UK Macro Daily(Beta Mode)

PMIs and BoE Speeches Set Tone for Sterling

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,390.03 | -1.13% |

| FTSE 250 | 23,200.70 | -0.56% |

| GBP/USD | 1.32 | +0.06% |

| GBP/EUR | 1.15 | +0.05% |

| GBP/JPY | 213.52 | +0.28% |

| Brent Crude | 78.96 | -1.11% |

| Gold | 4,213.90 | -0.24% |

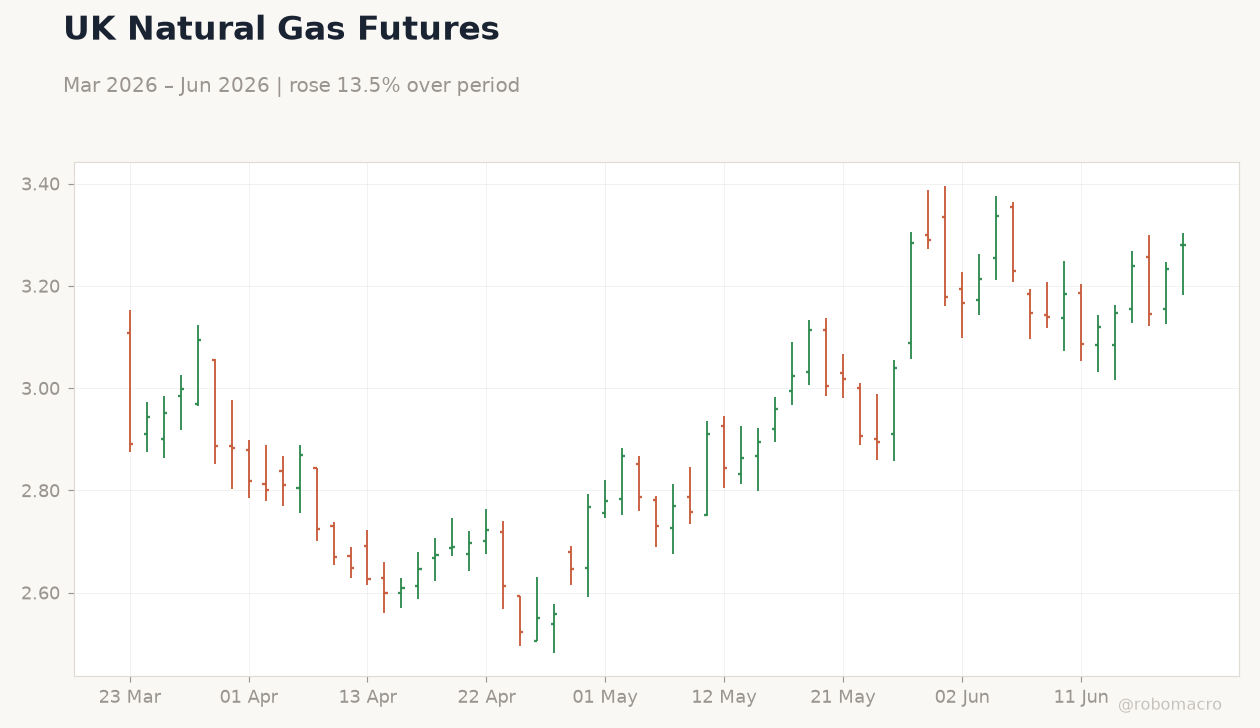

| UK Nat Gas | 3.28 | +1.42% |

| Bitcoin | 64,058.86 | -0.28% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

UK Business Confidence (OECD) | Type: macro_line | Confidence Index: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

UK Business Confidence (OECD) | Type: macro_line | Confidence Index: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-23) | |||

| S&P Global Manufacturing PMI Flash | 53.90 | 53.60 | 00:30 |

| S&P Global Services PMI Flash | 49.30 | 50 | 00:30 |

| CBI Industrial Trends Orders | -41 | -35 | 02:00 |

| BoE Taylor Speech | - | - | 05:55 |

| BoE Dhingra Speech | - | - | 09:30 |

| Wednesday (2026-06-24) | |||

| BoE Dhingra Speech | - | - | 07:00 |

| Thursday (2026-06-25) | |||

| CBI Distributive Trades | -46 | -41 | 02:00 |

- Flash PMIs expected to show modest services rebound while manufacturing softens

- Two BoE speakers to clarify rate path after recent hold at 3.73%

- Gilt yields rise as markets trim cut expectations ahead of data

Yesterday's Recap

UK markets closed lower with FTSE 100 falling 1.13% to 10,390.03 and FTSE 250 declining 0.56% to 23,200.70. The 10-year gilt yield climbed 2.51% to 4.94% as investors reduced bets on near-term easing. Sterling posted modest gains, with GBP/USD rising 0.06% to 1.32 and GBP/EUR advancing 0.05% to 1.15.

Brent crude dropped 1.11% to 78.96 while UK natural gas rose 1.42% to 3.28. No major data releases occurred on 21 June, leaving price action driven by positioning ahead of tomorrow’s indicators. Gold edged 0.24% lower to 4,213.90 amid a firmer dollar.

The Day Ahead

Markets will focus on the 00:30 S&P Global flash PMIs for June, with manufacturing consensus at 53.6 after 53.9 and services at 50.0 after 49.3. The 02:00 CBI Industrial Trends Orders survey is expected to improve to -35 from -41. BoE’s Taylor speaks at 05:55 followed by Dhingra at 09:30, both carrying high market impact.

These releases will update growth and inflation signals ahead of the next policy meeting. Traders will parse speeches for any shift in the committee’s gradual easing bias.

Other Economic Notes

Bank of England analysis shows Brexit reduced UK GDP by 6%, weighing on long-run productivity. Unemployment stands at 4.90% while CPI inflation prints 3.40% year-on-year, keeping real wage growth contained. Chancellor Reeves has signalled targeted energy support in the June fiscal statement without broad tax cuts.

EU-UK talks on sanitary and phytosanitary rules continue to progress slowly, offering limited near-term relief for trade volumes.

Global Macro News

European officials stress unity ahead of potential US policy shifts under Trump, affecting UK export outlook. South African rate-cut prospects improved after a US-brokered peace deal, indirectly supporting risk sentiment for sterling crosses. China’s tourism surge highlights shifting global demand patterns that could influence UK services exports.

US and Canadian tourism initiatives aim to capture market share, pressuring UK inbound visitor growth. Private-market stress tests launched by the BoE will examine tail risks relevant to UK pension and insurance holdings. Broader gilt movements remain sensitive to US Treasury yields and ECB signals.