UK Macro Daily(Beta Mode)

UK Housing Data Disappoints

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,608.90 | +2.51% |

| FTSE 250 | 22,205.60 | -1.02% |

| GBP/USD | 1.34 | +0.20% |

| GBP/EUR | 1.15 | -0.07% |

| GBP/JPY | 213.70 | +0.58% |

| Brent Crude | 96.85 | +0.97% |

| Gold | 4,790.40 | -0.04% |

| UK Nat Gas | 2.66 | -0.22% |

| Bitcoin | 72,110.96 | +1.39% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

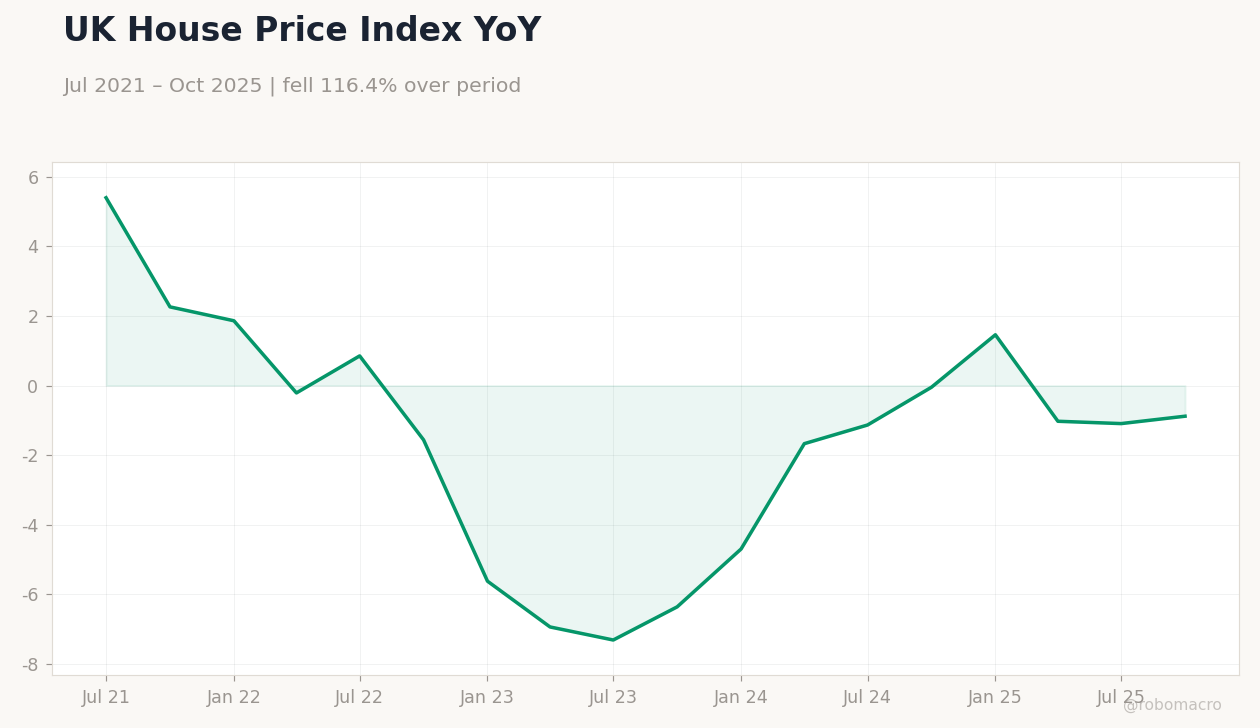

| Halifax House Price Index Month-over-Month | 0.30 | 0.10 | -0.50 |

| Halifax House Price Index Year-over-Year | 1.20 | 1.50 | 0.80 |

| S&P Global Construction PMI | 44.50 | 43.90 | 45.60 |

| RICS House Price Balance | -14 | -18 | -23 |

UK 10Y Gilt Yield | Type: macro_line | 10Y Yield %: 4.432 (2026-02-01) | Range: 0.644–4.689 | Trend(6pt): 0.9058,2.145,4.42,4.416,4.451,4.432

UK 10Y Gilt Yield | Type: macro_line | 10Y Yield %: 4.432 (2026-02-01) | Range: 0.644–4.689 | Trend(6pt): 0.9058,2.145,4.42,4.416,4.451,4.432

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK housing metrics weakened, with Halifax prices falling short of expectations and RICS balance deteriorating, highlighting sector pressures.

- Construction PMI exceeded forecasts, providing a counterbalance, while FTSE 100 rose sharply amid mixed market moves.

- BoE warnings on Iran conflict and global risks influenced sentiment, with sterling showing modest gains.

Yesterday's Recap

UK housing indicators disappointed, as the Halifax House Price Index declined 0.5% month-over-month versus a consensus of 0.1%, and year-over-year growth slowed to 0.8% against an expected 1.5%. The RICS House Price Balance dropped to -23, below the forecast of -18, reflecting ongoing property market challenges. In contrast, the S&P Global Construction PMI rose to 45.6, beating the consensus of 43.9 and prior reading of 44.5, indicating slight sector improvement.

The FTSE 100 advanced 2.51% to 10,608.90, supported by energy and banking gains in a risk-on environment, while the FTSE 250 fell 1.02% to 22,205.60 due to small-cap weakness. Sterling firmed slightly, with GBP/USD up 0.20% to 1.34 and GBP/JPY climbing 0.58% to 213.70, though GBP/EUR eased 0.07% to 1.15. The UK 10-year gilt yield decreased 0.42 percentage points to 4.43%, amid safe-haven demand, as Brent crude rose 0.97% to 96.85 despite regional tensions.

Markets navigated the mixed data cautiously, with geopolitical concerns taking precedence.

The Day Ahead

No significant UK economic releases or events are slated for today, allowing time to process yesterday's housing and construction updates. Focus may turn to any impromptu Bank of England statements or international factors affecting sterling and gilts. Tomorrow similarly features no key data, likely directing attention to global influences such as oil dynamics and US policy signals.

Traders should watch for carryover from European or US markets, potentially swaying FTSE performance and currency pairs. Volatility could remain subdued absent unexpected developments, though Middle East escalations, as noted in BoE commentary, may introduce uncertainty.

Other Economic Notes

UK housing faces headwinds from elevated interest rates and affordability strains, with recent figures raising concerns for consumer activity. MUFG highlighted PMI inflation increases adding uncertainty to the economic path, possibly postponing monetary easing. The Bank of England's work on a stablecoin framework reflects efforts to regulate digital assets and enhance stability in evolving financial landscapes.