US Macro Daily(Beta Mode)

Labor Data Mixed, Cuts Steady

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,878.70 | +0.09% |

| Nasdaq | 23,505.14 | +0.22% |

| Spot VIX | 15.80 | -1.74% |

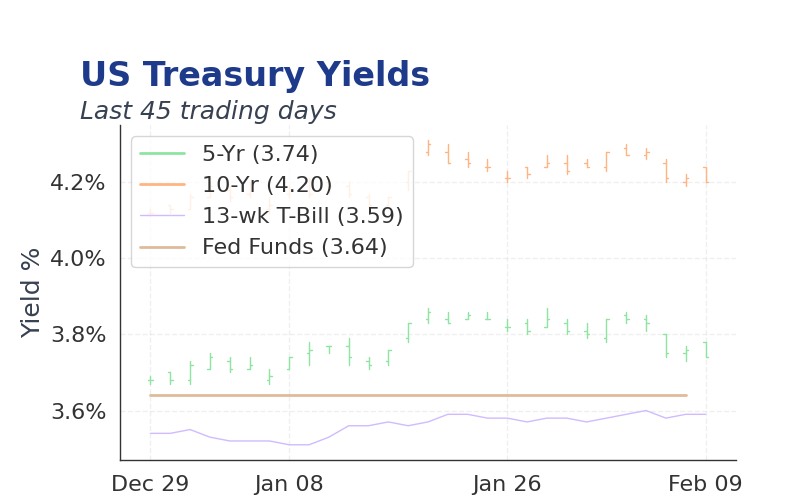

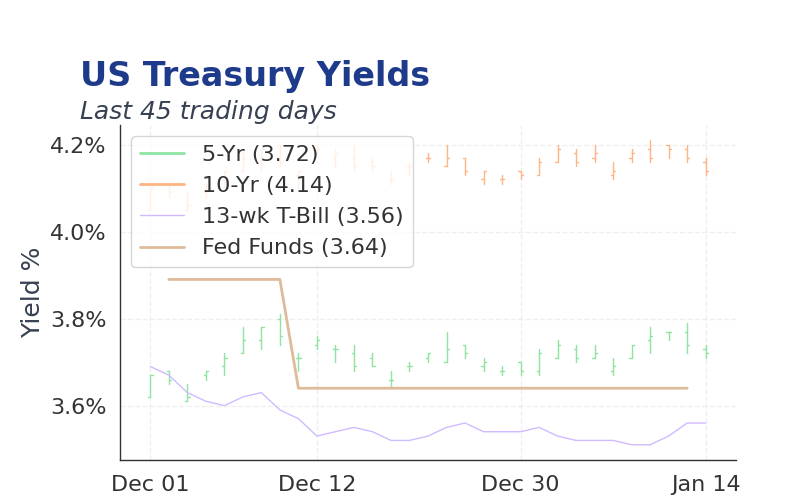

| 2 Year Bond Yield | 3.53 | +3 bps |

| 10 Year Bond Yield | 4.10 | +4 bps |

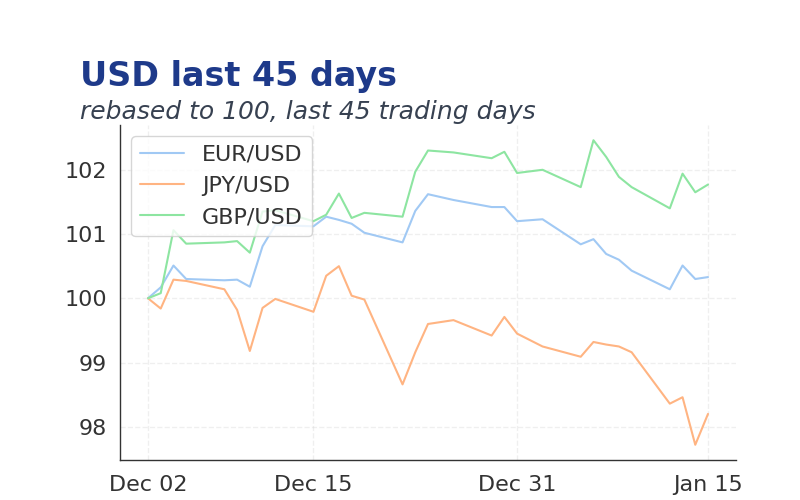

| EUR/USD | 1.1642 | -0.02% |

| USD/JPY | 155.13 | +0.02% |

| GBP/USD | 1.333 | -0.02% |

| WTI Oil | Data Unavailable | Data Unavailable |

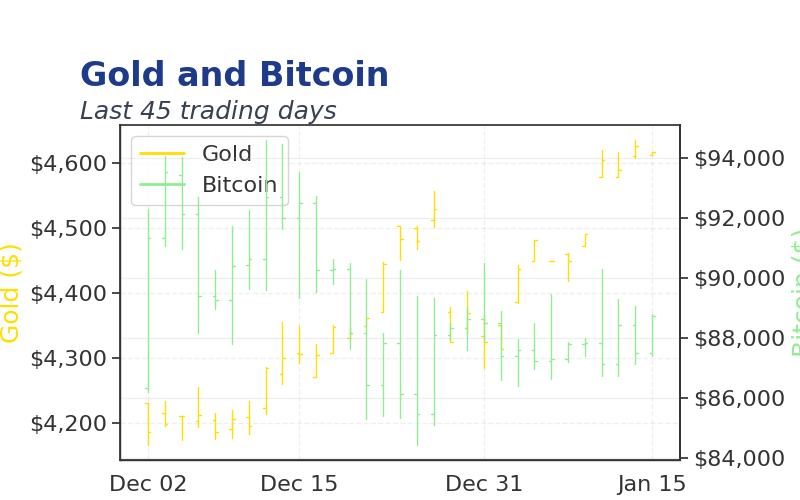

| Gold | 4,208.37 | +0.12% |

| Bitcoin | 92,421.77 | -1.11% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| MBA 30-Year Mortgage Rate | 6.40 | - | 6.32 |

| ADP Employment Change | 47,000 | 10,000 | -32,000 |

| Export Prices Month-over-Month | 0.10 | 0.10 | 0 |

| Import Prices Month-over-Month | 0.10 | 0.10 | 0 |

| Industrial Production Month-over-Month | -0.30 | 0 | 0.10 |

| Services Sector PMI | 52.40 | 52.10 | 52.60 |

| EIA Weekly Crude Oil Inventory | 2.8m | -800,000 | 574,000 |

| EIA Weekly Gasoline Inventory | 2.5m | 1.5m | 4.5m |

| Weekly Jobless Claims | 218,000 | 220,000 | 191,000 |

| Factory Orders Month-over-Month | 1.30 | 0.50 | 0.20 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Federal Reserve Balance Sheet | 6550m | - | 16:30 |

| Michigan Consumer Sentiment Prel | - | - | 10:00 |

| Core PCE Price Index Month-over-Month | 0.20 | 0.20 | 10:00 |

| Personal Income Month-over-Month | 0.40 | 0.40 | 10:00 |

| Personal Spending Month-over-Month | 0.60 | 0.40 | 10:00 |

| PCE Price Index Month-over-Month | 0.30 | 0.30 | 10:00 |

| PCE Price Index Year-over-Year | 2.70 | 2.80 | 10:00 |

- ADP payrolls plunged 32k unexpectedly, signaling labor market contraction amid 'no hire, no fire' trends.

- Today's PCE inflation data could guide Fed's pace, with consensus at 0.3% m/m.

- Fuel economy rollback boosts auto sector but risks higher emissions and inflation.

Yesterday's Recap

ADP employment change fell sharply to -32k, missing consensus of 10k and prior 47k, highlighting unexpected private sector job losses that weighed on equity sentiment.

Weekly jobless claims dropped to 191k, beating consensus of 220k and prior 218k, indicating resilient labor demand despite broader weaknesses.

Industrial production edged up 0.1% m/m, slightly above consensus of 0% and prior -0.3%, suggesting mild manufacturing recovery.

Services PMI rose to 52.6, surpassing consensus of 52.1 and prior 52.4, pointing to expansion in non-manufacturing sectors.

EIA crude oil inventories increased 574k barrels, exceeding consensus draw of 800k, while gasoline stocks surged 4.52M against 1.5M expected.

Mortgage rates dipped to 6.32%, below prior 6.4%, aiding housing affordability.

Markets traded calmly, with S&P 500 at 6878.70, Nasdaq at 23505.14, VIX at 15.80, 2-year yield at 3.53%, 10-year at 4.10%, EUR/USD at 1.1642, USD/JPY at 155.13, GBP/USD at 1.333, gold at 4208.37, and bitcoin at 92421.77. (cont...)