UK Macro Daily(Beta Mode)

BoE Holds Amid Iran Tensions

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,363.90 | -0.14% |

| FTSE 250 | 22,443.81 | -0.39% |

| GBP/USD | 1.35 | -0.24% |

| GBP/EUR | 1.16 | -0.06% |

| GBP/JPY | 213.90 | +0.42% |

| Brent Crude | 109.76 | -4.09% |

| Gold | 4,572.50 | +1.17% |

| UK Nat Gas | 2.78 | -2.90% |

| Bitcoin | 81,457.96 | +2.04% |

| UK 2Y Gilt | - | - |

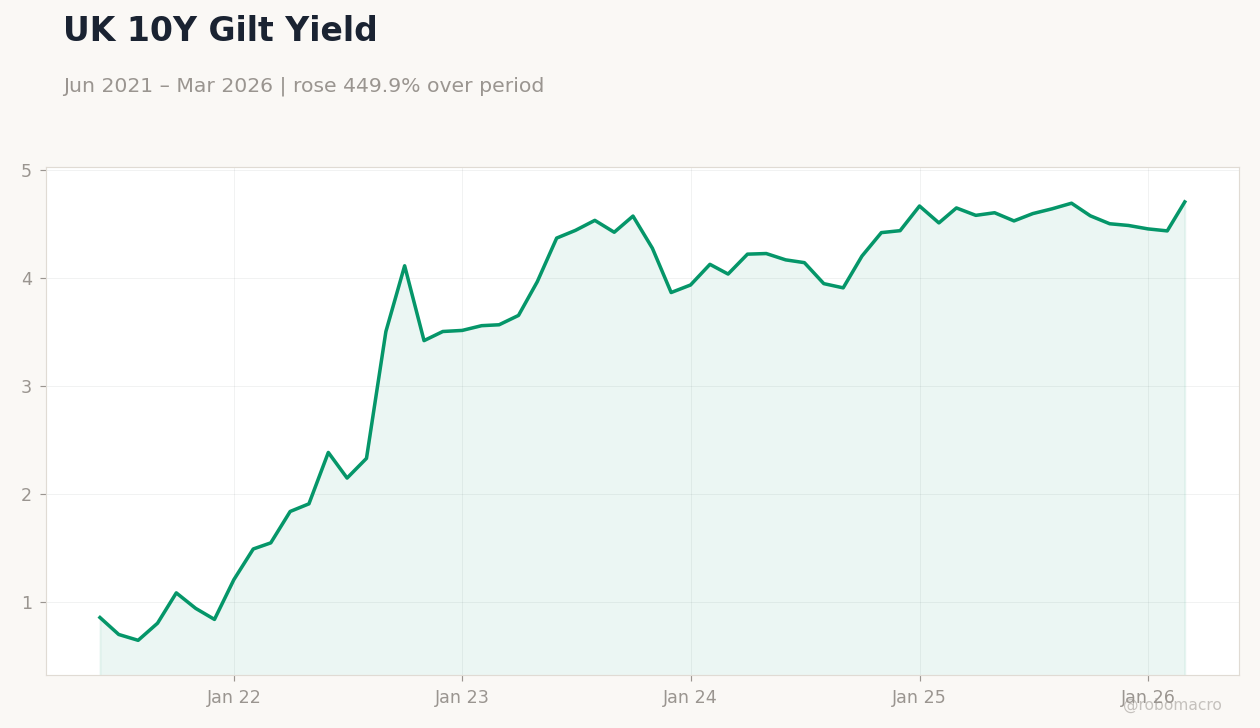

| UK 10Y Gilt | 4.70% | +6.05% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoE Woods Speech | - | - | - |

Brent Crude Oil Price | Type: macro_line | Brent Price (USD): 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(6pt): 68.62,106.1,90.73,77.3,111.9,113.9

Brent Crude Oil Price | Type: macro_line | Brent Price (USD): 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(6pt): 68.62,106.1,90.73,77.3,111.9,113.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-07) | |||

| S&P Global Construction PMI | 45.60 | 46.20 | 00:30 |

| Friday (2026-05-08) | |||

| Halifax House Price Index Month-over-Month | -0.50 | 0.20 | 22:00 |

| Halifax House Price Index Year-over-Year | 0.80 | - | 22:00 |

- BoE maintains rates at 3.73% with 8-1 MPC vote, citing energy risks from Iran conflict.

- FTSE 100 dips 0.14% on global uncertainty; 10Y Gilt yield rises to 4.70%.

- Sterling weakens vs USD, as markets eye upcoming PMI and housing data.

Yesterday's Recap

UK markets closed mixed following the BoE Woods Speech, which highlighted ongoing inflation pressures amid geopolitical tensions. The FTSE 100 ended at 10,363.90, down 0.14%, pressured by declines in energy stocks as Brent crude fell 4.09% to 109.76 amid supply concerns. FTSE 250 dropped 0.39% to 22,443.81, reflecting broader caution in mid-caps.

Sterling weakened, with GBP/USD at 1.35 (-0.24%) and GBP/EUR at 1.16 (-0.06%), while GBP/JPY rose 0.42% to 213.90 on safe-haven yen flows. UK 10Y Gilt yield climbed to 4.70% with a 6.05% change, signaling hawkish repricing after the speech. No major data releases occurred, but the speech reinforced vigilance on wage dynamics, contributing to gold's 1.17% gain to 4,572.50 as a hedge.

Overall, sentiment remained subdued, with UK Nat Gas down 2.90% to 2.78 on milder demand outlooks.

The Day Ahead

Attention turns to Thursday's S&P Global Construction PMI at 00:30, expected at 46.2 versus prior 45.6, which could signal sector recovery amid housing policy shifts. Friday brings Halifax House Price Index at 22:00, with MoM consensus at 0.2% from -0.5% prior, potentially boosting mortgage-sensitive assets if it beats. The YoY Halifax figure lacks consensus but follows 0.8% prior, offering insights into property market resilience.

No events today, allowing markets to digest recent BoE rhetoric. Broader focus includes any spillover from global news, such as UAE-US talks. Traders eye these for BoE policy implications ahead of next MPC.

Other Economic Notes

Broader UK themes include persistent inflation at 3.40% YoY CPI, pressuring households despite unemployment steady at 5.20%. Reform UK's immigration policies pose risks to labor supply and growth, as noted by economists. Energy sector faces headwinds from Iran war impacts, with farming highlighted as vulnerable.

Global Macro News

Global tensions from the US-Iran conflict are elevating energy prices, indirectly supporting UK Nat Gas despite its recent dip, as BoE warns of potential rate hikes if shocks persist. (cont...)