UK Macro Daily(Beta Mode)

Retail Sales Surge Eases UK Growth Fears

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,373.20 | +0.05% |

| FTSE 250 | 23,013.40 | -0.21% |

| GBP/USD | 1.34 | +0.19% |

| GBP/EUR | 1.16 | -0.03% |

| GBP/JPY | 214.00 | +0.09% |

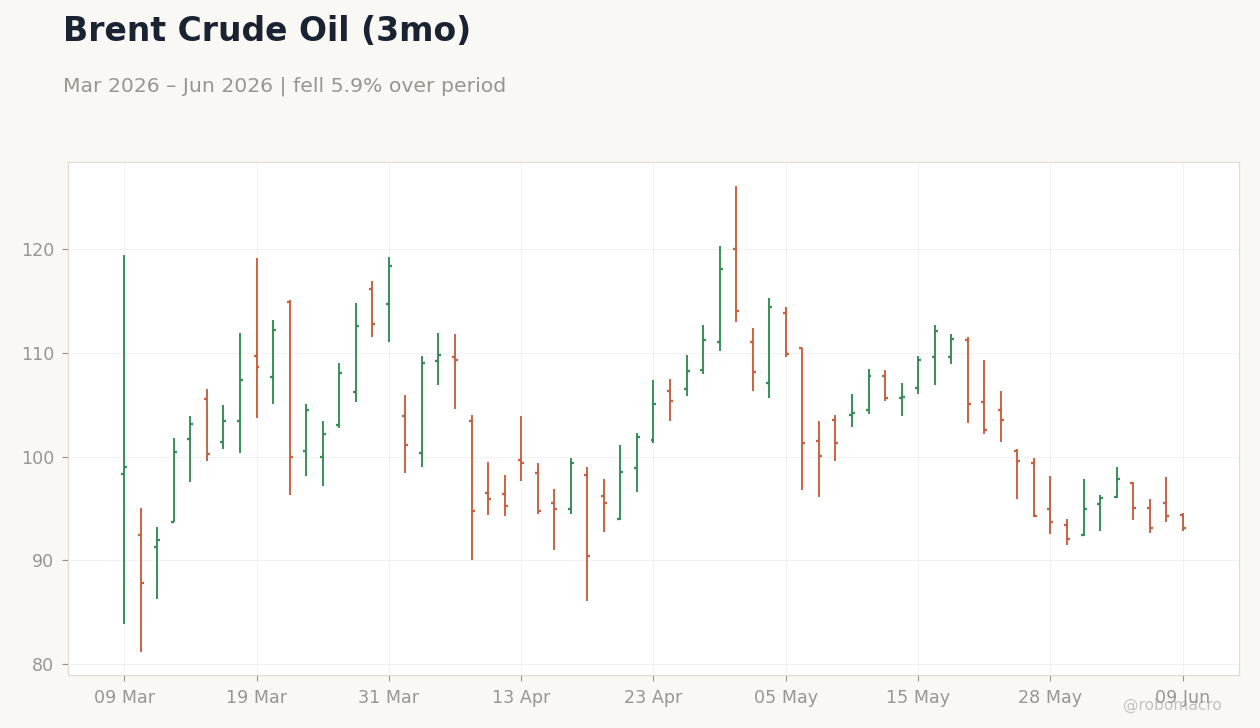

| Brent Crude | 93.29 | -1.02% |

| Gold | 4,354.80 | +0.44% |

| UK Nat Gas | 3.16 | +0.38% |

| Bitcoin | 63,400.83 | +0.49% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.82% | +2.55% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BRC Retail Sales Monitor Year-over-Year | -3.40 | 0.60 | 3.40 |

GBP/USD Exchange Rate (3mo) | Type: market_hloc | Rate: 1.336 (2026-06-09) | Range: 1.317–1.36 | Trend(6pt): 1.33,1.317,1.351,1.353,1.343,1.336

GBP/USD Exchange Rate (3mo) | Type: market_hloc | Rate: 1.336 (2026-06-09) | Range: 1.317–1.36 | Trend(6pt): 1.33,1.317,1.351,1.353,1.343,1.336

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-10) | |||

| RICS House Price Balance | -34 | - | 15:01 |

| Friday (2026-06-12) | |||

| GDP Month-over-Month | 0.30 | -0.10 | 22:00 |

| GDP 3-Month Avg | 0.60 | 0.70 | 22:00 |

| Goods Trade Balance | -27,220m | -22,850m | 22:00 |

| Goods Trade Balance Non-EU | -15,195m | - | 22:00 |

| Industrial Production Month-over-Month | -0.20 | 0.10 | 22:00 |

| Manufacturing Production Month-over-Month | 1.20 | -0.20 | 22:00 |

- BRC retail sales rebound sharply to 3.4% YoY from -3.4%

- FTSE 100 rises 0.05% while 10-year gilt yields climb 2.55% to 4.82%

- BoE signals rates stay on hold at 3.73% barring worst-case inflation spike

Yesterday's Recap

UK retail sales delivered a strong surprise as the BRC monitor printed 3.4% year-over-year, well above the 0.6% consensus and reversing the prior contraction. Equity markets showed limited reaction with the FTSE 100 closing at 10,373.20, up 0.05%, while the FTSE 250 fell 0.21% to 23,013.40. Sterling gained modestly, lifting GBP/USD to 1.34 (+0.19%) and GBP/JPY to 214.00 (+0.09%).

The 10-year gilt yield rose 2.55% to 4.82%, reflecting reduced near-term easing bets. Brent crude slipped 1.02% to 93.29 amid mixed global energy signals, and gold advanced 0.44% to 4,354.80. No MPC members spoke publicly.

The Day Ahead

Attention turns to the RICS House Price Balance release tomorrow at 15:01 BST, which is expected to show continued weakness in the housing market. High-impact GDP figures arrive on Friday including month-over-month output, the three-month average, industrial production, and the goods trade balance. Markets will monitor whether the retail sales beat feeds into stronger Friday prints or confirms a soft patch.

OIS pricing continues to embed a first 25 bp BoE cut only after the summer. Sterling volatility may increase if trade data disappoints.

Other Economic Notes

UK unemployment stands at 5.20% while CPI inflation remains elevated at 3.40% year-over-year, keeping real wage growth modest. The sharp retail sales turnaround suggests consumer resilience despite higher borrowing costs at the 3.73% Bank Rate. Gilt curves have steepened modestly as QT proceeds and bond sales add to taxpayer costs estimated at £36bn.

Housing indicators remain soft, pointing to limited wealth effects supporting consumption ahead.

Global Macro News

China’s May exports rose 19.4% despite regional disruptions from the Iran conflict, supporting global trade volumes that indirectly benefit UK exporters. The US dollar index held near 100 amid rising Fed hike bets and Middle East tensions, capping sterling upside. Brent crude’s decline reflected easing supply concerns while gold’s advance highlighted persistent safe-haven demand.

UK natural gas edged higher 0.38% to 3.16, adding to domestic energy price risks. Broader risk sentiment stayed constructive as Bitcoin rose 0.49% to 63,400.83.