UK Macro Daily(Beta Mode)

Gilts Weaken as Energy Costs Lift Inflation Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,466.30 | +0.22% |

| FTSE 250 | 23,167.50 | +0.96% |

| GBP/USD | 1.35 | -0.05% |

| GBP/EUR | 1.16 | +0.03% |

| GBP/JPY | 214.30 | +0.01% |

| Brent Crude | 95.57 | -7.70% |

| Gold | 4,524.50 | +0.08% |

| UK Nat Gas | 3.06 | +5.16% |

| Bitcoin | 76,763.98 | -0.28% |

| UK 2Y Gilt | - | - |

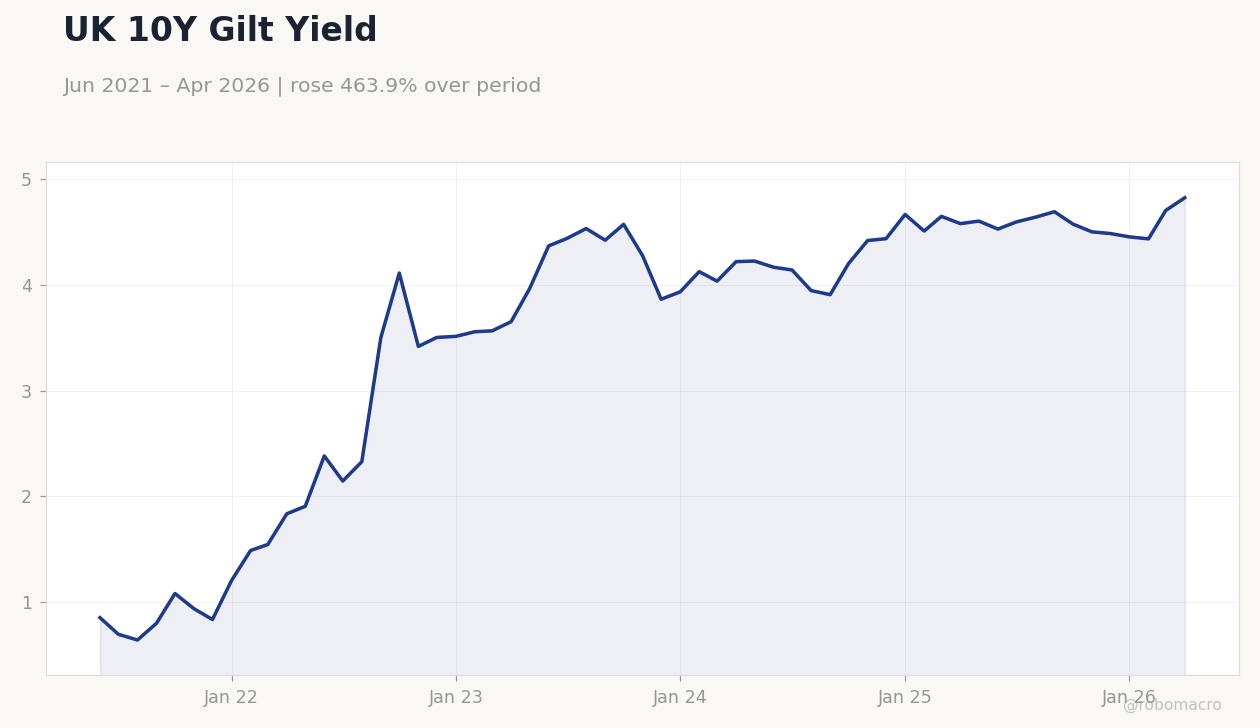

| UK 10Y Gilt | 4.82% | +2.55% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

UK 10Y Gilt Yield | Type: macro_line | Yield %: 4.821 (2026-04-01) | Range: 0.644–4.821 | Trend(6pt): 0.8549,2.328,4.569,4.434,4.432,4.821

UK 10Y Gilt Yield | Type: macro_line | Yield %: 4.821 (2026-04-01) | Range: 0.644–4.821 | Trend(6pt): 0.8549,2.328,4.569,4.434,4.432,4.821

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| CBI Distributive Trades | -68 | -60 | 02:00 |

| Thursday (2026-05-28) | |||

| BoE Breeden Speech | - | - | 00:05 |

| Friday (2026-05-29) | |||

| Nationwide Housing Prices Month-over-Month | 0.40 | - | 22:00 |

| Nationwide Housing Prices Year-over-Year | 3 | - | 22:00 |

| BoE Gov Bailey Speech | - | - | 00:20 |

- UK CPI at 3.40% y/y and 5.20% unemployment keep BoE Bank Rate at 3.73% on hold.

- FTSE 100 rises 0.22% to 10,466.30 while 10-year gilt yield climbs 2.55% to 4.82%.

- Brent crude drops 7.70% to $95.57 amid Gulf supply concerns that threaten UK energy prices.

Yesterday's Recap

Markets digested softer global risk appetite with FTSE 100 edging 0.22% higher to 10,466.30 and FTSE 250 advancing 0.96% to 23,167.50. Sterling eased modestly, with GBP/USD falling 0.05% to 1.35 while GBP/EUR gained 0.03% to 1.16. The 10-year gilt yield rose sharply by 2.55% to 4.82%, reflecting reduced expectations for near-term BoE easing.

UK natural gas climbed 5.16% to 3.06 amid supply jitters. No domestic data releases occurred on 25 May, leaving price action driven by overseas developments and positioning ahead of the CBI Distributive Trades survey.

The Day Ahead

Attention centres on the 02:00 release of CBI Distributive Trades, expected to improve to -60 from -68 and offering an early read on May consumer spending. Markets will also monitor any follow-through from the recent drop in Brent crude and its potential pass-through to June inflation prints. BoE Governor Bailey is scheduled to speak on 29 May, which could clarify the committee’s reaction function to energy-driven price pressures.

Sterling crosses remain sensitive to any shift in OIS pricing around the 3.73% Bank Rate.

Other Economic Notes

Bank lending to UK businesses has fallen to its lowest level in nearly 30 years as weak growth and tighter regulation constrain credit to SMEs. UK inflation forecasts have been revised higher due to climbing energy and food costs linked to Gulf developments. Economists argue the BoE should pause active gilt sales to avoid exacerbating funding stress in an already softening economy.

These factors together point to a prolonged period of above-target inflation and subdued domestic demand.

Global Macro News

Brent crude’s 7.70% decline to $95.57 highlights demand weakness in China and higher US inventories, yet Gulf tensions continue to threaten UK import costs. The Bank of Japan’s deputy governor stated that Middle East developments will influence the timing of any further rate hikes, adding to global policy uncertainty. These cross-currents keep sterling volatility elevated and gilt curves under pressure from external shocks.