UK Macro Daily(Beta Mode)

UK PMIs Disappoint as Services Contract

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,438.78 | -0.22% |

| FTSE 250 | 23,141.67 | +0.17% |

| GBP/USD | 1.32 | -0.19% |

| GBP/EUR | 1.16 | +0.06% |

| GBP/JPY | 213.22 | -0.04% |

| Brent Crude | 72.88 | -1.17% |

| Gold | 3,994.70 | +0.11% |

| UK Nat Gas | 3.30 | +2.36% |

| Bitcoin | 61,692.43 | +1.14% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 53.90 | 53.80 | 53.10 |

| S&P Global Services PMI Flash | 49.30 | 50.50 | 48.70 |

| BoE Breeden Speech | - | - | - |

| CBI Industrial Trends Orders | -41 | -35 | -45 |

| BoE Taylor Speech | - | - | - |

| BoE Dhingra Speech | - | - | - |

| BoE Breeden Speech | - | - | - |

| BoE Dhingra Speech | - | - | - |

| BoE Pill Speech | - | - | - |

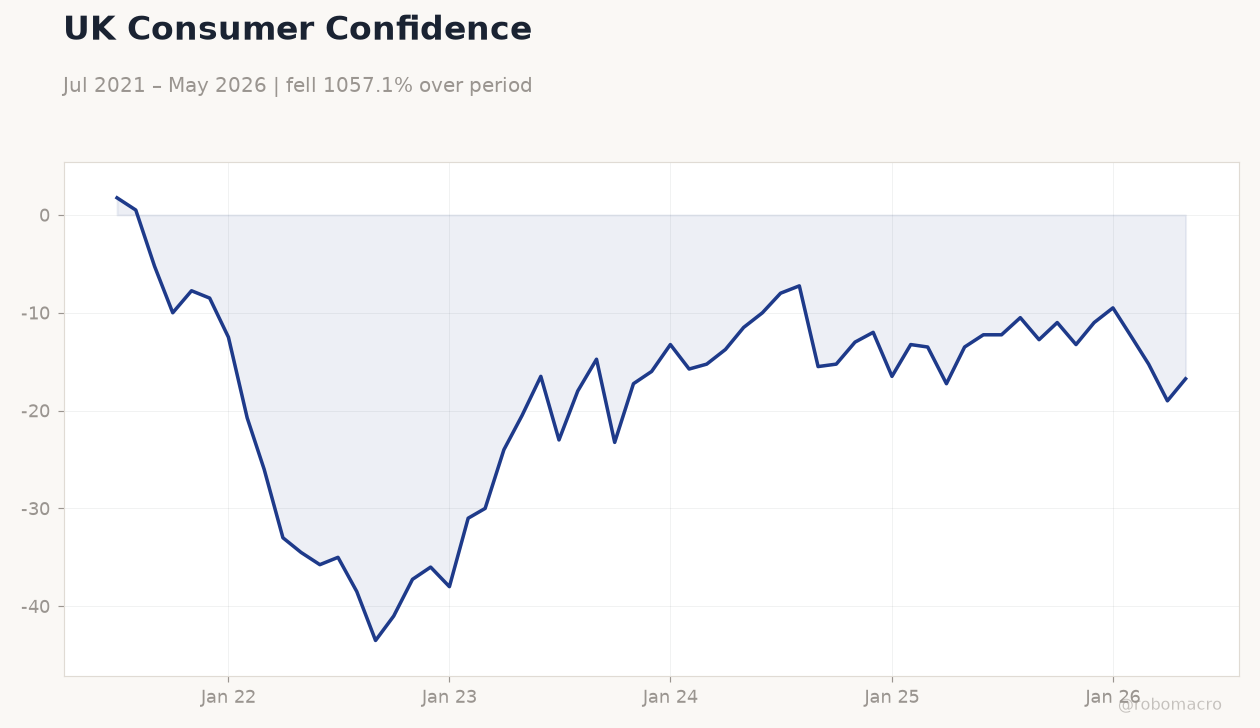

UK Consumer Confidence | Type: macro_line | Consumer Confidence Index: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

UK Consumer Confidence | Type: macro_line | Consumer Confidence Index: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| CBI Distributive Trades | -46 | -41 | 02:00 |

- S&P Global flash PMIs missed forecasts sharply, with manufacturing at 53.1 and services at 48.7, signalling contraction in services activity.

- CBI Industrial Trends Orders fell to -45, worse than the -35 consensus, highlighting softening industrial demand.

- FTSE 100 declined 0.22% while 10-year gilt yields rose 2.51% to 4.94%, reflecting risk-off sentiment.

Yesterday's Recap

UK flash PMIs disappointed on 23 June, with manufacturing at 53.1 against a 53.8 consensus and services activity contracting to 48.7 versus 50.5 expected. The CBI Industrial Trends Orders survey printed at -45, missing forecasts and the prior -41 reading. Multiple Bank of England speakers, including Breeden, Taylor and Dhingra, addressed audiences without altering near-term policy signals.

Sterling weakened 0.19% against the dollar to 1.32 while the FTSE 100 fell 0.22% to 10,438.78. The 10-year gilt yield climbed to 4.94%. Brent crude fell 1.17% to 72.88 amid softer global demand signals.

The Day Ahead

Markets will focus on the CBI Distributive Trades release at 02:00 ET, expected to improve to -41 from -46 and offering a timely gauge of consumer-facing demand. No other high-impact UK data are scheduled. MPC members Breeden, Dhingra and Pill are again due to speak, with attention on any fresh comments about inflation persistence.

Traders will monitor sterling crosses and gilt futures for positioning ahead of month-end flows.

Other Economic Notes

UK CPI remains at 3.40% year-on-year while unemployment sits at 4.90%, keeping the Bank of England on a cautious path with the Bank Rate at 3.73%. Recent company-level data cited by the Bank suggest Brexit has reduced UK output by around 6%, weighing on medium-term growth potential. A subdued growth outlook persists as services activity contracts and industrial orders deteriorate, limiting upside for domestic demand.

Gilt markets continue to reflect these dynamics through elevated term premia.

Global Macro News

European and US officials signalled closer alignment on security issues ahead of the NATO summit, supporting risk sentiment outside the UK. Brent crude extended losses below 75 dollars for the first time since the Middle East conflict ended, capping imported inflation pressures. Saudi Arabia’s latest sukuk issuance of 2.81 billion dollars showed continued appetite for Gulf debt, indirectly aiding sterling funding markets.

<i>↓ p.2</i>