UK Macro Daily(Beta Mode)

UK PMIs Weaken as 10Y Gilt Yield Climbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,461.60 | +0.31% |

| FTSE 250 | 23,064.58 | -0.42% |

| GBP/USD | 1.32 | +0.32% |

| GBP/EUR | 1.16 | -0.07% |

| GBP/JPY | 212.95 | -0.17% |

| Brent Crude | 73.42 | -2.44% |

| Gold | 4,048.50 | +0.45% |

| UK Nat Gas | 3.33 | -0.42% |

| Bitcoin | 60,179.23 | +0.77% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 53.90 | 53.80 | 53.10 |

| S&P Global Services PMI Flash | 49.30 | 50.50 | 48.70 |

| BoE Breeden Speech | - | - | - |

| CBI Industrial Trends Orders | -41 | -35 | -45 |

| BoE Taylor Speech | - | - | - |

| BoE Dhingra Speech | - | - | - |

| BoE Breeden Speech | - | - | - |

| BoE Dhingra Speech | - | - | - |

| BoE Pill Speech | - | - | - |

| CBI Distributive Trades | -46 | -41 | -54 |

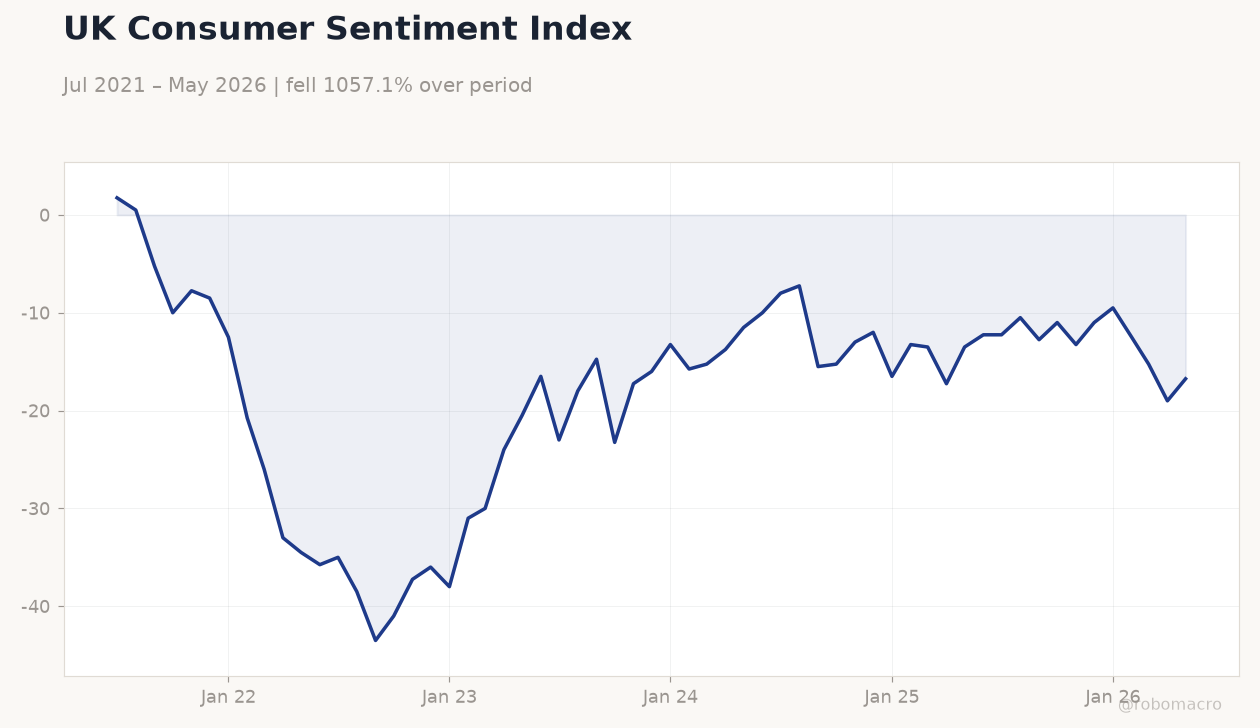

UK Consumer Sentiment Index | Type: macro_line | Sentiment Index: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

UK Consumer Sentiment Index | Type: macro_line | Sentiment Index: -16.75 (2026-05-01) | Range: -43.5–1.75 | Trend(6pt): 1.75,-43.5,-17.25,-16.5,-15.25,-16.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- S&P Global services PMI fell to 48.7 versus 50.5 consensus, while manufacturing printed 53.1 against 53.8 expected.

- CBI distributive trades and industrial trends orders both missed forecasts sharply, signalling weaker domestic demand.

- UK 10-year gilt yield rose 2.51% to 4.94% as sterling gained 0.32% against the dollar to 1.32.

Yesterday's Recap

UK flash PMIs released at 00:30 ET showed clear downside surprises. Services activity contracted more than forecast while manufacturing growth slowed. CBI industrial trends orders printed at -45 against -35 consensus, and distributive trades slumped to -54 versus -41 expected.

Multiple Bank of England speakers including Breeden, Taylor, Dhingra and Pill addressed audiences throughout the day. FTSE 100 rose 0.31% to 10,461.60 while the mid-cap FTSE 250 fell 0.42%. The 10-year gilt yield climbed sharply to 4.94% and Brent crude dropped 2.44% to 73.42.

Sterling posted modest gains across most crosses despite the soft data.

The Day Ahead

No high-impact UK data releases are scheduled for today. Markets will monitor follow-up commentary from yesterday’s BoE speakers for any fresh signals on the policy path. The Retail Payments Infrastructure Board consultation on next-generation payments infrastructure remains in focus following its launch.

Attention will also turn to any updates from the Prudential Regulation Authority annual report. Sterling and gilt curves are likely to stay sensitive to global risk sentiment given the empty domestic calendar.

Other Economic Notes

UK CPI inflation stands at 3.40% and unemployment at 4.90%, both consistent with a gradual cooling in price and labour-market pressures. The Bank Rate remains at 3.73%. Recent PMI weakness and softer CBI readings reinforce the view that domestic demand is losing momentum.

Gilt markets have priced limited further easing this year, with the 10-year yield reflecting both fiscal and inflation expectations. Housing and retail sales data due later in the month will provide the next concrete tests of consumer resilience.

Global Macro News

Iraq signalled possible OPEC exit unless its production quota rises, adding downside risk to Brent which already fell sharply. The Philippines, UAE and Indonesia will begin CPTPP accession talks, potentially expanding trade links that could affect UK services exports. <i>↓ p.2</i>