UK Macro Daily(Beta Mode)

Bailey: Rate Cuts Off the Table

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,478.30 | -0.18% |

| FTSE 250 | 23,188.80 | -0.61% |

| GBP/USD | 1.33 | +0.64% |

| GBP/EUR | 1.17 | +0.64% |

| GBP/JPY | 215.23 | -0.12% |

| Brent Crude | 71.10 | -0.66% |

| Gold | 4,086.10 | +0.44% |

| UK Nat Gas | 3.18 | -1.27% |

| Bitcoin | 60,038.47 | +0.06% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoE Pill Speech | - | - | - |

| BoE Consumer Credit | 1,713m | 1,800m | 1,662m |

| Mortgage Approvals | 66,030 | 62,900 | 56,210 |

| Mortgage Lending Level | 4,440m | 4,600m | 2,890m |

| Nationwide Housing Prices Month-over-Month | -0.60 | 0 | 0 |

| Nationwide Housing Prices Year-over-Year | 1.70 | 2.40 | 2.20 |

| BoE Gov Bailey Speech | - | - | - |

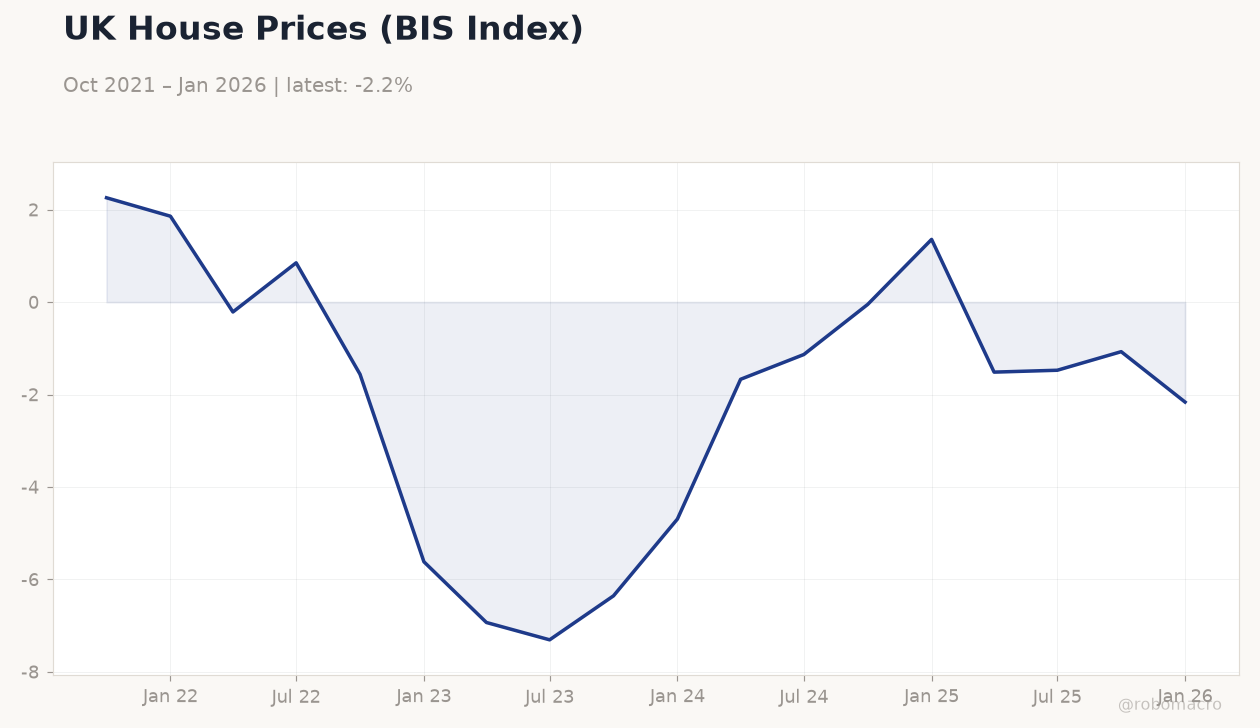

UK House Prices (BIS Index) | Type: macro_line | Index Level: -2.163 (2026-01-01) | Range: -7.308–2.258 | Trend(6pt): 2.258,-1.561,-6.356,-0.04994,-1.072,-2.163

UK House Prices (BIS Index) | Type: macro_line | Index Level: -2.163 (2026-01-01) | Range: -7.308–2.258 | Trend(6pt): 2.258,-1.561,-6.356,-0.04994,-1.072,-2.163

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoE Mann Speech | - | - | 07:45 |

| Friday (2026-07-03) | |||

| BoE Gov Bailey Speech | - | - | 07:00 |

- BoE Governor Bailey stated rate cuts remain off the table, citing persistent inflation pressures and incomplete household impact from prior tightening.

- UK housing data showed mixed signals with Nationwide prices flat month-over-month while mortgage approvals and lending fell sharply below consensus.

- Sterling strengthened against the dollar and euro as gilt yields rose, with FTSE 100 declining modestly amid global equity divergence.

Yesterday's Recap

UK data releases highlighted cooling housing activity. Mortgage approvals dropped to 56,210 from 66,030 prior, while net mortgage lending fell to £2.89bn against £4.6bn expected. Consumer credit also missed at £1.662bn.

Nationwide house prices rose 2.2% year-over-year, below the 2.4% consensus, though the monthly reading printed flat at 0%. BoE Governor Bailey delivered remarks confirming that rate reductions are not under consideration given current inflation dynamics. Markets responded with the 10-year gilt yield climbing 2.51% to 4.94% and GBP/USD advancing 0.64% to 1.33.

The FTSE 100 closed 0.18% lower at 10,478.30.

The Day Ahead

Markets will focus on BoE Deputy Governor Catherine Mann’s speech scheduled for 07:45 ET. No major data releases are due today, leaving policy rhetoric as the primary driver. Investors will parse Mann’s comments for any divergence from Bailey’s recent stance on holding the 3.73% Bank Rate.

Sterling crosses and gilt futures are expected to remain sensitive to forward guidance signals. Attention will also turn to Friday’s repeat Bailey appearance for further confirmation on the policy path.

Other Economic Notes

UK CPI stands at 3.4% year-over-year while unemployment has risen to 4.9%, pointing to a labour market that is easing but still tight enough to support wage pressures. The BoE continues quantitative tightening by shrinking its balance sheet and shifting toward a demand-driven reserve system. Housing weakness may feed into lower consumption, yet the committee has shown no inclination to adjust policy settings in the near term.

Gilt yields have risen in tandem with the hawkish rhetoric, supporting sterling.