UK Macro Daily(Beta Mode)

BoE Holds as Inflation Data Looms

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,471.70 | +1.63% |

| FTSE 250 | 23,341.30 | +0.07% |

| GBP/USD | 1.34 | -0.24% |

| GBP/EUR | 1.16 | -0.27% |

| GBP/JPY | 215.12 | -0.01% |

| Brent Crude | 81.53 | -1.97% |

| Gold | 4,366.90 | +0.90% |

| UK Nat Gas | 3.17 | +0.70% |

| Bitcoin | 66,541.01 | +0.38% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

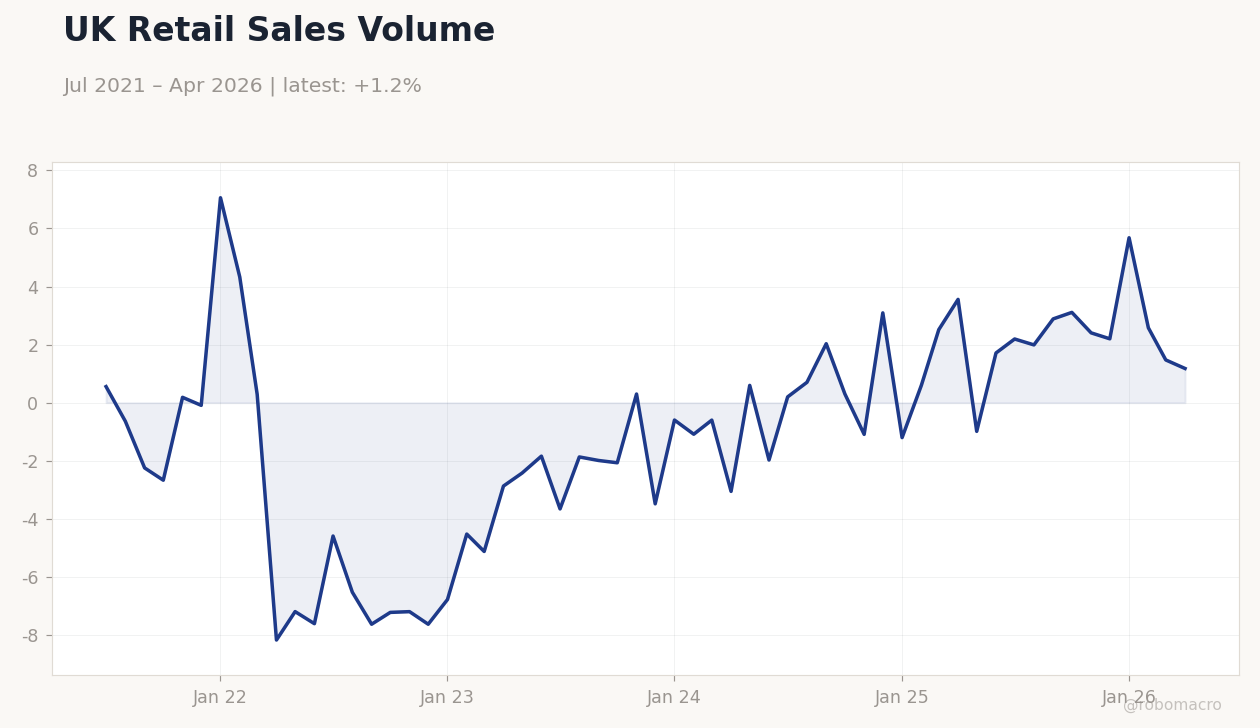

UK Retail Sales Volume | Type: macro_line | Index: 1.178 (2026-04-01) | Range: -8.172–7.058 | Trend(6pt): 0.554,-7.629,0.2982,-1.202,1.472,1.178

UK Retail Sales Volume | Type: macro_line | Index: 1.178 (2026-04-01) | Range: -8.172–7.058 | Trend(6pt): 0.554,-7.629,0.2982,-1.202,1.472,1.178

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-17) | |||

| Inflation Rate Year-over-Year | 2.80 | 3 | 22:00 |

| Core Inflation Rate Year-over-Year | 2.50 | 2.70 | 22:00 |

| Inflation Rate Month-over-Month | 0.70 | - | 22:00 |

| Thursday (2026-06-18) | |||

| Headline Unemployment Rate | 5 | 5 | 22:00 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.10 | 4 | 22:00 |

| Employment Change | 148,000 | - | 22:00 |

| BoE Interest Rate Decision | 3.75 | 3.75 | 03:00 |

| BoE MPC Vote Cut | 0 | - | 03:00 |

- UK inflation data due tonight expected to show YoY rise to 3.0% from prior 2.8%, keeping pressure on BoE policy.

- FTSE 100 rose 1.63% to 10,471.70 while 10Y gilt yields climbed 2.51% to 4.94% amid mixed sterling moves.

- BoE Bank Rate remains at 3.73% with markets pricing limited chance of near-term change ahead of Thursday’s decision.

Yesterday's Recap

UK markets closed higher on Monday with the FTSE 100 advancing 1.63% to 10,471.70 while the FTSE 250 gained a modest 0.07%. Sterling weakened, with GBP/USD falling 0.24% to 1.34 and GBP/EUR down 0.27% to 1.16. Brent crude dropped 1.97% to $81.53 and gold rose 0.90% to $4,366.90.

No major UK data prints occurred on 15 June, leaving focus on positioning ahead of the inflation release. Gilt yields edged higher, with the 10Y benchmark finishing at 4.94%. Market participants digested global signals on energy and trade routes without domestic catalysts.

The Day Ahead

UK CPI YoY, core CPI and MoM inflation figures print at 22:00 ET tonight, with consensus pointing to a 3.0% annual rate. Thursday brings the BoE Interest Rate Decision at 03:00 ET alongside MPC votes and minutes, expected to leave the Bank Rate unchanged at 3.73%. Unemployment, earnings and employment change data follow at 22:00 ET.

GfK consumer confidence and Friday retail sales complete the week’s domestic releases. Markets will watch for any shift in forward guidance on quantitative tightening.

Other Economic Notes

Persistent services inflation and wage growth near 4% continue to anchor BoE caution despite headline CPI at 3.40% in early 2025 readings. Retail sales weakness last month highlighted consumer fragility, while housing indicators remain subdued. QT bond sales proceed at a steady pace, with the governor recently defending the programme against criticism over market liquidity.

Fiscal pressures ahead of autumn tax decisions add another layer of uncertainty for gilt markets. Unemployment stands at 4.90%.

Global Macro News

ECB’s recent hike has complicated BoE timing, leaving UK rate expectations more dovish than euro-area peers. A US-Iran deal reopening the Strait of Hormuz eased near-term energy price risks, reducing the likelihood of imported inflation spikes. European tourism recovery reached €30bn, supporting UK inbound services exports.

<i>↓ p.2</i>