UK Macro Daily(Beta Mode)

BoE Set to Hold as CPI Stays Sticky

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,471.70 | +1.63% |

| FTSE 250 | 23,480.45 | +0.66% |

| GBP/USD | 1.34 | +0.12% |

| GBP/EUR | 1.16 | -0.17% |

| GBP/JPY | 215.05 | +0.13% |

| Brent Crude | 82.95 | -5.02% |

| Gold | 4,359.70 | +3.43% |

| UK Nat Gas | 3.03 | -2.88% |

| Bitcoin | 65,521.08 | +1.71% |

| UK 2Y Gilt | - | - |

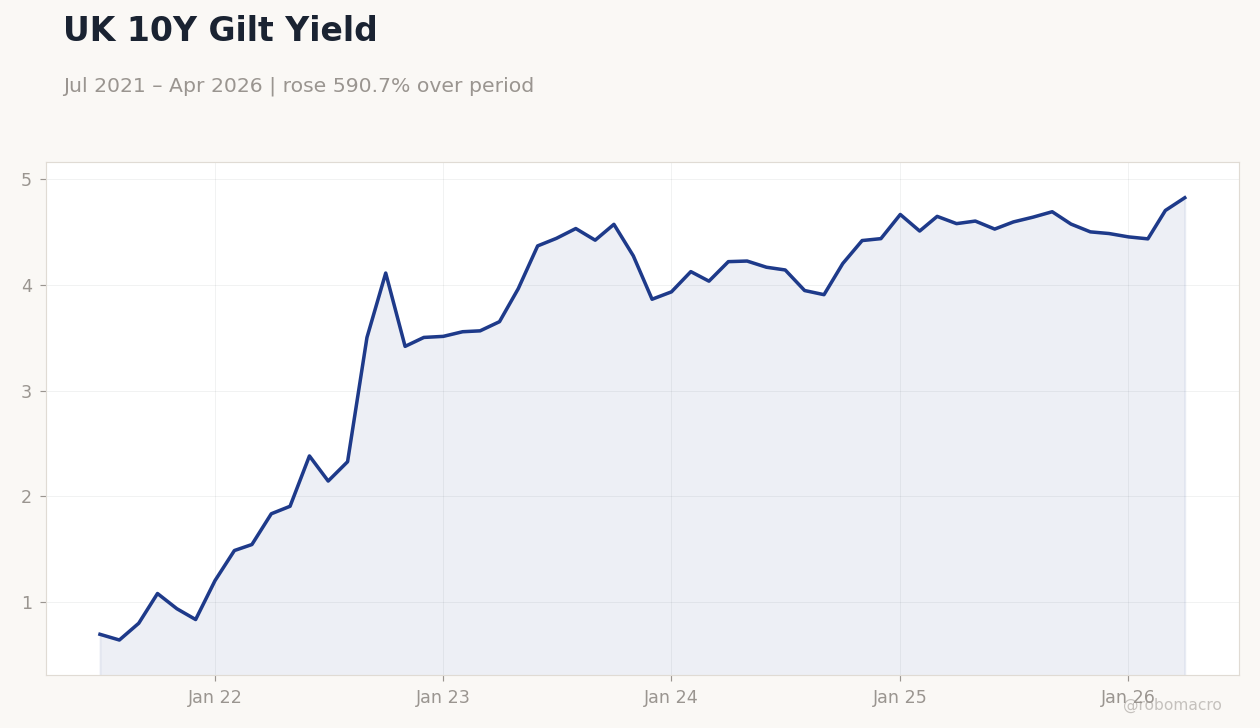

| UK 10Y Gilt | 4.82% | +2.55% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

UK 10Y Gilt Yield | Type: macro_line | 10Y Yield %: 4.821 (2026-04-01) | Range: 0.644–4.821 | Trend(6pt): 0.6979,3.501,4.272,4.663,4.701,4.821

UK 10Y Gilt Yield | Type: macro_line | 10Y Yield %: 4.821 (2026-04-01) | Range: 0.644–4.821 | Trend(6pt): 0.6979,3.501,4.272,4.663,4.701,4.821

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-17) | |||

| Inflation Rate Year-over-Year | 2.80 | - | 22:00 |

| Core Inflation Rate Year-over-Year | 2.50 | - | 22:00 |

| Inflation Rate Month-over-Month | 0.70 | - | 22:00 |

| Thursday (2026-06-18) | |||

| Headline Unemployment Rate | 5 | - | 22:00 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.10 | - | 22:00 |

| Employment Change | 148,000 | - | 22:00 |

| BoE Interest Rate Decision | 3.75 | - | 03:00 |

| BoE MPC Vote Cut | 0 | - | 03:00 |

- UK CPI at 3.40% y/y keeps BoE rate steady at 3.73% ahead of June releases.

- FTSE 100 rises 1.63% to 10,471.70 while 10Y gilt yields reach 4.82% on growth resilience.

- Sterling gains modestly versus USD as markets price only gradual near-term easing.

Yesterday's Recap

UK markets closed higher on 14 June, with the FTSE 100 advancing 1.63% to 10,471.70 and the FTSE 250 adding 0.66% to 23,480.45. Sterling posted modest gains, lifting GBP/USD to 1.34 and GBP/JPY to 215.05 while GBP/EUR eased to 1.16. Brent crude fell 5.02% to 82.95 amid softer demand signals, and gold climbed 3.43% to 4,359.70 on safe-haven flows.

UK 10Y gilt yields rose 2.55% to 4.82% as investors adjusted to firmer growth resilience. No major data prints occurred. Natural gas declined 2.88% to 3.03 while Bitcoin added 1.71%.

The Day Ahead

UK inflation data due 16 June will show the latest CPI, core CPI and monthly prints, all high-impact releases. Labour-market figures follow on 17 June, covering unemployment, earnings growth and employment changes. The BoE interest-rate decision arrives 18 June, with the committee expected to vote to hold the bank rate at 3.73%.

Retail-sales and consumer-confidence data close the week on 18-19 June. Markets will scrutinise any shifts in forward guidance for clues on future easing timing.

Other Economic Notes

UK growth showed resilience despite the April contraction, supporting the view that restrictive policy continues to anchor inflation at 3.40%. Fiscal policy remains focused on meeting rules without additional tax increases, reducing gilt volatility. Housing indicators and retail spending will test consumer strength amid elevated borrowing costs.

Broader themes centre on whether softening inflation allows measured easing without reigniting price pressures.

Global Macro News

European travel and tourism economies reached a thirty-billion-euro milestone, with strong inbound growth benefiting UK aviation and hospitality. France signalled readiness to support reopening of the Strait of Hormuz alongside the UK amid Middle East tensions. Ireland’s GDP volatility distorted eurozone aggregates and highlighted cross-border data challenges.

<i>↓ p.2</i>