US Macro Daily(Beta Mode)

Fed Cuts Steady Amid Calm Data

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,878.30 | +0.63% |

| Nasdaq | 23,428.83 | +0.52% |

| Spot VIX | 14.11 | +0.21% |

| 2 Year Bond Yield | 3.50 | -1 bps |

| 10 Year Bond Yield | 4.15 | -2 bps |

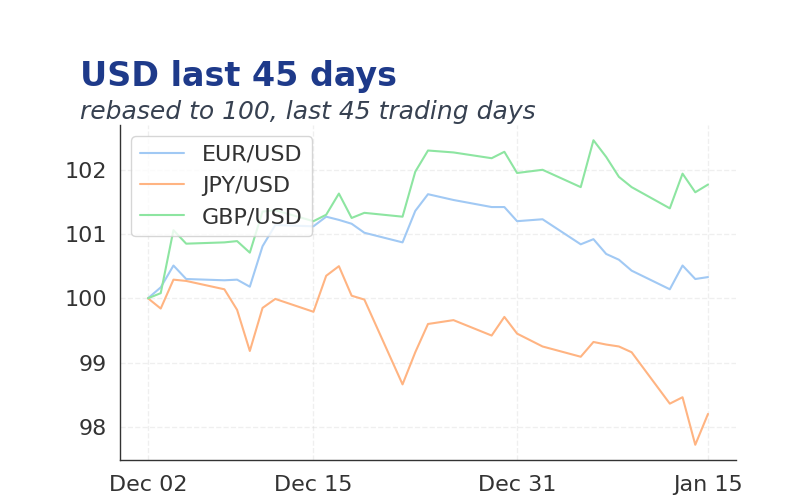

| EUR/USD | 1.1798 | +0.36% |

| USD/JPY | 155.90 | -0.70% |

| GBP/USD | 1.351 | +0.38% |

| WTI Oil | 56.66 | +0.91% |

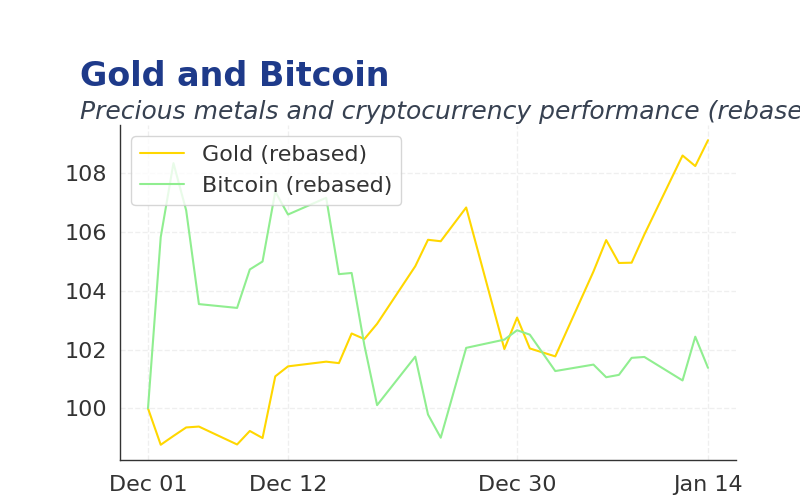

| Gold | 4,483.74 | +0.87% |

| Bitcoin | 87,655.31 | -1.01% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Chicago Fed National Activity Index | -0.31 | - | -0.21 |

| Ny Fed Bill Purchases 4 To 12 Months | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Durable Goods Orders Month-over-Month | 0.50 | -1.50 | 08:30 |

| GDP Growth Quarter-over-Quarter Second Estimate | 3.80 | 3.30 | 08:30 |

| Corporate Profits Quarter-over-Quarter Prel | 0.20 | - | 08:30 |

| Durable Goods Orders Ex Transp Month-over-Month | 0.60 | 0.30 | 08:30 |

| GDP Price Index Quarter-over-Quarter 2nd Est | 2.10 | - | 08:30 |

| Industrial Production Month-over-Month | 0.10 | 0.10 | 09:15 |

| Industrial Production Month-over-Month | - | - | 09:15 |

| Cb Consumer Confidence | 88.70 | - | 10:00 |

| Richmond Fed Manufacturing Index | -15 | -7 | 10:00 |

| Richmond Fed Manufacturing Shipments Index | -14 | - | 10:00 |

- Chicago Fed index improved, signaling modest US economic resilience.

- Markets traded calmly with low volatility, supporting equities.

- Upcoming GDP revision eyes further rate cut confirmation.

Yesterday's Recap

Equities edged higher, with the S&P 500 closing at 6,878.30 and Nasdaq at 23,428.83, reflecting steady investor sentiment in a low-volatility environment.

Bond yields ticked down modestly, with the 10-year at 4.15% and 2-year at 3.50%, as rate cut expectations tempered inflation concerns.

FX saw the USD weaken against EUR to 1.1798 and GBP to 1.351, while strengthening slightly against JPY to 155.90 amid geopolitical flows.

Commodities advanced, with WTI oil at $56.66, gold hitting $4,483.74 on safe-haven demand, and Bitcoin at $87,655.31 consolidating gains.

The Chicago Fed National Activity Index rose to -0.21 from -0.31, beating expectations and hinting at underlying growth stability.

The Day Ahead

Durable Goods Orders at 8:30am are expected at -1.5% versus 0.5% prior, potentially revealing manufacturing pressures.

GDP Q3 2nd Estimate at 8:30am forecast at 3.3% annualized against 3.8%, with price index and corporate profits providing inflation and earnings context.

Industrial Production and CB Consumer Confidence at 9:15am and 10:00am will assess labor and spending trends.

Richmond Fed Manufacturing Index at 10:00am expected at -7 versus -15 prior, eyeing regional recovery signals. (cont...)