UK Macro Daily(Beta Mode)

CBI Trades Slump, BoE Decision Looms

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,379.10 | -0.74% |

| FTSE 250 | 22,579.40 | -0.02% |

| GBP/USD | 1.35 | +0.03% |

| GBP/EUR | 1.15 | +0.01% |

| GBP/JPY | 215.18 | -0.22% |

| Brent Crude | 103.95 | -3.95% |

| Gold | 4,644.40 | -0.66% |

| UK Nat Gas | 2.72 | +6.63% |

| Bitcoin | 76,903.46 | -2.23% |

| UK 2Y Gilt | - | - |

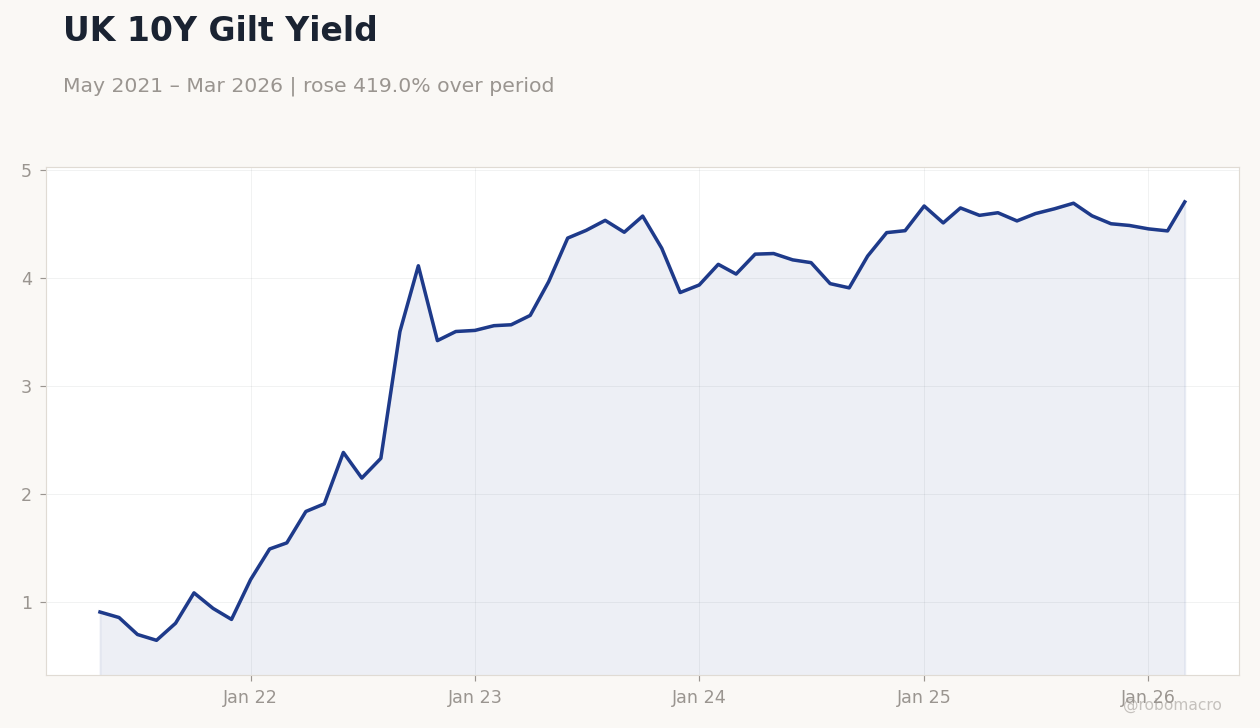

| UK 10Y Gilt | 4.70% | +6.05% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| CBI Distributive Trades | -52 | -48 | -68 |

UK 10Y Gilt Yield | Type: macro_line | 10Y Yield %: 4.701 (2026-03-01) | Range: 0.644–4.701 | Trend(6pt): 0.9058,2.145,4.42,4.416,4.451,4.701

UK 10Y Gilt Yield | Type: macro_line | 10Y Yield %: 4.701 (2026-03-01) | Range: 0.644–4.701 | Trend(6pt): 0.9058,2.145,4.42,4.416,4.451,4.701

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-04-30) | |||

| Nationwide Housing Prices Month-over-Month | 0.90 | -0.30 | 22:00 |

| Nationwide Housing Prices Year-over-Year | 2.20 | - | 22:00 |

| BoE Interest Rate Decision | 3.75 | 3.75 | 03:00 |

| BoE MPC Vote Cut | 0 | - | 03:00 |

| BoE MPC Vote Hike | 0 | - | 03:00 |

| BoE MPC Vote Unchanged | 9 | - | 03:00 |

| BoE Monetary Policy Report | - | - | 03:00 |

| MPC Meeting Minutes | - | - | 03:00 |

| Friday (2026-05-01) | |||

- CBI Distributive Trades plunged to -68, missing consensus and signaling sharp retail contraction.

- FTSE 100 dropped 0.74% amid risk-off mood; 10Y gilt yield rose to 4.70% on inflation worries.

- BoE rate decision eyed Thursday, with hold expected at 3.73% amid Iran war impacts.

Yesterday's Recap

The CBI Distributive Trades survey for April came in at -68, well below consensus of -48 and prior -52, indicating severe retail sector weakness from subdued consumer spending and supply issues. This contributed to pressure on UK stocks, with the FTSE 100 down 0.74% at 10,379.10 on global caution, while the FTSE 250 dipped 0.02% to 22,579.40, aided by some mid-cap strength. Sterling was mixed, up 0.03% to 1.35 versus USD and 0.01% to 1.15 against EUR, but down 0.22% to 215.18 on JPY.

The 10Y gilt yield climbed to 4.70% amid inflation concerns from geopolitical tensions. Energy prices varied: Brent crude fell 3.95% to 103.95 on demand fears, while UK natural gas rose 6.63% to 2.72 due to supply constraints. Gold slipped 0.66% to 4,644.40, and Bitcoin declined 2.23% to 76,903.46, reflecting broader risk aversion.

These developments highlighted UK economic vulnerabilities ahead of policy updates.

The Day Ahead

Focus shifts to Nationwide Housing Prices on April 29, with MoM consensus at -0.3% versus prior 0.9%, and YoY following 2.2% last, potentially showing property market slowdown from elevated rates. On April 30, the BoE interest rate decision is key, with consensus for no change from prior 3.75%, but verified current rate at 3.73%; accompanying Monetary Policy Report and MPC minutes will offer guidance on inflation and growth. MPC votes on cuts, hikes, and unchanged are expected to show the committee voting to hold, based on prior patterns of 0 cuts, 0 hikes, and 9 unchanged.

BoE's Pill speaks later, possibly addressing tightening and war risks. Into May 1, data includes BoE Consumer Credit, Mortgage Approvals (consensus 60,000 vs prior 62,580), and Mortgage Lending, gauging credit and consumer trends.

Other Economic Notes

UK economy faces stagnation risks, with reports noting flatlining growth before the Middle East crisis and closures of pubs and restaurants at three sites daily from cost pressures. Verified UK CPI YoY stands at 3.40% as of March 2025, exceeding the BoE's 2% target and raising worries over energy-driven inflation. Unemployment is at 5.20% as of November 2025, suggesting labor market softness that may curb wages but also reflect weak demand.