Yesterday's Recap

Q3 GDP expanded at a surprising 4.3% annualized rate, surpassing the 3.0% consensus and up from 3.8% in Q2, fueled by resilient consumer spending that rose to a 3.5% pace.

Consumer confidence slumped to 89.1 in December, the lowest in nearly four years, with expectations for income and jobs deteriorating amid tariff fears.

Initial jobless claims fell to 214,000, beating estimates of 223,000, signaling labor market stability despite broader uncertainties.

Markets closed higher on Wednesday, with the S&P 500 at 6,933.90 and Nasdaq at 23,613.31 in calm conditions, while VIX stood at 14.16.

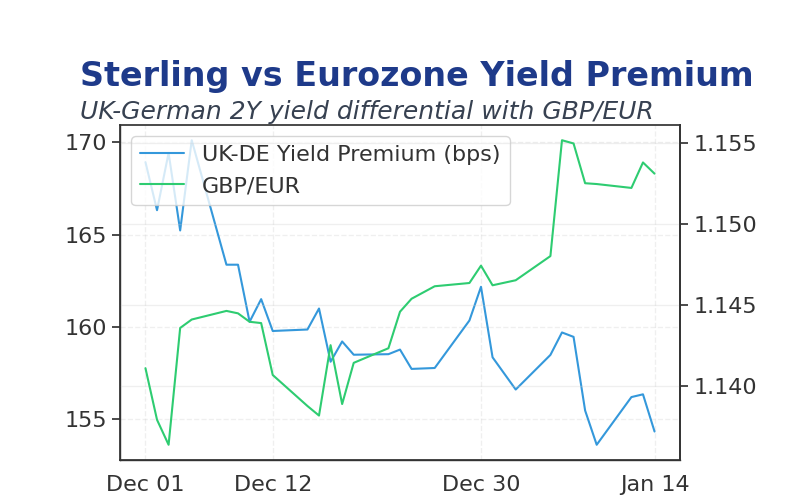

Bond yields held steady, with 2-year at 3.51% and 10-year at 4.14%, as rate cut expectations tempered moves.

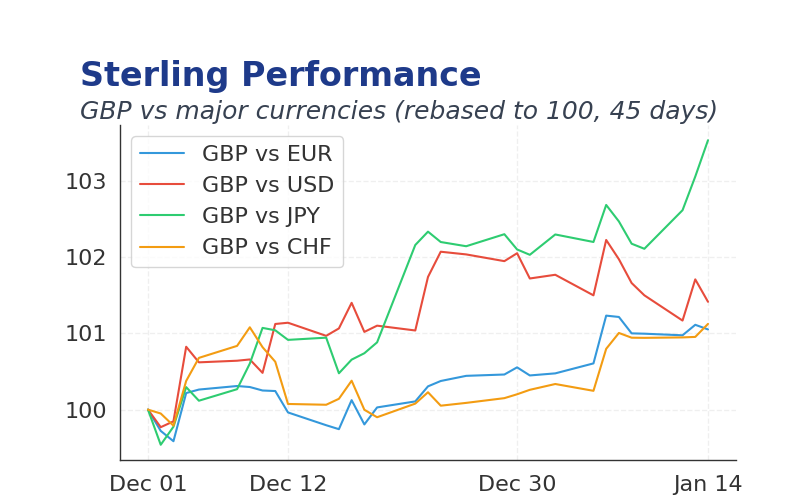

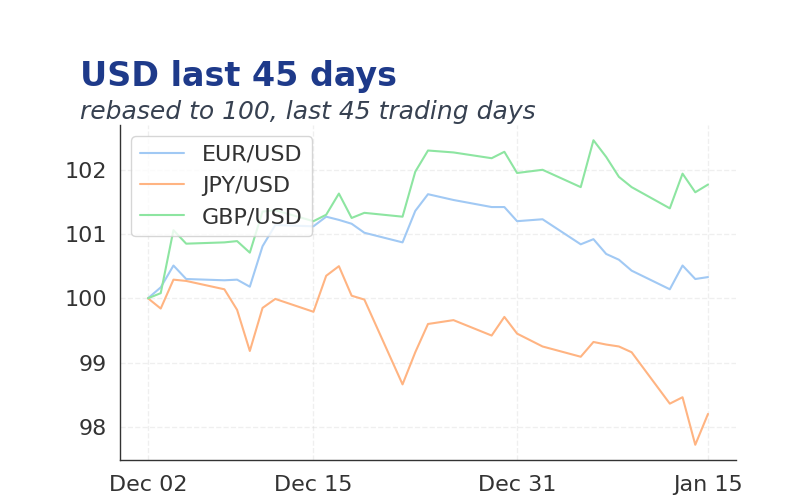

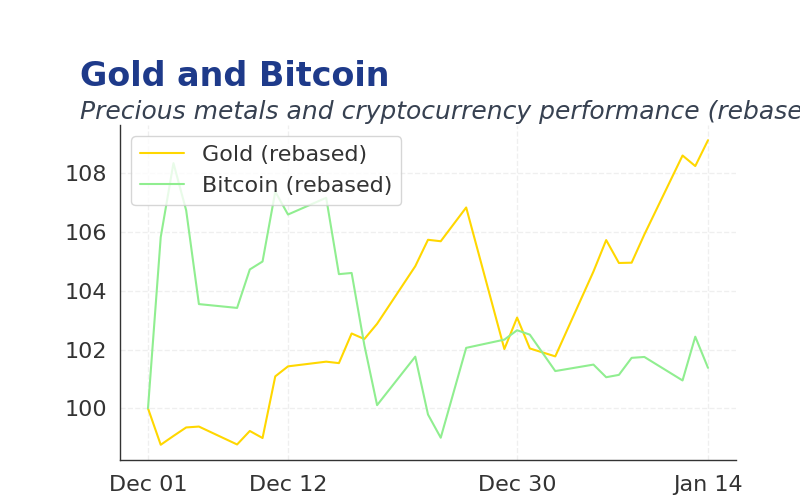

FX showed EUR/USD at 1.1780 and USD/JPY at 156.36, with commodities like gold rising to 4,514.87 and WTI oil at 58.38. (cont...)