for volatility tied to global risk sentiment. Upcoming weeks could see renewed interest in inflation indicators, given the Bank Rate's current stance at 3.73%. Overall, the quiet calendar might amplify reactions to external news flows.

Other Economic Notes

Broader UK economic themes point to persistent challenges in the housing sector, exacerbated by mortgage pressures amid expectations of sustained Bank of England rates. With unemployment at 5.20% as of November 2025, labor market softness could weigh on consumer spending and growth prospects. Energy costs remain a wildcard, influencing inflation trajectories despite recent global de-escalations.