UK Macro Daily(Beta Mode)

Retail Sales Beat Boosts Pound, Lifts Yields

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,254.83 | -1.14% |

| FTSE 250 | 23,013.40 | -0.21% |

| GBP/USD | 1.34 | +0.44% |

| GBP/EUR | 1.16 | +0.17% |

| GBP/JPY | 213.57 | -0.11% |

| Brent Crude | 91.29 | -0.17% |

| Gold | 4,224.50 | -0.83% |

| UK Nat Gas | 3.08 | -1.78% |

| Bitcoin | 61,288.08 | -2.86% |

| UK 2Y Gilt | - | - |

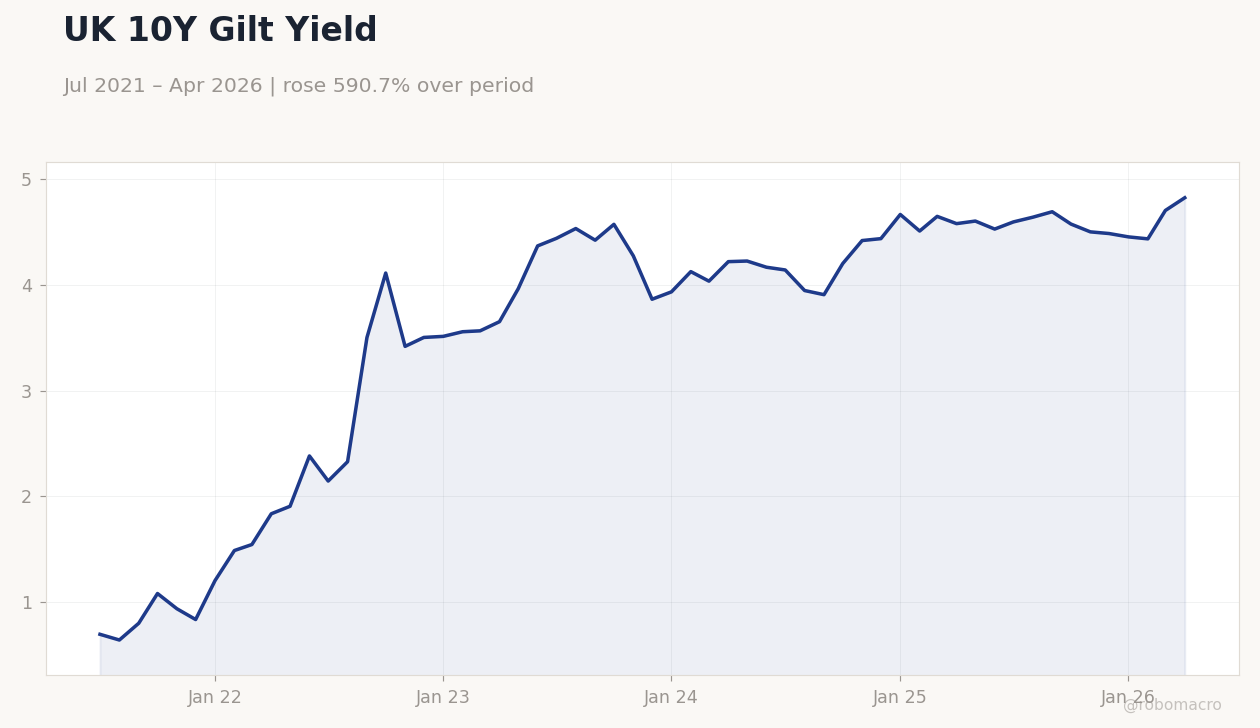

| UK 10Y Gilt | 4.82% | +2.55% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BRC Retail Sales Monitor Year-over-Year | -3.40 | 0.60 | 3.40 |

UK 10Y Gilt Yield | Type: macro_line | Yield %: 4.821 (2026-04-01) | Range: 0.644–4.821 | Trend(6pt): 0.6979,3.501,4.272,4.663,4.701,4.821

UK 10Y Gilt Yield | Type: macro_line | Yield %: 4.821 (2026-04-01) | Range: 0.644–4.821 | Trend(6pt): 0.6979,3.501,4.272,4.663,4.701,4.821

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RICS House Price Balance | -34 | - | 15:01 |

| Friday (2026-06-12) | |||

| GDP Month-over-Month | 0.30 | -0.10 | 22:00 |

| GDP 3-Month Avg | 0.60 | 0.70 | 22:00 |

| Goods Trade Balance | -27,220m | -22,850m | 22:00 |

| Goods Trade Balance Non-EU | -15,195m | - | 22:00 |

| Industrial Production Month-over-Month | -0.20 | 0.10 | 22:00 |

| Manufacturing Production Month-over-Month | 1.20 | -0.20 | 22:00 |

- BRC retail sales rebounded to 3.4% YoY, beating consensus 0.6% and signalling firmer consumer demand.

- FTSE 100 fell 1.14% to 10,254.83 while 10-year gilt yields rose 2.55% to 4.82% on the data.

- GBP/USD climbed 0.44% to 1.34 as markets pared near-term BoE easing bets.

Yesterday's Recap

UK retail sales data surprised positively yesterday with the BRC monitor printing 3.4% year-over-year against forecasts of just 0.6%. The outturn reversed four prior months of contraction and pointed to resilient household spending despite elevated borrowing costs. Equity markets reacted negatively, sending the FTSE 100 down 1.14% to close at 10,254.83 while the FTSE 250 eased 0.21%.

Sterling strengthened across the board, with GBP/USD rising 0.44% to 1.34 and GBP/EUR adding 0.17% to 1.16. Gilt yields moved higher in response, lifting the 10-year benchmark 2.55% to 4.82%. Brent crude slipped 0.17% to 91.29 while UK natural gas fell 1.78% to 3.08.

Bitcoin declined 2.86% to 61,288.08.

The Day Ahead

Attention turns to the RICS house price balance due at 15:01 today. Friday brings a heavy data schedule including GDP month-over-month, industrial production, manufacturing output and the goods trade balance. Markets will scrutinise the GDP print for signs that the earlier energy shock is now weighing on activity.

No MPC members are scheduled to speak, leaving the focus squarely on the incoming numbers.

Other Economic Notes

Deutsche Bank estimates that BoE gilt sales have already added £36 billion to UK debt-servicing costs over four years. The ONS recently revised Q1 GDP higher to 0.7% quarter-on-quarter, yet forward indicators point to a possible contraction in Q2. Labour-market resilience, with unemployment at 5.20%, continues to support the BoE’s cautious stance on easing.

Persistent inflation at 3.40% keeps real yields elevated and limits scope for near-term policy relief.

Global Macro News

China’s May exports rose 19.4% despite the Iran conflict, supporting global growth sentiment but adding to imported inflation pressures for the UK. US forces disabled an oil tanker in the Gulf of Oman, tightening energy-supply concerns and keeping Brent near 91. <i>↓ p.2</i>