UK Macro Daily(Beta Mode)

Inflation Flat, BoE Set to Hold Rates

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,500.60 | +0.06% |

| FTSE 250 | 23,364.70 | +0.16% |

| GBP/USD | 1.33 | -0.91% |

| GBP/EUR | 1.15 | -0.12% |

| GBP/JPY | 213.67 | -0.78% |

| Brent Crude | 77.83 | -2.16% |

| Gold | 4,322.70 | -0.83% |

| UK Nat Gas | 3.14 | -0.29% |

| Bitcoin | 63,875.02 | -2.63% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.80 | 3 | 2.80 |

| Core Inflation Rate Year-over-Year | 2.50 | 2.70 | 2.60 |

| Inflation Rate Month-over-Month | 0.70 | 0.40 | 0.20 |

| Headline Unemployment Rate | 5 | 5 | - |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.10 | 4 | - |

| Employment Change | 148,000 | 75,000 | - |

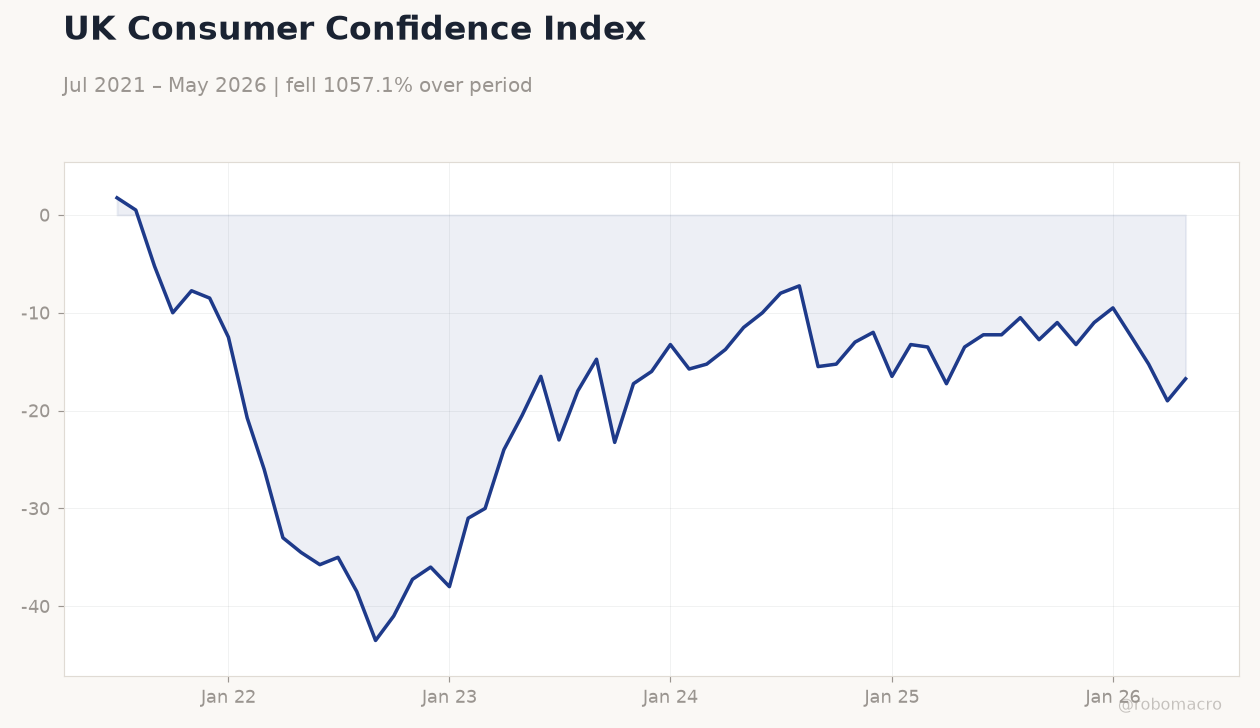

UK Consumer Confidence Index | Type: macro_line | Consumer Confidence: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

UK Consumer Confidence Index | Type: macro_line | Consumer Confidence: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoE Interest Rate Decision | 3.75 | 3.75 | 03:00 |

| BoE MPC Vote Cut | 0 | - | 03:00 |

| BoE MPC Vote Hike | 1 | - | 03:00 |

| BoE MPC Vote Unchanged | 8 | - | 03:00 |

| MPC Meeting Minutes | - | - | 03:00 |

| GFK Consumer Confidence Index | -23 | -24 | 15:01 |

- UK CPI YoY holds steady at 2.8% versus 3.0% consensus, with core at 2.6%.

- BoE expected to keep Bank Rate unchanged at 3.75% amid Middle East tensions.

- Sterling falls 0.91% against USD as markets price limited near-term easing.

Yesterday's Recap

UK inflation data released yesterday showed headline CPI YoY unchanged at 2.8%, matching the prior print but missing the 3.0% consensus. Core CPI rose 2.6% YoY, softer than the 2.7% expected, while the monthly rate printed just 0.2% against forecasts of 0.4%. The figures reinforced the view that price pressures remain contained despite earlier energy volatility.

Equity markets were little changed, with the FTSE 100 rising 0.06% to 10,500.60 and the FTSE 250 adding 0.16%. Sterling weakened across the board, with GBP/USD falling 0.91% to 1.33 and GBP/JPY dropping 0.78%. The 10-year gilt yield climbed 2.51% to 4.94%, reflecting reduced expectations for near-term rate cuts.

The Day Ahead

The Bank of England will announce its interest-rate decision at 03:00 ET, with markets fully pricing an unchanged 3.75% Bank Rate. The MPC is expected to vote to hold, and the accompanying minutes will be scrutinised for any shifts in forward guidance. GfK consumer confidence is due at 15:01 ET and is forecast to edge lower to -24.

Retail-sales figures for May, due tomorrow, are projected to rebound 0.5% MoM after April’s -1.3% print. Attention will also focus on any commentary regarding the impact of recent geopolitical developments on the inflation outlook.

Other Economic Notes

Labour-market data scheduled for release later today include the headline unemployment rate and average earnings growth, both of which will inform the BoE’s assessment of domestic demand. Persistent weakness in real wage growth would support the case for a cautious policy stance. Gilt yields have risen this week as investors scale back bets on aggressive easing, pushing the 10-year yield above 4.9%.

Housing-market indicators remain subdued, with mortgage approvals still below pre-pandemic averages.

Global Macro News

Three Iranian tankers exited the Strait of Hormuz, marking the first crude exports in two months and easing immediate supply concerns. Brent crude fell 2.16% to $77.83 per barrel on the news. US interest in African critical minerals continues to grow, with Namibia highlighted as a key partner.

<i>↓ p.2</i>