UK Macro Daily(Beta Mode)

Starmer Resignation Overshadows BoE Rules

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,390.03 | -1.13% |

| FTSE 250 | 22,883.92 | -1.35% |

| GBP/USD | 1.32 | +0.16% |

| GBP/EUR | 1.16 | +0.53% |

| GBP/JPY | 213.64 | +0.20% |

| Brent Crude | 76.89 | -1.30% |

| Gold | 4,132.70 | -1.18% |

| UK Nat Gas | 3.28 | +0.92% |

| Bitcoin | 62,863.27 | -1.70% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

UK Business Confidence (Services) | Type: macro_line | Confidence Index: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

UK Business Confidence (Services) | Type: macro_line | Confidence Index: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 53.90 | 53.80 | 00:30 |

| S&P Global Services PMI Flash | 49.30 | 50.50 | 00:30 |

| CBI Industrial Trends Orders | -41 | -35 | 02:00 |

| BoE Taylor Speech | - | - | 05:55 |

| BoE Dhingra Speech | - | - | 09:30 |

- Keir Starmer resigns as Labour leader, triggering political uncertainty.

- BoE finalises softer stablecoin rules with £40B issuance cap.

- FTSE 100 drops 1.13% while 10Y gilt yields rise to 4.94%.

Yesterday's Recap

Markets absorbed Keir Starmer’s resignation announcement and the Bank of England’s release of its final stablecoin framework. The FTSE 100 closed at 10,390.03, down 1.13%, while the FTSE 250 fell 1.35%. Sterling gained modestly, with GBP/USD rising 0.16% to 1.32 and GBP/EUR advancing 0.53%.

The 10-year gilt yield climbed 2.51% to 4.94%. News that Brexit had reduced UK output by around 6% added to the cautious tone. Brent crude and gold both declined more than 1%, reflecting broader risk-off flows.

The Day Ahead

Attention turns to the 00:30 S&P Global flash PMIs. Manufacturing is expected to edge lower to 53.8 from 53.9, while services are forecast to rebound to 50.5 from 49.3. At 02:00 the CBI Industrial Trends Orders survey is projected to improve to -35 from -41.

Two Bank of England speakers follow: Taylor at 05:55 and Dhingra at 09:30. Markets will parse any fresh signals on the 3.73% Bank Rate path ahead of tomorrow’s additional Dhingra remarks.

Other Economic Notes

UK CPI remains at 3.4% and unemployment stands at 4.9%, keeping real wage growth positive but still above the Bank’s 2% target. The gilt curve has steepened modestly as investors price in a slower pace of cuts. Stablecoin regulatory clarity may support fintech activity without immediate implications for monetary aggregates.

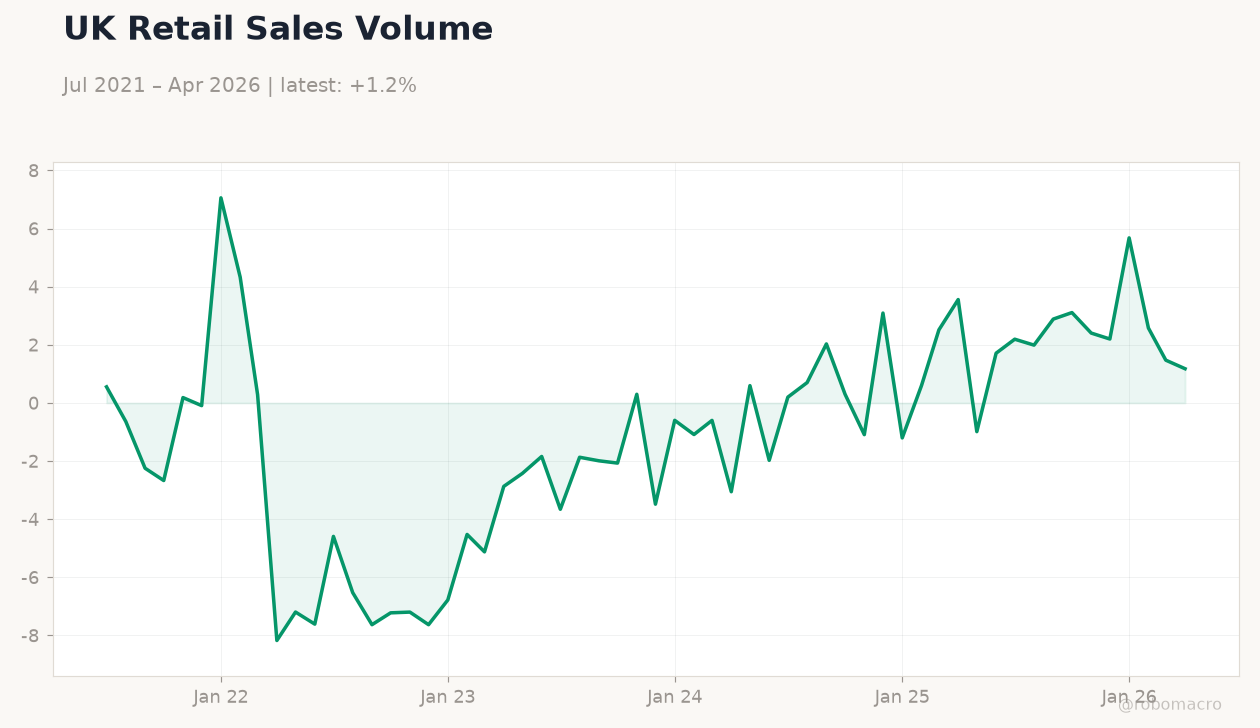

Housing and retail sales data due later this month will test whether consumer resilience persists into the second half of 2026.

Global Macro News

The Bank of England’s £40B stablecoin cap aligns with similar frameworks emerging in the EU and Singapore. Brexit-related output losses of 6% continue to weigh on long-term productivity estimates. Ukrainian labour inflows have supported Polish growth, indirectly aiding UK supply chains in manufacturing.

Gulf states including Saudi Arabia and Oman are expanding tourism capacity, offering limited offset to softer European demand. US and euro-area rate decisions later this week will influence sterling crosses and gilt spreads. Global equity weakness, evident in Bitcoin’s 1.7% decline, has spilled into UK mid-cap names.