UK Macro Daily(Beta Mode)

BoE Holds at 3.75% After Soft CPI Print

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,390.03 | -1.13% |

| FTSE 250 | 23,279.45 | -0.22% |

| GBP/USD | 1.32 | -0.79% |

| GBP/EUR | 1.15 | -0.31% |

| GBP/JPY | 212.87 | -0.35% |

| Brent Crude | 80.31 | +0.58% |

| Gold | 4,169.10 | -1.30% |

| UK Nat Gas | 3.20 | -0.96% |

| Bitcoin | 62,552.09 | -0.55% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.80 | 3 | 2.80 |

| Core Inflation Rate Year-over-Year | 2.50 | 2.70 | 2.60 |

| Inflation Rate Month-over-Month | 0.70 | 0.40 | 0.20 |

| Headline Unemployment Rate | 5 | 5 | 4.90 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.40 | 4 | 4.40 |

| Employment Change | 148,000 | 75,000 | 100,000 |

| BoE Interest Rate Decision | 3.75 | 3.75 | 3.75 |

| BoE MPC Vote Cut | 0 | - | 0 |

| BoE MPC Vote Hike | 1 | - | 2 |

| BoE MPC Vote Unchanged | 8 | - | 7 |

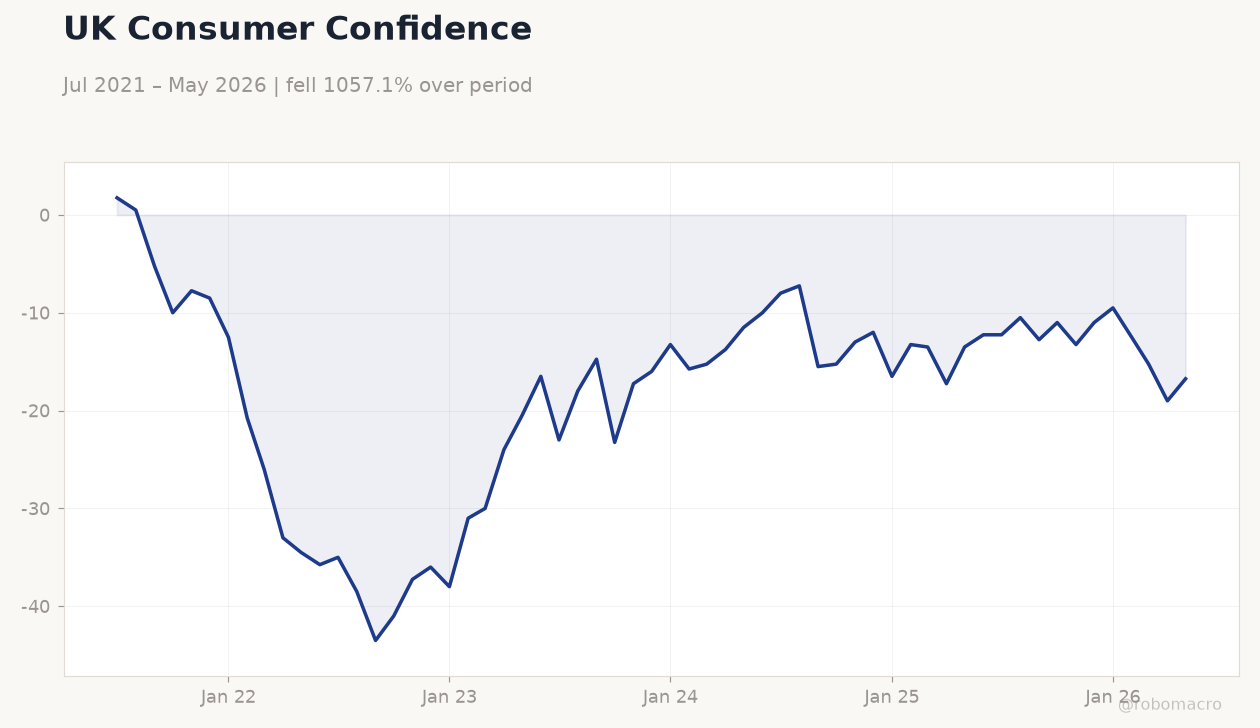

UK Consumer Confidence | Type: macro_line | Consumer Confidence: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

UK Consumer Confidence | Type: macro_line | Consumer Confidence: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK May inflation held at 2.8% y/y while core rose 0.1pp to 2.6%, both below consensus

- BoE keeps Bank Rate at 3.75% in 7-2 vote with two members favouring a hike

- FTSE 100 drops 1.13% to 10,390; 10Y gilt yield climbs 2.51% to 4.94%

Yesterday's Recap

UK May CPI came in at 2.8% y/y, matching the prior print but missing the 3.0% consensus, while core inflation edged up to 2.6% against a 2.7% forecast. The MoM reading softened to 0.2% versus 0.4% expected. Unemployment fell to 4.9% and employment rose by 100,000, though average earnings growth stayed at 4.4%.

The Bank of England left Bank Rate unchanged at 3.75%, with the committee voting 7-2 to hold despite two members preferring a hike. GfK consumer confidence printed at -23, beating the -24 consensus. Equity markets sold off with the FTSE 100 declining 1.13% and sterling weakening across the board, while the 10Y gilt yield rose sharply to 4.94%.

The Day Ahead

No UK data releases are scheduled for 19 June. Markets will monitor follow-through from yesterday’s BoE decision and any MPC member comments. Retail sales prints due tomorrow will provide the next high-impact read on consumer spending.

Sterling crosses remain sensitive to shifts in rate-cut pricing. Global developments around the US-Iran agreement may continue to influence energy prices and gilt yields.

Other Economic Notes

Softer inflation prints have reinforced expectations for eventual policy easing even as the BoE stayed on hold. Labour-market resilience, with unemployment at 4.9%, continues to support the committee’s cautious stance. Gilt yields rose on the day despite the dovish data, reflecting positioning ahead of further global central-bank signals.

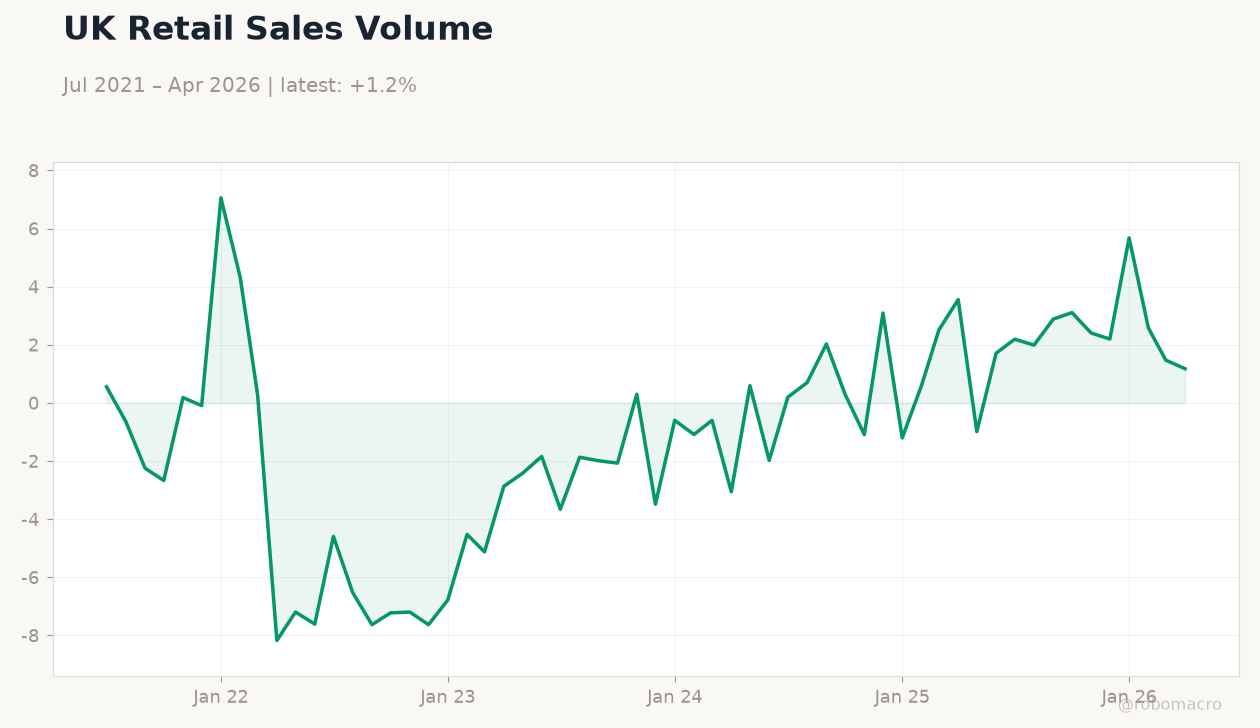

Retail sales weakness last month highlights ongoing pressure on household spending amid elevated borrowing costs.

Global Macro News

The US-Iran agreement pushed Brent crude higher to 80.31 while easing some near-term inflation risks for the UK. US gas prices fell below $4 per gallon, supporting global disinflation narratives. European pension funds are shifting allocations away from US assets due to concentration risks in technology.

Brexit-related analysis from Bank of England company data estimates a 6% long-term hit to UK output. <i>↓ p.2</i>