US Macro Daily(Beta Mode)

Stocks Sink on Chip Retreat

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,851.70 | -1.07% |

| Nasdaq | 23,195.17 | -1.69% |

| Spot VIX | 16.44 | +10.71% |

| 2 Year Bond Yield | 3.52 | -1 bps |

| 10 Year Bond Yield | 4.17 | -1 bps |

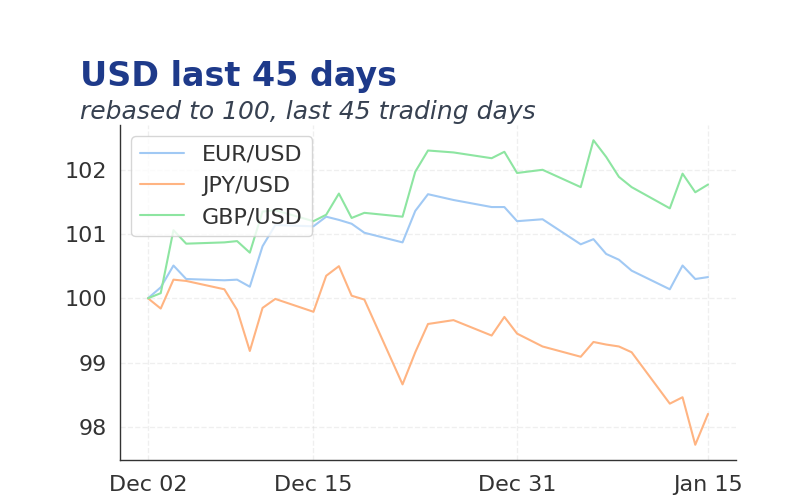

| EUR/USD | 1.1739 | -0.01% |

| USD/JPY | 155.88 | +0.18% |

| GBP/USD | 1.337 | -0.20% |

| WTI Oil | 57.60 | -1.47% |

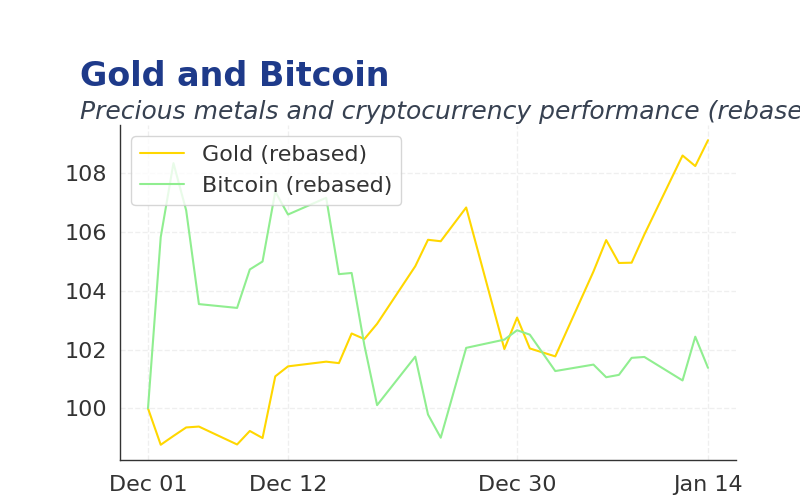

| Gold | 4,339.47 | +0.96% |

| Bitcoin | 90,207.40 | -0.08% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NY Empire State Manufacturing Index | 18.70 | 10 | 08:30 |

| Speech by Fed's Miran | - | - | 09:30 |

| NAHB Housing Market Index | 38 | 38 | 10:00 |

| Speech by Fed's Williams | - | - | 10:30 |

| ADP Employment Change Weekly | 4,750 | - | 08:15 |

| Payroll Jobs Growth | 119,000 | - | 08:30 |

| Payroll Jobs Growth | - | 40,000 | 08:30 |

| Retail Sales Month-over-Month | 0.20 | 0.20 | 08:30 |

| Headline Unemployment Rate | 4.40 | 4.40 | 08:30 |

| Monthly Wage Growth | 0.20 | - | 08:30 |

- Broadcom's disappointing sales outlook sparked a -11% plunge, dragging chip stocks lower and pressuring tech-heavy Nasdaq.

- Upcoming payrolls data at 8:30am expected at 40K versus 119K prior, with unemployment rate steady at 4.4%, signaling potential labor market shifts.

- Hawkish Fed comments from Goolsbee and Schmid pushed 10-year yields up 3.5bps to 4.192%, amid debates over rate cut pace in the easing cycle.

Friday's Recap

Equities sold off sharply, with S&P 500 closing at 6851.70 down 1.07%, Nasdaq at 23195.17 down 1.91%, and Dow at -0.51%, as Broadcom's missed sales outlook fueled a chip sector retreat exceeding 1σ volatility thresholds.

Bond yields climbed, 10-year rising 3.5bps to 4.17% and 2-year up to 3.52%, driven by hawkish Fed dissent on inflation risks.

FX held steady with EUR/USD at 1.1739 and GBP/USD at 1.337, while USD/JPY ticked to 155.88 on balanced flows.

Commodities edged higher, WTI oil at 57.60 up from prior levels and gold at 4339.47, supported by supply concerns.

Bitcoin fell to 90207.40, reflecting crypto weakness amid broader market pressures.

The Day Ahead

ADP Employment Change at 08:15 expected at consensus levels versus prior 4750, will gauge private-sector hiring trends.

Payroll Jobs Growth at 08:30 projected at 40K versus 119K previous, alongside Unemployment Rate at 4.4% and Monthly Wage Growth, may influence Fed cut bets.

NY Empire State Manufacturing Index at 08:30 consensus 10 versus 18.70 prior, Retail Sales at 0.2%, and NAHB Housing Market Index at 38, will assess economic momentum. (cont...)