UK Macro Daily(Beta Mode)

UK Inflation Hits 3.3%, Jobs Strengthen

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,498.10 | -1.05% |

| FTSE 250 | 22,972.00 | +0.00% |

| GBP/USD | 1.35 | -0.12% |

| GBP/EUR | 1.15 | +0.19% |

| GBP/JPY | 215.29 | +0.17% |

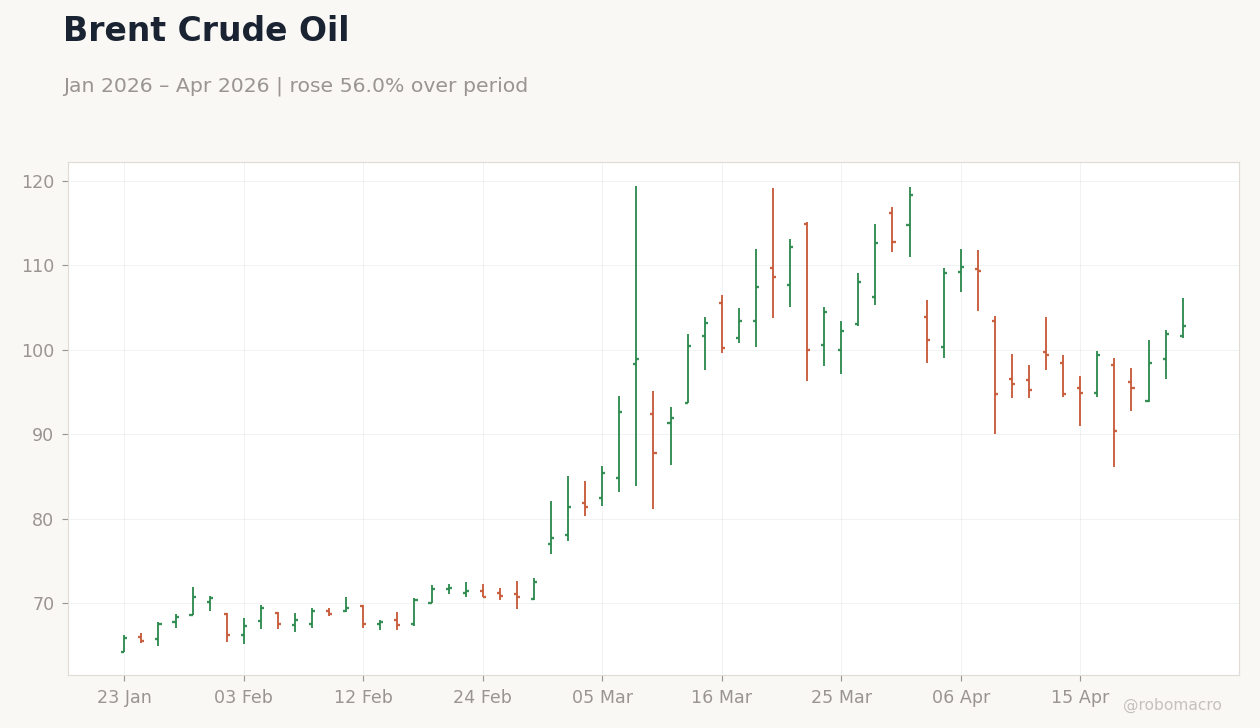

| Brent Crude | 102.83 | +0.90% |

| Gold | 4,728.40 | -0.09% |

| UK Nat Gas | 2.71 | -0.29% |

| Bitcoin | 78,249.89 | +2.48% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.70% | +6.05% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 5.20 | 5.20 | 4.90 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.10 | 3.60 | 3.80 |

| Employment Change | 84,000 | - | 25,000 |

| Inflation Rate Year-over-Year | 3 | 3.30 | 3.30 |

| Core Inflation Rate Year-over-Year | 3.20 | 3.20 | 3.10 |

| Inflation Rate Month-over-Month | 0.40 | 0.60 | 0.70 |

UK House Prices YoY | Type: macro_line | House Price Index: -0.8816 (2025-10-01) | Range: -7.308–5.391 | Trend(6pt): 5.391,0.8499,-7.308,-1.134,-1.094,-0.8816

UK House Prices YoY | Type: macro_line | House Price Index: -0.8816 (2025-10-01) | Range: -7.308–5.391 | Trend(6pt): 5.391,0.8499,-7.308,-1.134,-1.094,-0.8816

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 51 | 49.90 | 00:30 |

| S&P Global Services PMI Flash | 50.50 | 50 | 00:30 |

| CBI Business Optimism Index | -19 | - | 02:00 |

| CBI Industrial Trends Orders | -27 | -30 | 02:00 |

| GFK Consumer Confidence Index | -21 | -25 | 15:01 |

- UK inflation rose to 3.3% YoY, matching consensus amid fuel pressures, with core at 3.1%.

- Unemployment dropped to 4.9%, earnings at 3.8%, showing labor market strength despite slower hiring.

- FTSE 100 fell 1.05%, 10Y gilt yields up 6.05% to 4.70% on inflation worries.

Yesterday's Recap

UK economic data revealed mixed signals, with inflation accelerating to 3.3% year-over-year, aligning with consensus but up from the previous 3% due to fuel price pressures, while core inflation eased to 3.1% versus expectations of 3.2%. Headline unemployment rate fell to 4.9% from 5.2%, beating forecasts and indicating robust labor demand, though employment change slowed to 25,000 from 84,000 prior. Average earnings including bonuses increased 3.8% on a three-month year-over-year basis, surpassing the 3.6% consensus and underscoring persistent wage pressures.

Monthly inflation rose 0.7%, above the 0.6% estimate, driven by transport and housing costs. Markets reacted cautiously: FTSE 100 declined 1.05% to 10,498.10, reflecting global risk aversion, while FTSE 250 remained flat at 22,972.00. Sterling softened slightly with GBP/USD down 0.12% to 1.35, but GBP/EUR rose 0.19% to 1.15 amid eurozone weakness.

UK 10-year gilt yields increased 6.05% to 4.70%, signaling inflation concerns overriding jobs strength.

The Day Ahead

Flash S&P Global Manufacturing PMI is scheduled at 00:30 ET, with consensus at 49.9 versus previous 51.0, potentially indicating contraction if below 50. Services PMI releases simultaneously, expected at 50 from 50.5 prior, key for assessing the dominant sector's momentum. CBI Business Optimism Index and Industrial Trends Orders come at 02:00 ET, with orders consensus at -30 from -27, providing manufacturing sentiment insights.

GFK Consumer Confidence Index follows at 15:01 ET, forecasted at -25 from -21, reflecting cost-of-living strains. These releases could sway sterling pairs and gilt yields, particularly if PMIs signal slowdown. Markets may also monitor US earnings spillover.

Other Economic Notes

UK economy faces ongoing inflationary pressures from energy and wages, hindering the return to a 2% target despite labor market improvements. Household optimism is at record lows due to price rises, potentially dampening consumption as per reports. Structural challenges, including post-Brexit trade and North Sea energy investments, underscore the importance of energy security for stability.