UK Macro Daily(Beta Mode)

BoE Holds Rates Amid Iran Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,219.10 | -1.40% |

| FTSE 250 | 22,443.80 | -0.39% |

| GBP/USD | 1.36 | +0.44% |

| GBP/EUR | 1.16 | +0.03% |

| GBP/JPY | 212.52 | -0.08% |

| Brent Crude | 108.43 | -1.31% |

| Gold | 4,674.50 | +2.61% |

| UK Nat Gas | 2.78 | -0.18% |

| Bitcoin | 81,486.60 | +0.69% |

| UK 2Y Gilt | - | - |

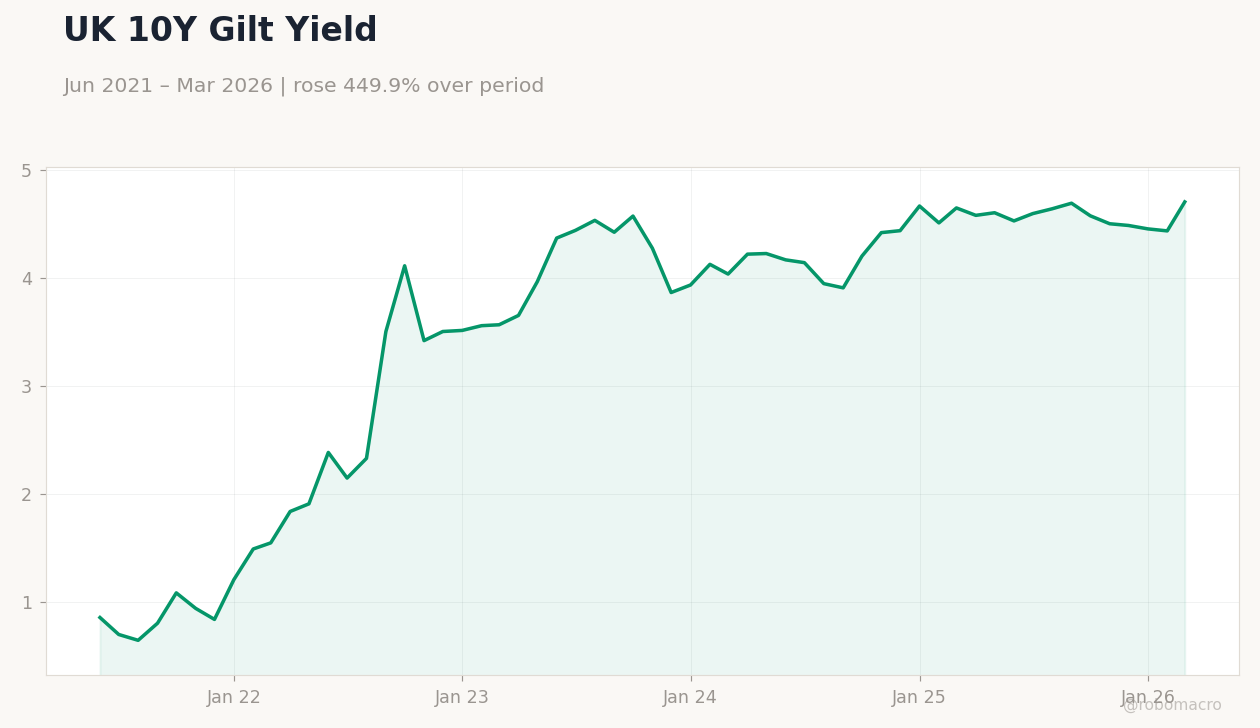

| UK 10Y Gilt | 4.70% | +6.05% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoE Woods Speech | - | - | - |

Brent Crude Price | Type: macro_line | Brent USD/bbl: 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(5pt): 68.73,106.5,86.82,78.01,113.9

Brent Crude Price | Type: macro_line | Brent USD/bbl: 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(5pt): 68.73,106.5,86.82,78.01,113.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-07) | |||

| S&P Global Construction PMI | 45.60 | 46.20 | 00:30 |

| Friday (2026-05-08) | |||

| Halifax House Price Index Month-over-Month | -0.50 | 0.20 | 22:00 |

| Halifax House Price Index Year-over-Year | 0.80 | - | 22:00 |

- Bank of England holds bank rate at 3.73%, warning of energy shocks from Iran conflict.

- Gilt yields rise sharply, 10Y at 4.70% up 6.05%; FTSE 100 drops 1.40%.

- Sterling firms to 1.36 vs USD on hawkish repricing.

Yesterday's Recap

The Bank of England maintained its bank rate at 3.73% amid global economic uncertainty and potential energy price shocks from the Iran conflict. Deputy Governor Woods gave a speech highlighting inflation vigilance, with no major data releases. UK stocks fell, FTSE 100 closing at 10,219.10 after a 1.40% decline on risk aversion in energy and banks, FTSE 250 down 0.39% to 22,443.80.

Sterling gained ground, GBP/USD up 0.44% to 1.36, GBP/EUR up 0.03% to 1.16, as markets anticipated sustained higher rates. Gilt yields jumped, 10Y at 4.70% with a 6.05% change, reflecting bets on possible hikes from energy warnings. Brent crude dropped 1.31% to 108.43, hit by demand concerns, UK natural gas down 0.18% to 2.78.

Gold climbed 2.61% to 4,674.50 as a haven asset, Bitcoin rose 0.69% to 81,486.60.

The Day Ahead

Thursday features S&P Global Construction PMI at 00:30, consensus 46.2 vs previous 45.6, gauging sector momentum amid elevated rates. Friday brings Halifax House Price Index at 22:00, monthly consensus 0.2% after -0.5% prior, year-over-year without forecast after 0.8%. These could reveal housing and consumer trends, shaping BoE demand views.

No speeches planned, but watch for BoE remarks on risks. Attention on alignment with recent wage and PMI strength.

Other Economic Notes

UK inflation persists above target, with verified CPI at 3.40% YoY as of March 2025. Unemployment at 5.20% per November 2025 data signals tight labor markets, potentially fueling wages and postponing cuts. BoE estimates QE unwind will cost taxpayers £125bn, limiting fiscal space for green initiatives.

Iran tensions heighten energy import risks, impacting farming and manufacturing as flagged by the BoE.

Global Macro News

US debt worries in French reports as a vulnerability could lift global yields, pressuring UK Gilts. UAE-US currency swap talks aim to steady oil economies, influencing Brent and UK imports. Nigerian naira firmed slightly vs USD, signaling EM stability that may affect risk sentiment and Sterling.

(cont...)