UK Macro Weekly

UK Demand Shock: Retail and Consumer Sentiment Collapse

Market Scorecard (Weekly Change)

| Asset | Fri Close | Week Chg |

|---|---|---|

| FTSE 100 | 10,846.70 | +2.07% |

| FTSE 250 | 23,719.00 | +0.93% |

| GBP/USD | 1.350 | 0.00% |

| GBP/EUR | 1.140 | 0.00% |

| GBP/JPY | 209.98 | +0.59% |

| Brent Crude | 71.32 | -0.47% |

| Gold | 5,204.80 | +4.60% |

| UK Nat Gas | 2.84 | -5.33% |

| Bitcoin | 67,682.60 | n/a |

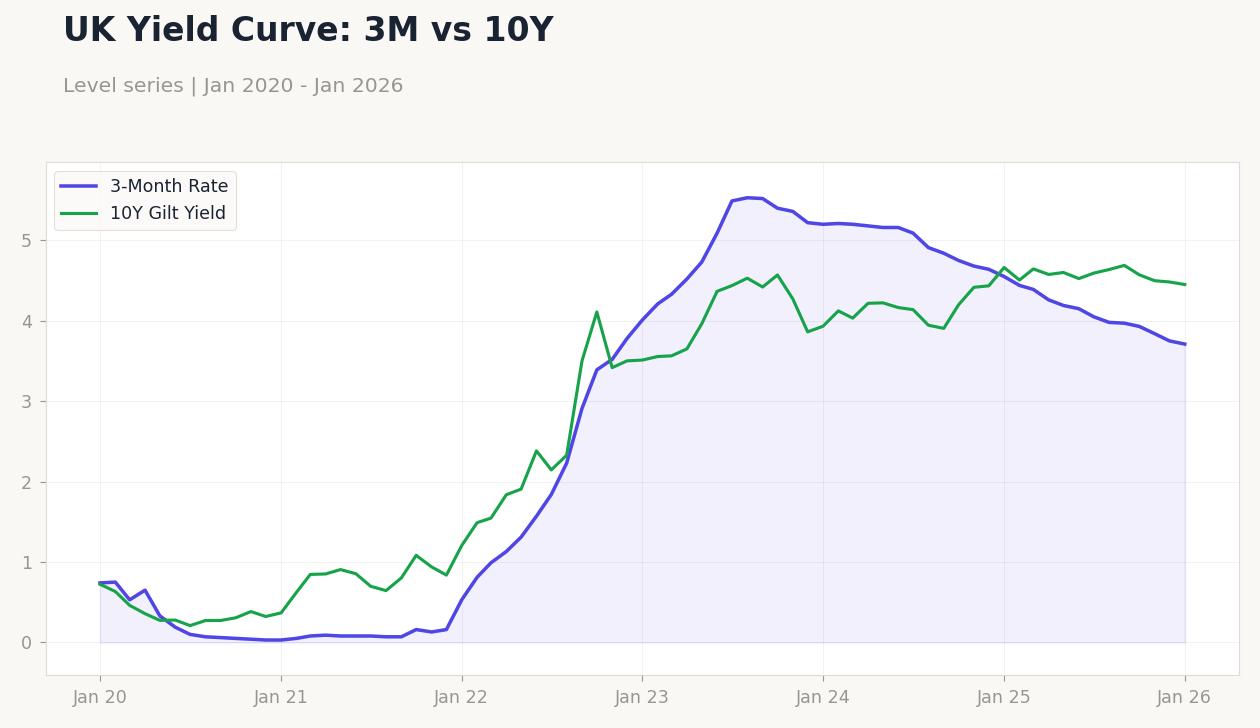

| UK 10Y Gilt | 4.45% | unch |

Prior Economic Events (Feb 23–27)

| Day | Event | Prior | Cons | Actual |

|---|---|---|---|---|

| Tuesday, Feb 24 | ||||

| CBI Distributive Trades | -17 | -16 | -43 | |

| Thursday, Feb 26 | ||||

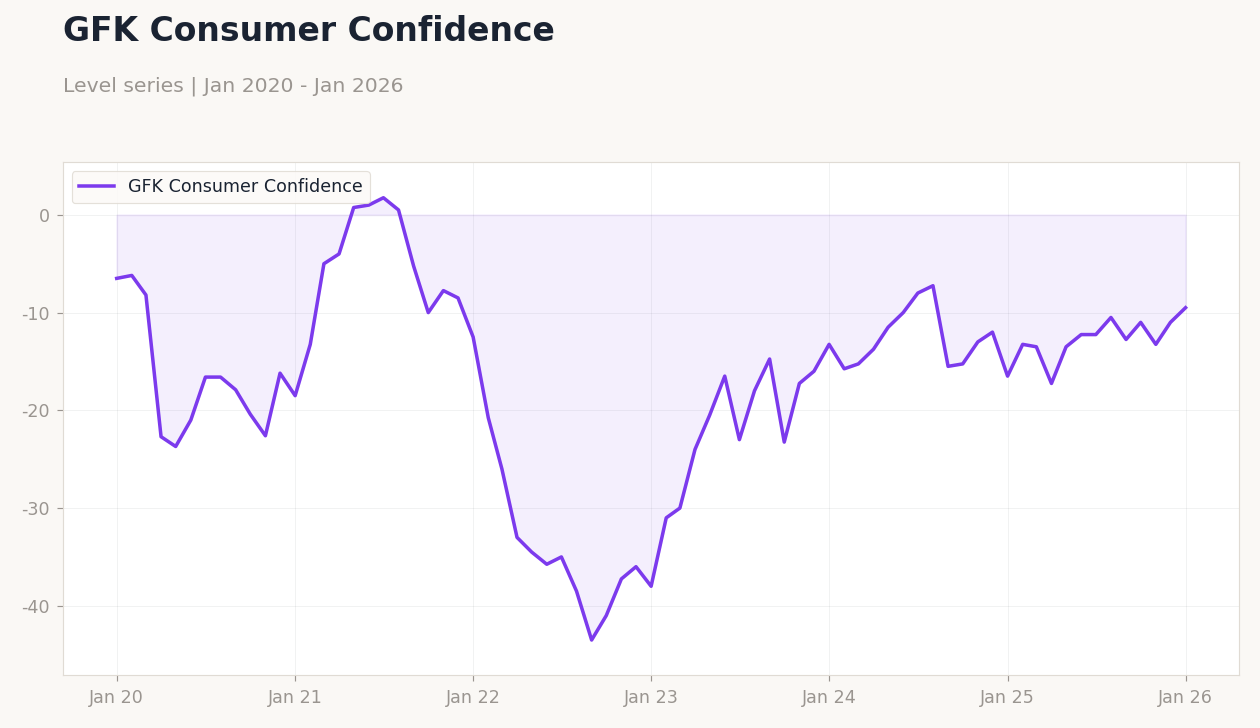

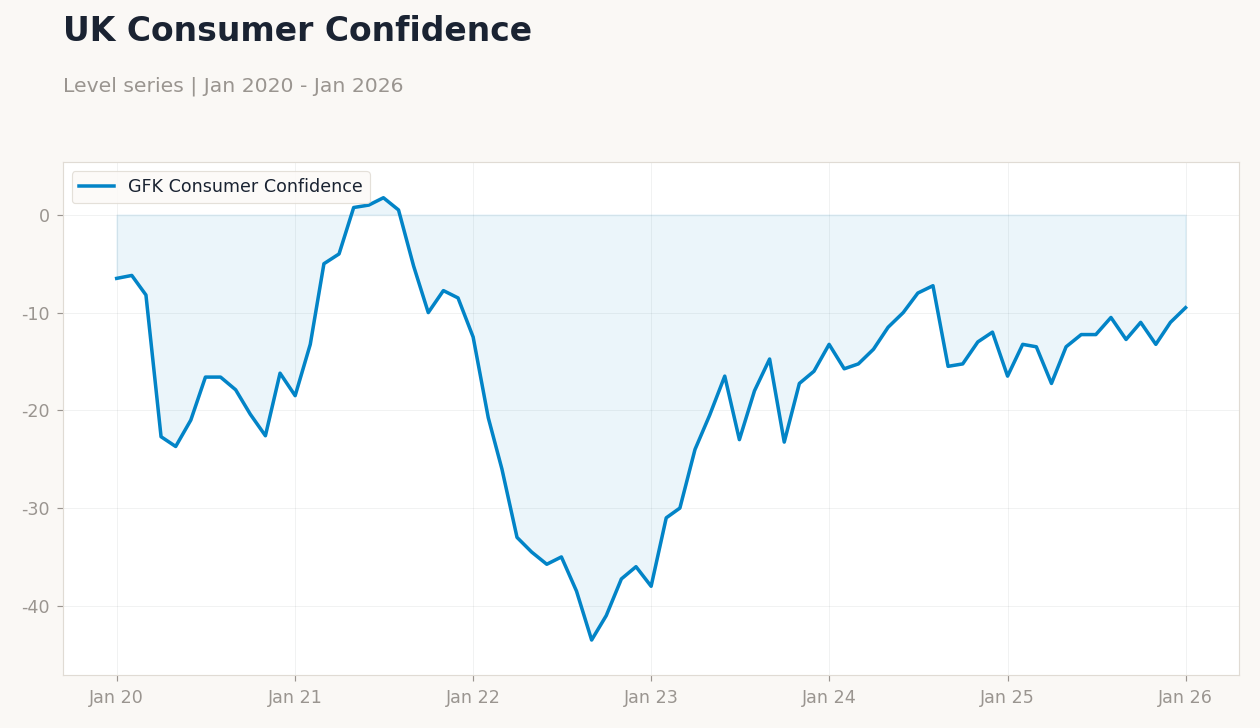

| GFK Consumer Confidence | -16 | -15 | -19 | |

Surprises & Misses

CBI Distributive Trades: -27pt miss

Worst reading since pandemic era. Retail volumes collapsed amid inflation fatigue and cost-of-living pressures. The magnitude of the miss suggests a step-change in consumer behaviour, not merely a seasonal dip.

GFK Consumer Confidence: -4pt miss

Fell to -19 vs -15 expected. All five sub-indices deteriorated. Major purchase intentions declined sharply, suggesting households are deferring spending.

Chart of the Week

- CBI Distributive Trades collapsed to -43 (vs -16 consensus), the worst reading since the pandemic, signalling acute retail distress from inflation and weak demand.

- GFK Consumer Confidence fell to -19 (vs -15 expected), confirming broad-based sentiment deterioration across households.

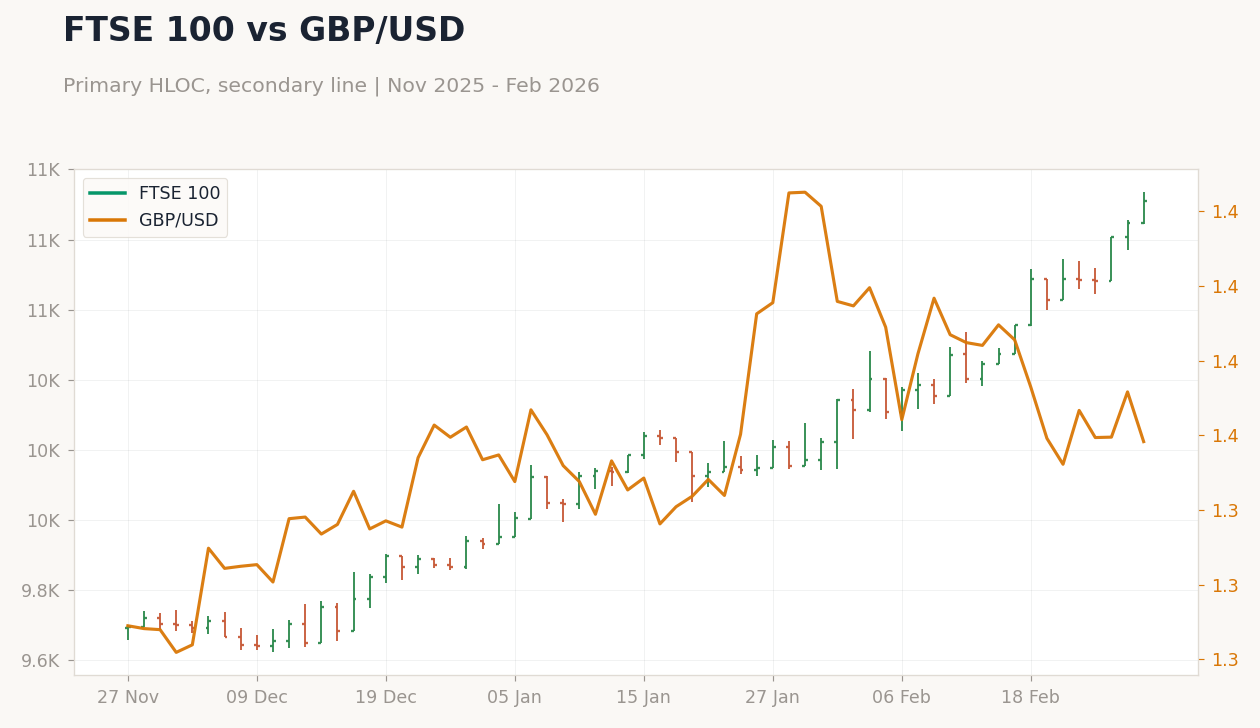

- FTSE 100 rallied 2.1% despite the domestic data miss, carried by US tech spillovers and defensive sector rotation — a stark sentiment-equity divergence.

- Sterling ended the week flat against USD but weakened 0.60% vs EUR and 0.84% vs JPY on Friday, as markets repriced BoE easing expectations.

- Next week: Nationwide Housing Prices, Mortgage Approvals, and Construction PMI — the housing complex will test whether demand weakness is spreading beyond retail.

Week in Review

The week's narrative was dominated by a stark divergence: UK sentiment indicators crumbled while equities rallied on external tailwinds. The CBI Distributive Trades survey set the tone on Tuesday, plunging to -43 in February — a 27-point miss against consensus of -16 and the weakest reading since the pandemic lockdowns. Retailers cited elevated cost pressures, subdued footfall, and cautious consumer behaviour as the primary drivers. Thursday's GFK Consumer Confidence Index compounded the picture, falling to -19 against expectations of -15, with households flagging concerns over inflation persistence and job security.

Yet the FTSE 100 appeared to operate in a parallel universe, gaining 2.1% across the week to close at 10,846.70. Thursday's 1.18% surge — the largest single-day gain of the week — was driven by global equity momentum from US tech earnings rather than any domestic catalyst. The FTSE 250, more exposed to the domestic economy, managed a more modest 0.93% gain. Sterling told a different story: after a brief mid-week recovery, GBP/USD ended flat at 1.35 while GBP/EUR slipped 0.60% on Friday alone, reflecting the dovish repricing of BoE expectations as the soft data accumulated. The 10Y Gilt yield held steady at 4.45%, with buyers and sellers reaching an uneasy equilibrium between safe-haven demand and the BoE's still-restrictive 3.75% rate.