UK Macro Daily(Beta Mode)

UK GDP Contracts 0.1% as Trade Gap Narrows

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,313.79 | +0.58% |

| FTSE 250 | 23,230.36 | +1.13% |

| GBP/USD | 1.34 | +0.24% |

| GBP/EUR | 1.16 | -0.02% |

| GBP/JPY | 214.49 | +0.01% |

| Brent Crude | 88.66 | -1.90% |

| Gold | 4,198.20 | +2.64% |

| UK Nat Gas | 3.07 | -0.52% |

| Bitcoin | 62,935.21 | -0.98% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.82% | +2.55% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

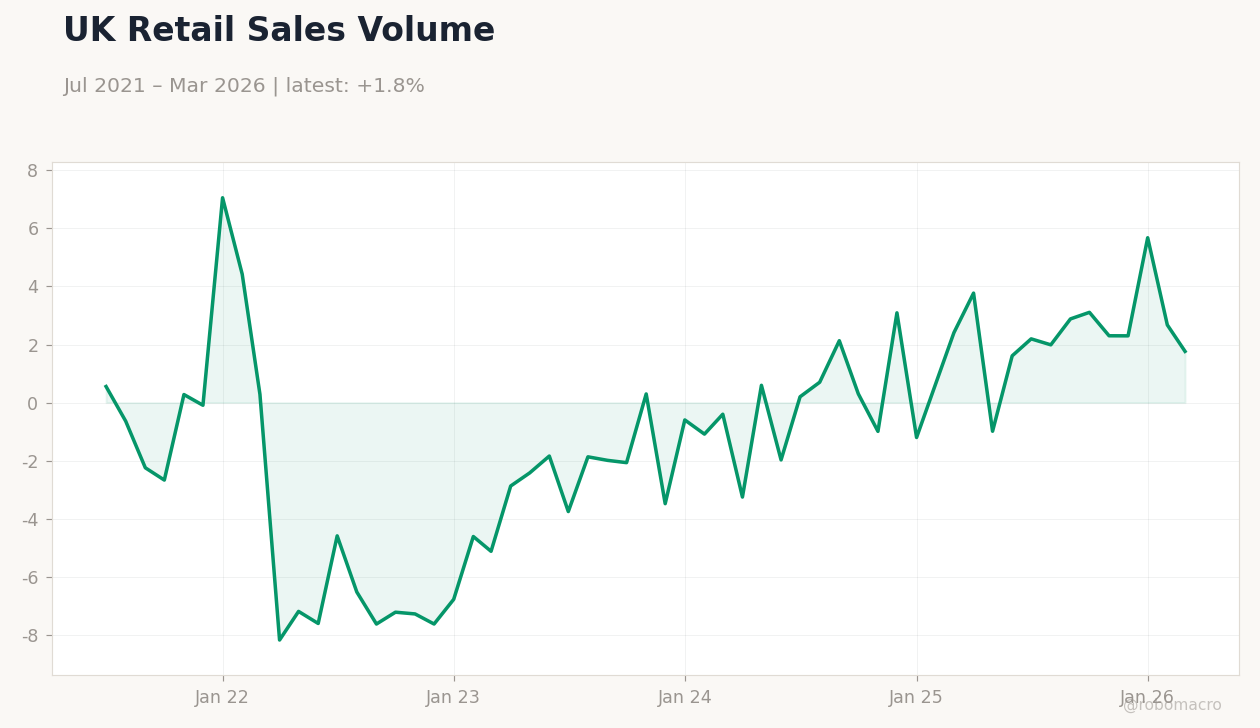

| BRC Retail Sales Monitor Year-over-Year | -3.40 | 0.60 | 3.40 |

| RICS House Price Balance | -34 | -31 | -34 |

| GDP Month-over-Month | 0.30 | -0.10 | -0.10 |

| GDP 3-Month Avg | 0.60 | 0.70 | 0.70 |

| Goods Trade Balance | -27,220m | -22,500m | -26,050m |

| Goods Trade Balance Non-EU | -15,195m | - | -13,050m |

| Industrial Production Month-over-Month | -0.20 | 0.10 | 0 |

| Manufacturing Production Month-over-Month | 1.20 | -0.20 | 0.40 |

UK 10Y Gilt Yield | Type: macro_line | Yield %: 4.821 (2026-04-01) | Range: 0.644–4.821 | Trend(6pt): 0.6979,3.501,4.272,4.663,4.701,4.821

UK 10Y Gilt Yield | Type: macro_line | Yield %: 4.821 (2026-04-01) | Range: 0.644–4.821 | Trend(6pt): 0.6979,3.501,4.272,4.663,4.701,4.821

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK GDP fell 0.1% MoM in April while the 3-month average rose 0.7%, confirming a soft patch.

- BRC retail sales jumped to +3.4% YoY, beating consensus, while RICS house prices stayed at -34.

- FTSE 100 rose 0.58% and GBP/USD gained 0.24% as 10-year gilt yields climbed 2.55% to 4.82%.

Yesterday's Recap

UK GDP contracted 0.1% month-over-month in April, matching consensus but reversing the prior 0.3% gain, while the three-month average edged up to 0.7%. Industrial production was flat and manufacturing output rose 0.4%, both missing forecasts. Goods trade balance narrowed to -£26.05bn and non-EU goods balance improved to -£13.05bn.

BRC retail sales rebounded sharply to +3.4% year-over-year against a -3.4% prior, and RICS house price balance held at -34. Equity markets advanced with FTSE 100 at 10,313.79 (+0.58%) and FTSE 250 at 23,230.36 (+1.13%). Sterling firmed modestly against the dollar to 1.34 while 10-year gilt yields rose to 4.82%.

The Day Ahead

No UK data releases are scheduled for 12 or 13 June. Markets will monitor global developments including US-Iran tensions and any follow-through from the ECB’s recent policy move. Sterling crosses and gilt yields are likely to remain sensitive to headlines on energy prices and Middle East supply risks.

Traders will also watch for any updates on fiscal guidance from the Treasury. Thin domestic calendars leave external factors as the dominant driver for UK asset prices.

Other Economic Notes

The April contraction aligns with higher fuel costs linked to Middle East instability, weighing on household spending and industrial activity. Retail sales strength offers a partial offset but appears concentrated in specific categories rather than broad-based demand. Housing indicators remain subdued, with RICS balances stuck in negative territory and pointing to limited near-term price momentum.

Overall, the data reinforce a picture of uneven growth amid external shocks.

Global Macro News

US President Trump signalled potential strikes on Iranian oil infrastructure, lifting safe-haven demand for gold which rose 2.64%. Brent crude fell 1.90% to $88.66 as traders weighed supply disruption risks against OPEC+ output signals. The ECB raised rates by 25 basis points, tightening euro-area financial conditions and supporting the euro against sterling.

<i>↓ p.2</i>