UK Macro Daily(Beta Mode)

BoE Holds Amid Middle East Energy Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,368.10 | +0.08% |

| FTSE 250 | 23,097.42 | +0.16% |

| GBP/USD | 1.34 | -0.46% |

| GBP/EUR | 1.16 | +0.14% |

| GBP/JPY | 213.74 | -0.46% |

| Brent Crude | 94.69 | +1.72% |

| Gold | 4,350.70 | +0.31% |

| UK Nat Gas | 3.12 | -3.44% |

| Bitcoin | 63,542.79 | +0.48% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.82% | +2.55% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

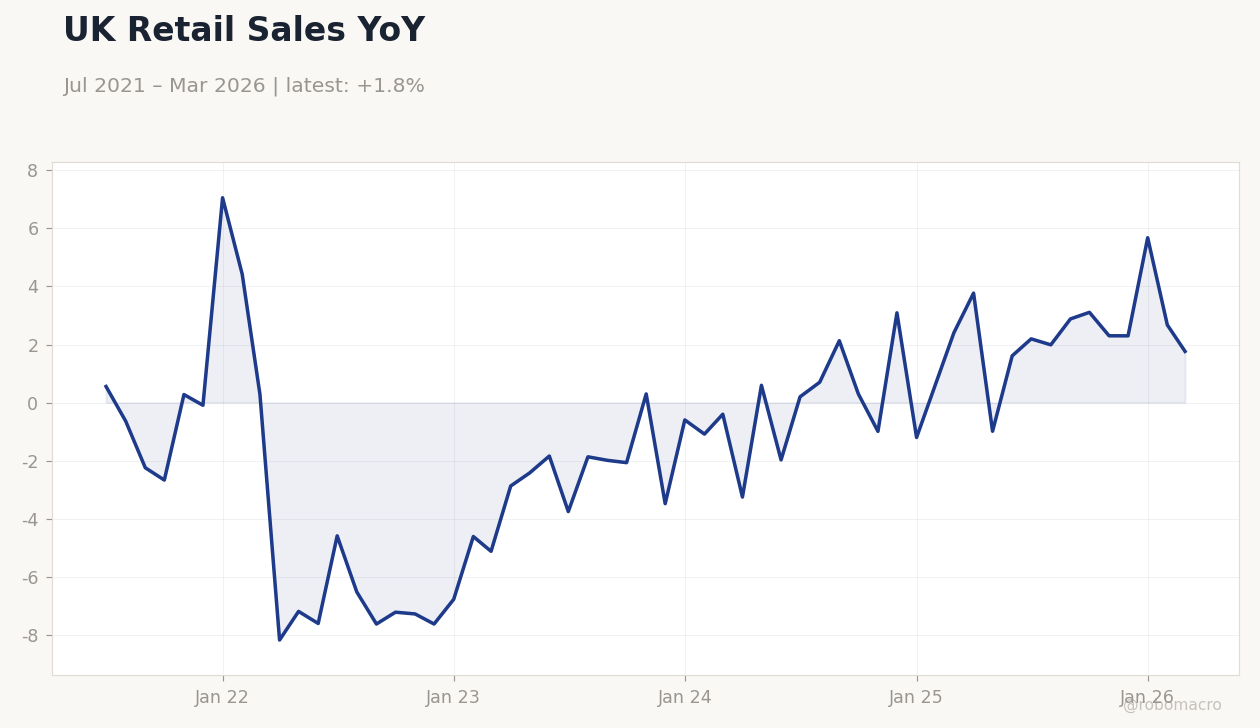

UK Retail Sales YoY | Type: macro_line | Retail Sales YoY %: 1.765 (2026-03-01) | Range: -8.179–7.058 | Trend(5pt): 0.554,-7.629,0.2982,-1.202,1.765

UK Retail Sales YoY | Type: macro_line | Retail Sales YoY %: 1.765 (2026-03-01) | Range: -8.179–7.058 | Trend(5pt): 0.554,-7.629,0.2982,-1.202,1.765

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BRC Retail Sales Monitor Year-over-Year | -3.40 | 0.60 | 15:01 |

| Wednesday (2026-06-10) | |||

| RICS House Price Balance | -34 | - | 15:01 |

| Friday (2026-06-12) | |||

| GDP Month-over-Month | 0.30 | -0.10 | 22:00 |

| GDP 3-Month Avg | 0.60 | - | 22:00 |

| Goods Trade Balance | -27,220m | -27,000m | 22:00 |

| Goods Trade Balance Non-EU | -15,195m | - | 22:00 |

| Industrial Production Month-over-Month | -0.20 | - | 22:00 |

| Manufacturing Production Month-over-Month | 1.20 | - | 22:00 |

- BRC Retail Sales Monitor expected to rebound to +0.6% YoY from -3.4%, offering first read on consumer resilience.

- BoE Bank Rate held at 3.73% with MPC citing persistent 3.4% CPI and Middle East-driven energy risks.

- FTSE 100 edged up 0.08% to 10,368.10 while 10Y gilt yields rose 2.55% to 4.82% on delayed-cut pricing.

Yesterday's Recap

UK markets digested the absence of fresh domestic data on 7 June. The FTSE 100 closed 0.08% higher at 10,368.10 while the FTSE 250 gained 0.16% to 23,097.42. Sterling weakened 0.46% versus the dollar to 1.34 but rose 0.14% against the euro to 1.16.

Brent crude climbed 1.72% to 94.69 on supply concerns, lifting UK 10Y gilt yields 2.55% to 4.82%. Natural gas fell 3.44% to 3.12 amid milder weather forecasts. No MPC members spoke, leaving swap markets pricing limited easing this year.

The Day Ahead

Attention turns to the BRC Retail Sales Monitor at 15:01 BST, with consensus pointing to a sharp turnaround to +0.6% YoY. Markets will parse the print for evidence that consumer spending is stabilising after last year’s weakness. Later in the week, RICS house-price data and the full suite of May GDP, industrial production and trade figures will arrive.

Any upside surprise in retail sales could reinforce the BoE’s cautious stance and cap gilt rallies. Traders will also monitor scheduled remarks for fresh guidance on the timing of any easing.

Other Economic Notes

UK unemployment stands at 5.2%, providing the MPC with room to keep policy restrictive. Core CPI at 3.4% remains above the 2% target, sustaining concerns over services inflation. Retail and housing indicators will be watched closely for signs that higher rates are finally cooling demand.

The ONS revisions to earlier GDP prints have reduced recession fears but not altered the BoE’s forward guidance.

Global Macro News

The dollar index held near 100 amid Middle East tensions and rising Fed-hike expectations. Brent crude’s advance to 94.69 reflected supply-risk premia that feed directly into UK energy prices. European PMIs and the German Ifo index softened, supporting sterling’s relative performance versus the euro.

Global equity sentiment stayed mixed as investors weighed US growth resilience against geopolitical uncertainty. Safe-haven flows lifted gold to 4,350.70 while bitcoin traded modestly higher. <i>↓ p.2</i>