US Macro Daily(Beta Mode)

Fed Cuts Amid Divisions

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,909.20 | +0.64% |

| Nasdaq | 23,654.16 | +0.33% |

| Spot VIX | 16.12 | +2.22% |

| 2 Year Bond Yield | 3.55 | -1 bps |

| 10 Year Bond Yield | 4.14 | -1 bps |

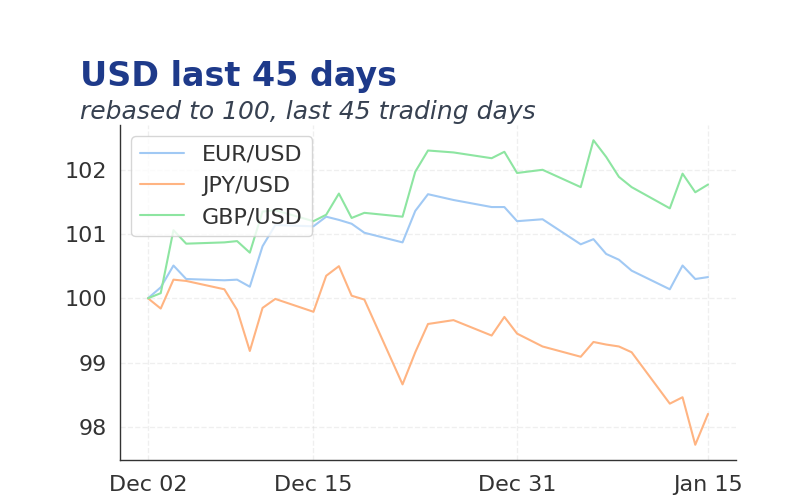

| EUR/USD | 1.1717 | +0.19% |

| USD/JPY | 155.77 | -0.10% |

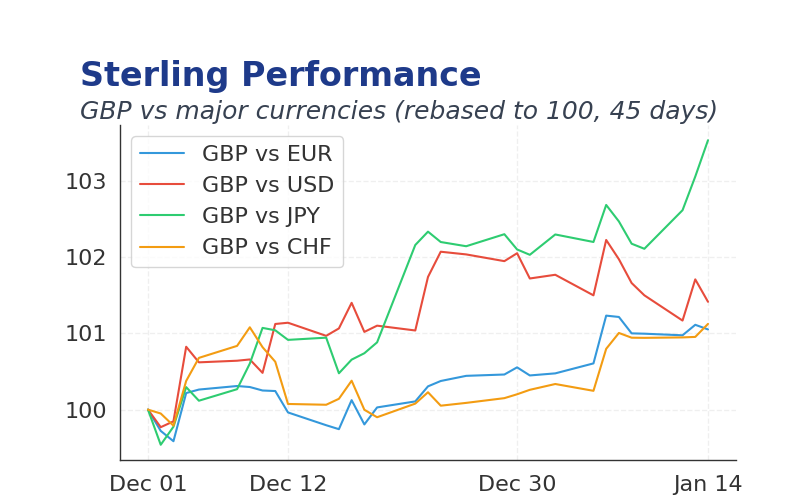

| GBP/USD | 1.338 | -0.01% |

| WTI Oil | 58.25 | -1.07% |

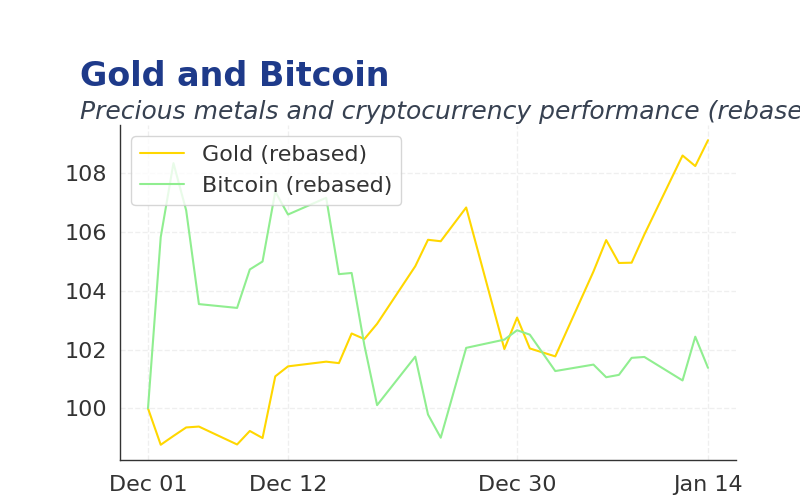

| Gold | 4,215.09 | -0.25% |

| Bitcoin | 90,281.62 | -1.90% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| MBA 30-Year Mortgage Rate | 6.32 | - | 6.33 |

| Employment Cost - Benefits Quarter-over-Quarter | 0.70 | - | 0.80 |

| Employment Cost - Wages Quarter-over-Quarter | 1 | - | 0.80 |

| Employment Cost Index Quarter-over-Quarter | 0.90 | 0.90 | 0.80 |

| EIA Weekly Crude Oil Inventory | 574,000 | -2.3m | -1.8m |

| EIA Weekly Gasoline Inventory | 4.5m | 2.8m | 6.4m |

| Fed Interest Rate Decision | 4 | 3.75 | 3.75 |

| FOMC Economic Projections | - | - | - |

| Monthly Budget Statement | -284m | -205m | -173m |

| Fed Press Conference | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | -59.6m | -63.3m | 08:30 |

| Exports Level | 280.8m | - | 08:30 |

| Imports Level | 340.4m | - | 08:30 |

| Weekly Jobless Claims | 191,000 | 220,000 | 08:30 |

| Federal Reserve Balance Sheet | 6540m | - | 16:30 |

| Speech by Fed's Paulson | - | - | 08:00 |

| Fed Hammack Speech | - | - | 08:30 |

| Fed Goolsbee Speech | - | - | 10:35 |

- Fed delivers third 25bps rate cut to 3.5-3.75%, but divided FOMC signals pause with one 2026 cut projected amid labor cooling.

- Today's trade balance and jobless claims could sway easing bets as tariff inflation looms.

- Global debt nears $346T, heightening refinancing risks and boosting stablecoin regulatory focus.

Yesterday's Recap

Employment costs rose 0.8% QoQ for benefits and wages, beating prior readings, while the index missed consensus at 0.8% versus 0.9%.

EIA crude inventories drew 1.8M barrels, less than 2.3M expected, with gasoline stocks building 6.4M versus 2.8M.

Fed cut rates in 9-3 vote, Powell highlighting labor softening and tariff inflation peaks in Q1, projecting one 2026 cut.

Equities gained, S&P 500 up 0.67% to 6,886.68, VIX at 16.12.

Bond yields fell, 2-year to 3.55% and 10-year to 4.14%, USD weakening against EUR to 1.1717 and JPY to 155.77.

Commodities held steady, WTI oil at 58.25, gold at 4,215.09, bitcoin at 90,281.62.

The Day Ahead

Trade balance expected at -$63.3B versus -$59.6B prior, with exports at 280.8B and imports at 340.4B at 8:30am.

Weekly jobless claims forecast at 220K versus 191K previous.

Fed speeches from Paulson at 8am, Hammack at 8:30am, Goolsbee at 10:35am may refine cut timing.

Federal Reserve balance sheet update at 4:30pm. (cont...)