UK Macro Daily(Beta Mode)

PMIs Surge, Inflation Steady

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,476.50 | -0.21% |

| FTSE 250 | 22,764.50 | -0.90% |

| GBP/USD | 1.35 | -0.25% |

| GBP/EUR | 1.15 | -0.05% |

| GBP/JPY | 215.17 | -0.06% |

| Brent Crude | 105.32 | +0.24% |

| Gold | 4,697.00 | -0.17% |

| UK Nat Gas | 2.72 | +4.17% |

| Bitcoin | 77,977.40 | -0.29% |

| UK 2Y Gilt | - | - |

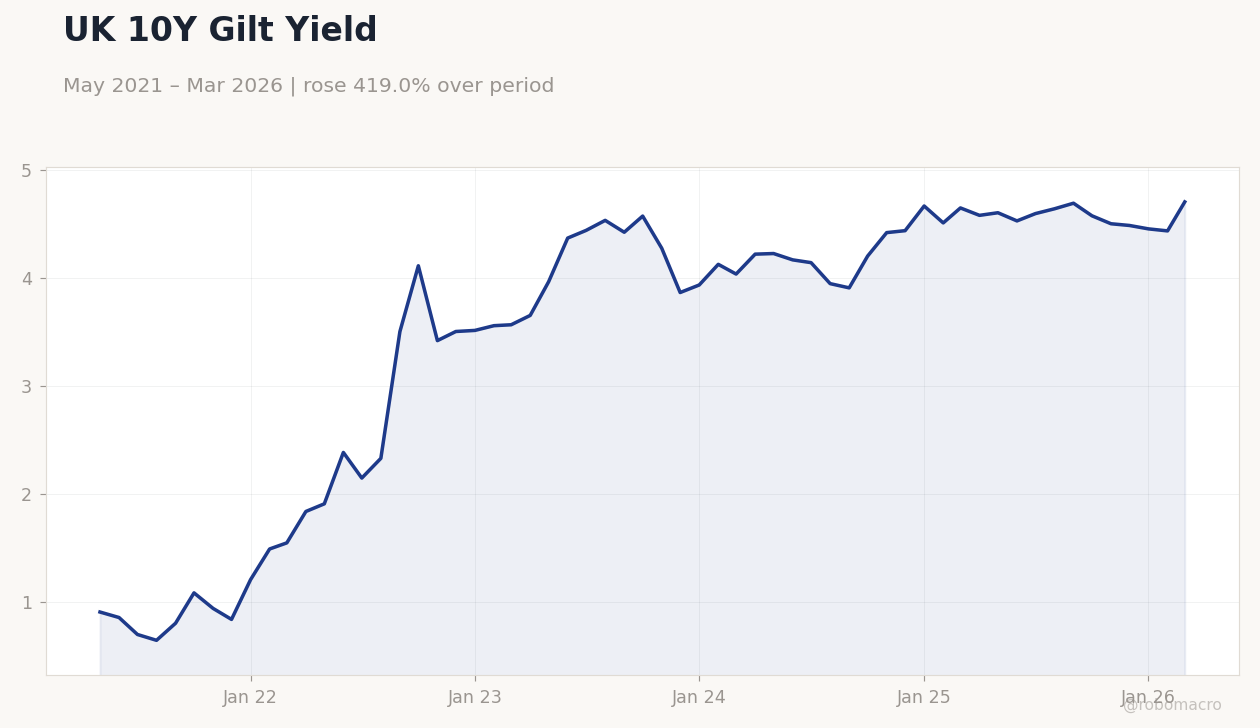

| UK 10Y Gilt | 4.70% | +6.05% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 5.20 | 5.20 | 4.90 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.10 | 3.60 | 3.80 |

| Employment Change | 84,000 | - | 25,000 |

| Inflation Rate Year-over-Year | 3 | 3.30 | 3.30 |

| Core Inflation Rate Year-over-Year | 3.20 | 3.20 | 3.10 |

| Inflation Rate Month-over-Month | 0.40 | 0.60 | 0.70 |

| S&P Global Manufacturing PMI Flash | 51 | 49.90 | 53.60 |

| S&P Global Services PMI Flash | 50.50 | 50 | 52 |

| CBI Business Optimism Index | -19 | - | -65 |

| CBI Industrial Trends Orders | -27 | -30 | -38 |

UK 10Y Gilt Yield | Type: macro_line | % Yield: 4.701 (2026-03-01) | Range: 0.644–4.701 | Trend(6pt): 0.9058,2.145,4.42,4.416,4.451,4.701

UK 10Y Gilt Yield | Type: macro_line | % Yield: 4.701 (2026-03-01) | Range: 0.644–4.701 | Trend(6pt): 0.9058,2.145,4.42,4.416,4.451,4.701

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK flash PMIs beat expectations, signaling robust economic activity amid easing unemployment.

- Inflation held at consensus levels, but wage growth and cost pressures persist.

- Markets dipped slightly, with Gilt yields rising on hawkish BoE signals.

Yesterday's Recap

UK economic data showed mixed signals with flash S&P Global Manufacturing PMI surging to 53.6 against a consensus of 49.9, indicating expansion, while Services PMI rose to 52.0 versus 50 expected, boosting overall composite growth outlook. Headline unemployment rate fell to 4.9% from 5.2%, beating forecasts and reflecting labor market resilience, though employment change slowed to 25,000. Inflation metrics aligned closely with expectations, with YoY rate at 3.3% matching consensus, core YoY dipping to 3.1%, and MoM rising to 0.7% above 0.6% forecast.

CBI Business Optimism Index plunged to -65 from -19, and Industrial Trends Orders worsened to -38, highlighting manufacturing pessimism, while GfK Consumer Confidence edged down to -25. Retail sales data for March were pending release late in the day, with consensus pointing to a modest 0.2% MoM rebound. FTSE 100 closed down 0.21% at 10,476.50, FTSE 250 fell 0.90% to 22,764.50, amid broader risk aversion, while GBP/USD weakened 0.25% to 1.35 and UK 10Y Gilt yield rose to 4.70% with a change of +6.05%, reflecting inflation concerns.

The Day Ahead

No major UK data releases are scheduled for today, shifting focus to any unscheduled Bank of England commentary or market reactions to yesterday's PMI beats. Investors will monitor sterling crosses for volatility, particularly GBP/USD around 1.35, amid global risk sentiment. Broader attention turns to potential MPC member speeches, though none are confirmed, which could influence Gilt yields.

Tomorrow also lacks key events, but early next week may bring housing data previews. Expect quiet trading unless external shocks from oil prices or US data emerge.

Other Economic Notes

Broader UK themes highlight persistent cost pressures clouding the growth rebound, as seen in stronger PMIs juxtaposed with declining CBI optimism. Wage growth at 3.8% YoY exceeds expectations, potentially fueling services inflation despite core CPI easing slightly. Fiscal warnings from political figures underscore risks of tax hikes, weighing on consumer and business sentiment amid flatlining pre-crisis growth.