UK Macro Daily(Beta Mode)

BoE Holds Firm as Lending Data Weaken

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,673.43 | +0.19% |

| FTSE 250 | 23,538.80 | +0.52% |

| GBP/USD | 1.34 | +0.59% |

| GBP/EUR | 1.17 | +0.01% |

| GBP/JPY | 215.48 | -0.16% |

| Brent Crude | 72.13 | +0.46% |

| Gold | 4,187.30 | +1.81% |

| UK Nat Gas | 3.24 | +1.53% |

| Bitcoin | 62,099.49 | +1.00% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.94% | +2.51% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoE Pill Speech | - | - | - |

| BoE Consumer Credit | 1,713m | 1,800m | 1,662m |

| Mortgage Approvals | 66,030 | 62,900 | 56,210 |

| Mortgage Lending Level | 4,440m | 4,600m | 2,890m |

| Nationwide Housing Prices Month-over-Month | -0.60 | 0 | 0 |

| Nationwide Housing Prices Year-over-Year | 1.70 | 2.40 | 2.20 |

| BoE Gov Bailey Speech | - | - | - |

| BoE Mann Speech | - | - | - |

| BoE Gov Bailey Speech | - | - | - |

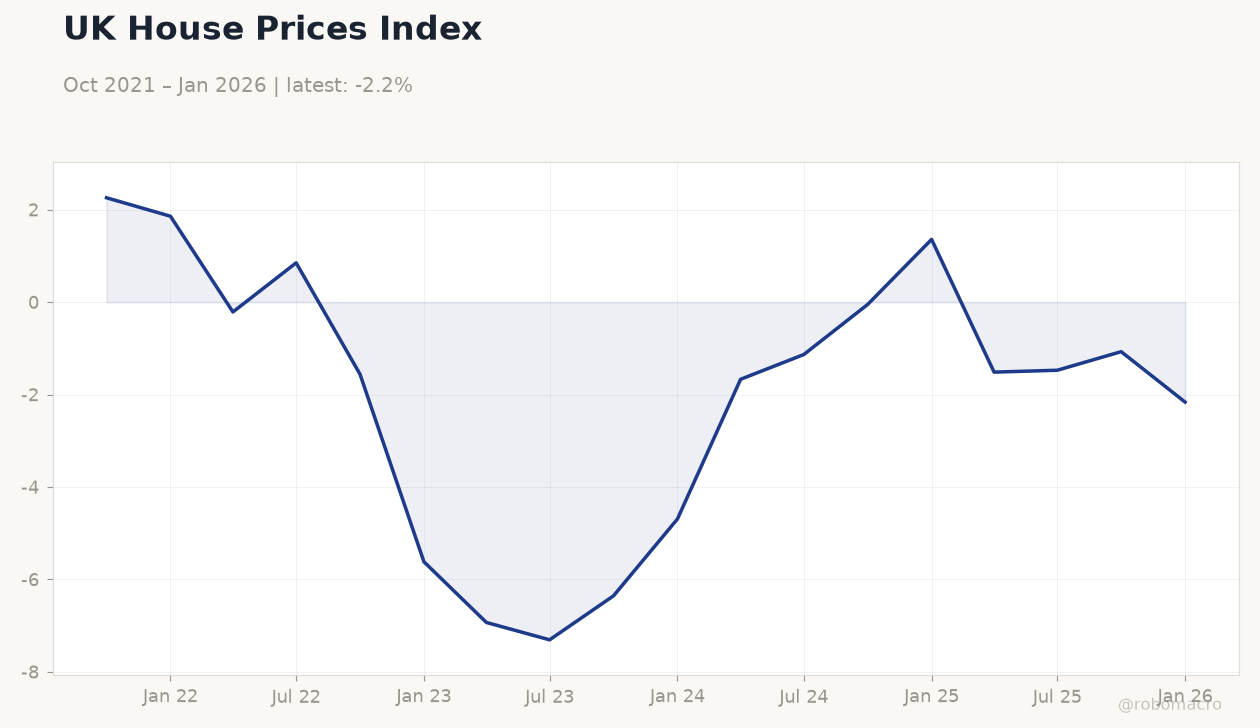

UK House Prices Index | Type: macro_line | Index: -2.163 (2026-01-01) | Range: -7.308–2.258 | Trend(6pt): 2.258,-1.561,-6.356,-0.04994,-1.072,-2.163

UK House Prices Index | Type: macro_line | Index: -2.163 (2026-01-01) | Range: -7.308–2.258 | Trend(6pt): 2.258,-1.561,-6.356,-0.04994,-1.072,-2.163

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- BoE signals no near-term rate cuts despite softer mortgage approvals and consumer credit.

- UK 10-year gilt yields rise to 4.94% as markets adjust to delayed easing.

- FTSE 100 edges up 0.19% while sterling strengthens against the dollar on relative policy stability.

Yesterday's Recap

UK mortgage approvals fell to 56,210 in May, missing the 62,900 consensus, while net mortgage lending dropped sharply to £2.89 billion against £4.6 billion expected. Consumer credit also undershot at £1.662 billion. Nationwide house prices rose 2.2% year-over-year, below the 2.4% forecast, though the monthly reading was flat.

BoE Governor Bailey and MPC members Pill and Mann delivered speeches that reinforced the committee’s decision to hold the 3.73% Bank Rate. Markets showed limited reaction, with the FTSE 100 closing at 10,673.43 and the 10-year gilt yield climbing 2.51% to 4.94%. GBP/USD advanced to 1.34 on the day.

The Day Ahead

Governor Bailey is scheduled to speak again at 07:00 ET, providing further clarity on the inflation outlook. No fresh data releases are listed for the UK today. Markets will monitor any comments on the 3.40% CPI reading and the 4.90% unemployment rate for signs of policy flexibility.

Sterling crosses and gilt futures are expected to remain sensitive to forward guidance. Traders continue to price the first cut later than previously anticipated.

Other Economic Notes

UK financial stability faces growing risks from climate-related exposures according to recent BoE assessments. Persistent above-target inflation at 3.40% continues to anchor policy, limiting scope for near-term easing. Fiscal authorities have reiterated commitment to existing borrowing rules without additional debt issuance.

Housing market momentum remains subdued following the latest Nationwide figures.

Global Macro News

The US economy added only 57,000 jobs in June, prompting a retreat in the dollar index and supporting GBP/USD. Saudi crude exports have returned toward pre-war levels, capping Brent upside despite the 0.46% daily gain to $72.13. Mexico and Canada are seeking alternatives after US officials declined to renew USMCA.

Tesla’s European sales recovery highlights uneven demand across advanced economies. <i>↓ p.2</i>