UK Macro Daily(Beta Mode)

FTSE Up as Iran Tensions Simmer

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,667.60 | +0.73% |

| FTSE 250 | 22,940.20 | -1.14% |

| GBP/USD | 1.35 | +0.25% |

| GBP/EUR | 1.15 | -0.07% |

| GBP/JPY | 214.81 | +0.11% |

| Brent Crude | 94.45 | -1.08% |

| Gold | 4,806.50 | -0.00% |

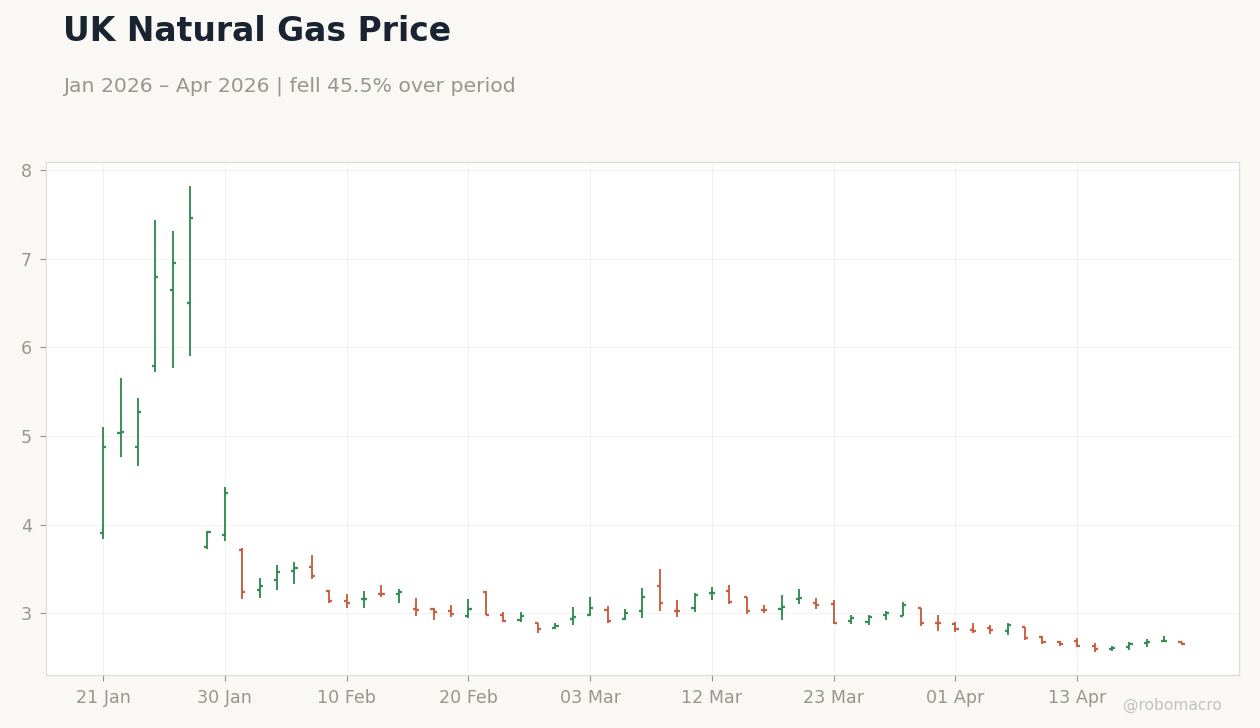

| UK Nat Gas | 2.66 | -1.19% |

| Bitcoin | 75,828.70 | +2.67% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.70% | +6.05% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

UK 10Y Gilt Yield | Type: macro_line | 10Y Yield %: 4.701 (2026-03-01) | Range: 0.644–4.701 | Trend(6pt): 0.9058,2.145,4.42,4.416,4.451,4.701

UK 10Y Gilt Yield | Type: macro_line | 10Y Yield %: 4.701 (2026-03-01) | Range: 0.644–4.701 | Trend(6pt): 0.9058,2.145,4.42,4.416,4.451,4.701

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 5.20 | 5.20 | 02:00 |

| Average Earnings incl. Bonus (3Mo/Yr) | 3.90 | 3.60 | 02:00 |

| Employment Change | 84,000 | - | 02:00 |

| Wednesday (2026-04-22) | |||

| Inflation Rate Year-over-Year | 3 | 3.30 | 02:00 |

| Core Inflation Rate Year-over-Year | 3.20 | 3.20 | 02:00 |

| Inflation Rate Month-over-Month | 0.40 | 0.60 | 02:00 |

| Thursday (2026-04-23) | |||

| S&P Global Manufacturing PMI Flash | 51 | 49.90 | 04:30 |

| S&P Global Services PMI Flash | 50.50 | 50 | 04:30 |

- FTSE 100 climbs 0.73% on energy gains amid Middle East risks.

- 10Y Gilt yield rises to 4.70% with +6.05% change, reflecting BoE caution.

- GBP/USD edges up 0.25% to 1.35 in volatile trading.

Yesterday's Recap

UK markets displayed mixed performance with the FTSE 100 closing at 10,667.60, up 0.73%, supported by energy sector strength amid Brent crude supply concerns from US-Iran tensions. The FTSE 250 fell 1.14% to 22,940.20, indicating caution in mid-caps tied to domestic growth. Sterling saw modest gains, with GBP/USD at 1.35 (+0.25%) and GBP/JPY at 214.81 (+0.11%), while GBP/EUR slipped 0.07% to 1.15.

Brent crude declined 1.08% to 94.45, pressured by geopolitical fears, and UK natural gas dropped 1.19% to 2.66. Gold remained flat at 4,806.50, acting as a safe haven, while Bitcoin rose 2.67% to 75,828.70. UK 10-year gilt yield increased to 4.70% with a +6.05% change, signaling tempered BoE easing expectations.

No major UK data releases yesterday, but reports highlighted February's 0.5% economic growth exceeding forecasts, aiding sentiment despite recession risks from Middle East conflicts.

The Day Ahead

Today's highlights include the headline unemployment rate at 02:00 ET, expected at 5.2% matching previous 5.2%, plus average earnings including bonus (3Mo/Yr) at 3.6% versus prior 3.9%. Employment change, with previous 84,000, has no consensus but will signal labor trends. Tomorrow features inflation data: YoY rate consensus 3.3% against previous 3.0%, core YoY at 3.2%, and MoM at 0.6%.

Thursday includes S&P Global Manufacturing PMI flash at 49.9 (prior 51.0) and Services PMI at 50.0 (prior 50.5) at 04:30 ET, followed by CBI Business Optimism Index and Industrial Trends Orders at 06:00 ET, and GFK Consumer Confidence at -25 at 19:01 ET. Friday brings retail sales MoM at 0.2% versus prior -0.4%, with YoY at 1.3%.

Other Economic Notes

UK economy showed strength with February's 0.5% growth beating expectations, though Middle East crises pose recession risks and threaten 250,000 jobs. Wage growth persists above BoE targets, fueling sticky inflation at 3.40% YoY as of March 2025. Policymakers stress fiscal discipline, limiting stimulus options.

Banking downgrades, especially at Barclays, highlight sector vulnerabilities to slowdowns. Unemployment stands at 5.20% as of November 2025, underscoring labor market resilience amid global uncertainties.