UK Macro Daily(Beta Mode)

UK Inflation Holds Flat Ahead of BoE Decision

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,494.20 | +0.61% |

| FTSE 250 | 23,402.93 | +0.33% |

| GBP/USD | 1.34 | +0.01% |

| GBP/EUR | 1.16 | -0.15% |

| GBP/JPY | 214.90 | -0.02% |

| Brent Crude | 78.42 | -0.68% |

| Gold | 4,346.90 | +0.37% |

| UK Nat Gas | 3.23 | -0.19% |

| Bitcoin | 65,410.07 | -0.29% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.80 | 3 | 2.80 |

| Core Inflation Rate Year-over-Year | 2.50 | 2.70 | 2.60 |

| Inflation Rate Month-over-Month | 0.70 | 0.40 | 0.20 |

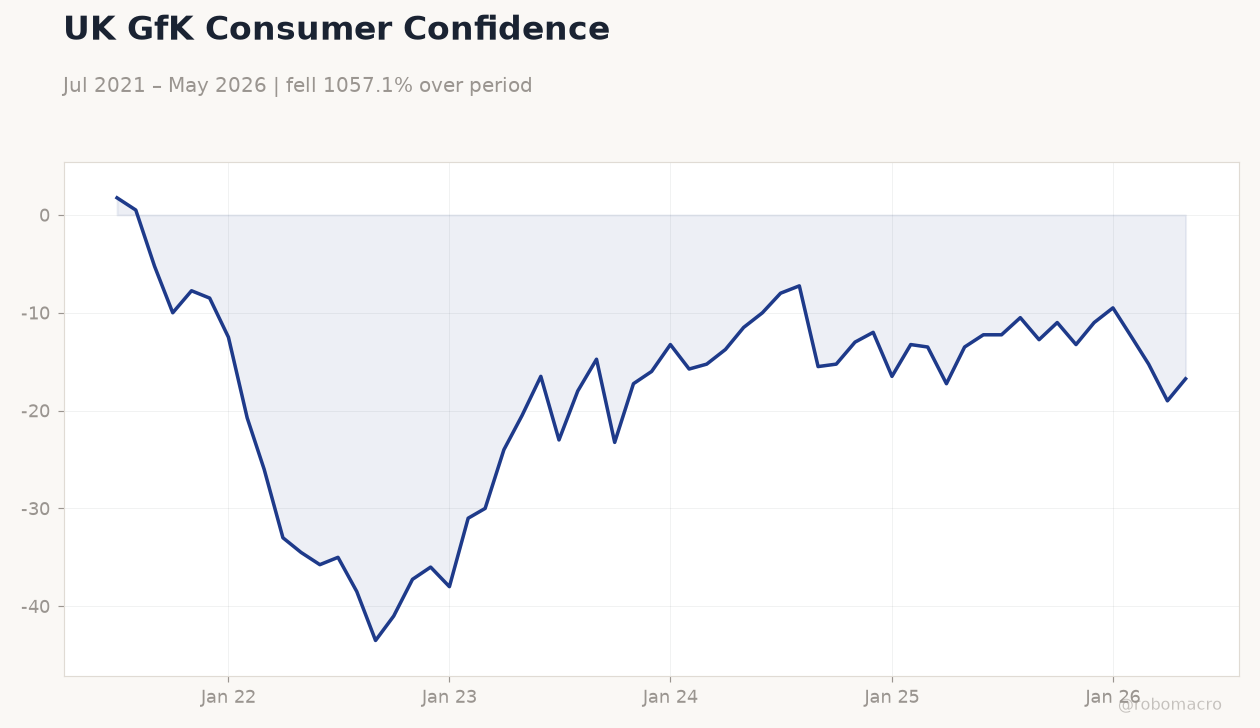

UK GfK Consumer Confidence | Type: macro_line | Consumer Confidence: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

UK GfK Consumer Confidence | Type: macro_line | Consumer Confidence: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-06-18) | |||

| Headline Unemployment Rate | 5 | 5 | 22:00 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.10 | 4 | 22:00 |

| Employment Change | 148,000 | 80,000 | 22:00 |

| BoE Interest Rate Decision | 3.75 | 3.75 | 03:00 |

| BoE MPC Vote Cut | 0 | - | 03:00 |

| BoE MPC Vote Hike | 1 | - | 03:00 |

| BoE MPC Vote Unchanged | 8 | - | 03:00 |

| MPC Meeting Minutes | - | - | 03:00 |

| GFK Consumer Confidence Index | -23 | -25 | 15:01 |

- UK CPI YoY held at 2.8% in line with prior reading while core rose 2.6%, both below consensus and signalling contained price pressures.

- FTSE 100 rose 0.61% and 10-year gilt yields climbed 2.51% as markets pared BoE cut expectations ahead of tomorrow’s decision.

- Sterling held above 1.34 against the dollar while labour-market data due later today will set the tone for MPC guidance.

Yesterday's Recap

UK CPI inflation printed unchanged at 2.8% YoY against a 3.0% consensus, with core CPI rising 2.6% versus 2.7% expected and the monthly rate slowing to 0.2%. The softer-than-forecast prints reinforced views that price pressures are moderating. Equity markets responded positively, lifting the FTSE 100 to 10,494.20 and the FTSE 250 to 23,402.93.

Gilt yields rose across the curve, with the 10-year benchmark reaching 4.94%. Sterling posted modest gains, GBP/USD reaching 1.34 while GBP/EUR eased 0.15%. Brent crude fell 0.68% to 78.42 amid softer energy prices.

Market pricing now assigns a lower probability of an immediate BoE cut.

The Day Ahead

Headline unemployment, average earnings and employment-change figures are scheduled for release at 22:00 ET today and will update the labour-market picture ahead of the MPC announcement. The BoE is expected to hold Bank Rate at 3.75% tomorrow morning. MPC minutes will be scrutinised for any shift in forward guidance.

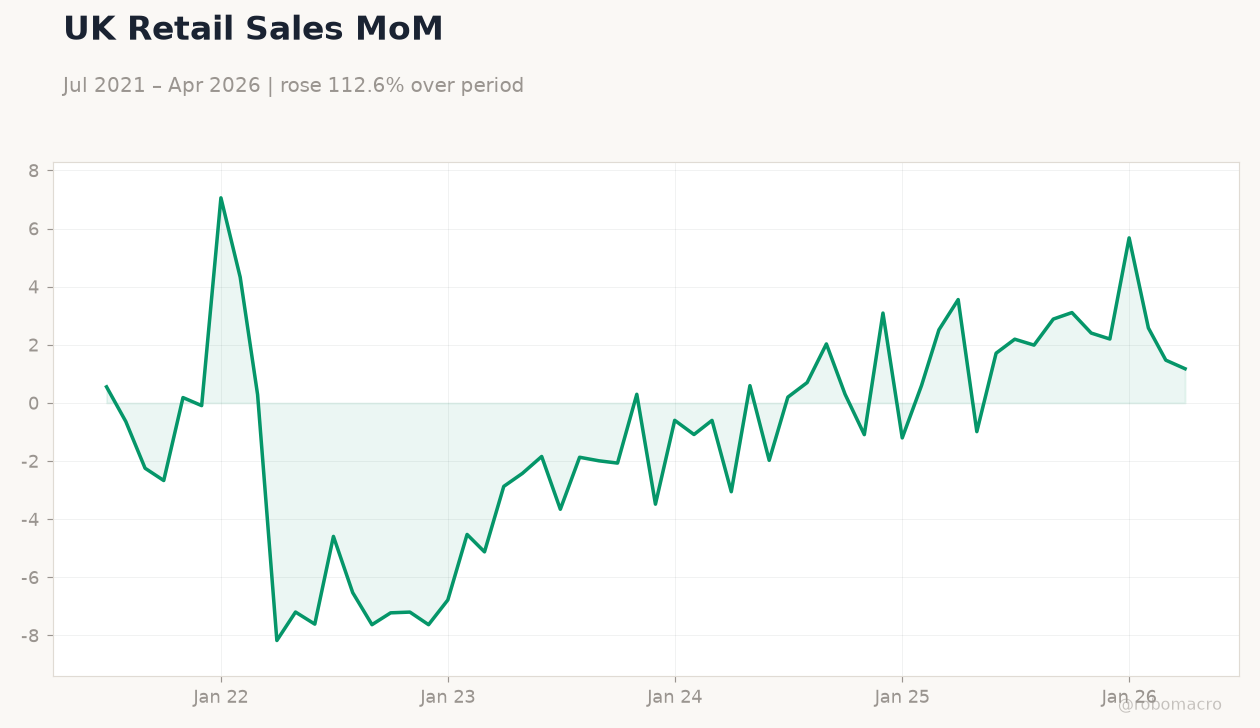

GfK consumer confidence is also due tomorrow afternoon. Retail-sales data on Friday will provide the first read on consumer spending after the inflation release.

Other Economic Notes

Recent inflation outturns leave the BoE with room to keep policy restrictive while monitoring second-round effects from wages. Fiscal guidance from the Treasury continues to emphasise deficit reduction, limiting any near-term support to growth. Housing-market indicators remain soft, with mortgage approvals still below pre-pandemic averages.

Overall, the data mix points to a gradual cooling in domestic demand without triggering an abrupt downturn.

Global Macro News

The Federal Reserve’s steady stance has supported broader risk sentiment and limited downside pressure on sterling. Euro-area final CPI figures printed in line with expectations, removing an external dovish catalyst for the BoE. <i>↓ p.2</i>