US Macro Daily(Beta Mode)

Data Beats Amid Cuts

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,909.10 | -0.34% |

| Nasdaq | 23,474.35 | -0.50% |

| Spot VIX | 14.58 | +2.68% |

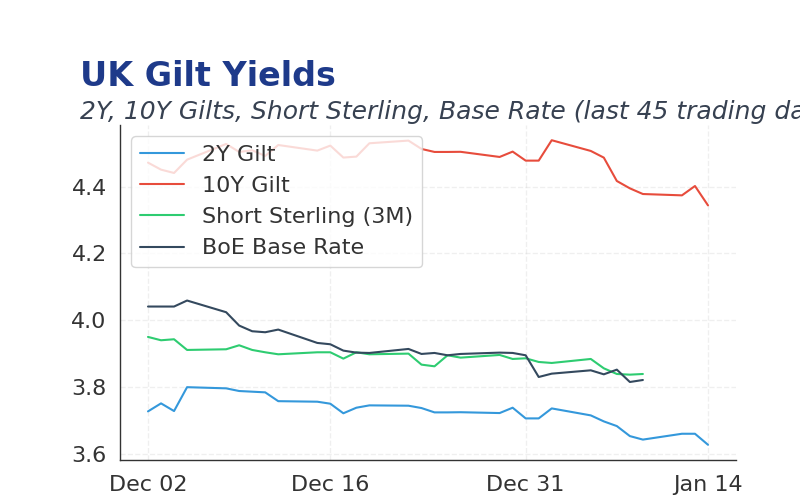

| 2 Year Bond Yield | 3.47 | +3 bps |

| 10 Year Bond Yield | 4.12 | +1 bps |

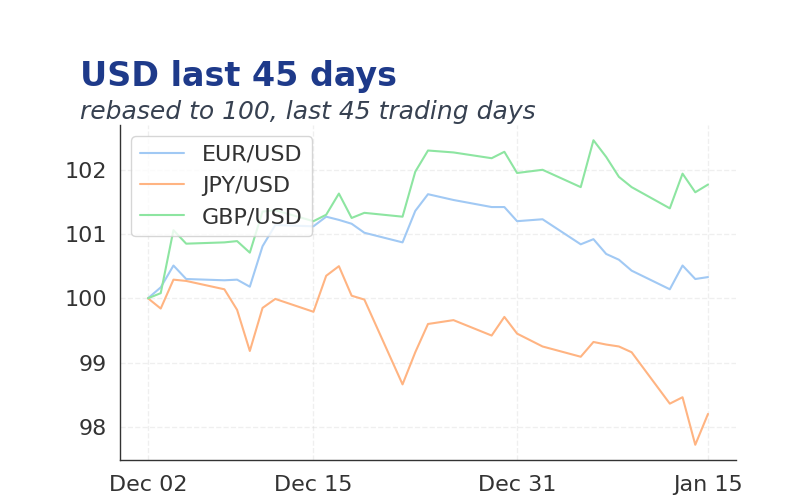

| EUR/USD | 1.1773 | +0.03% |

| USD/JPY | 155.87 | -0.13% |

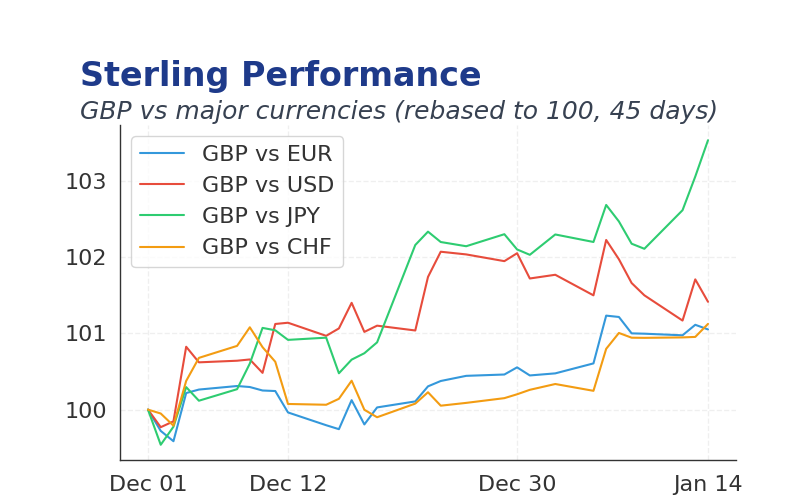

| GBP/USD | 1.351 | +0.08% |

| WTI Oil | 56.74 | 0.00% |

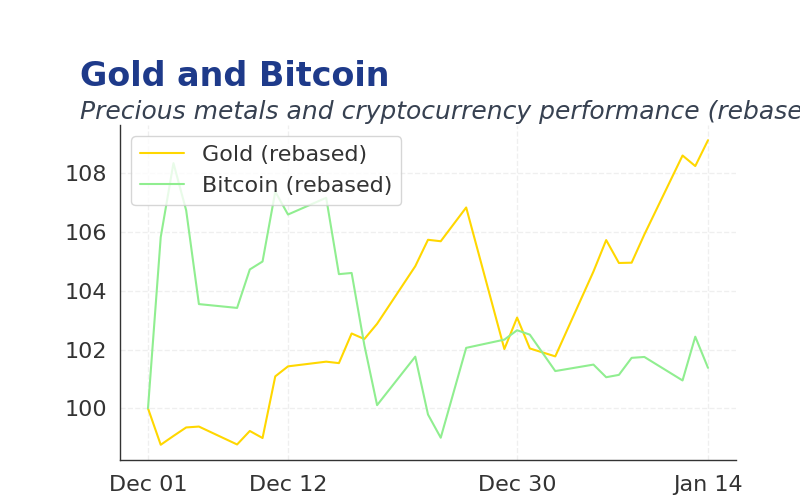

| Gold | 4,389.19 | +1.30% |

| Bitcoin | 87,811.25 | +0.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Pending Home Sales Month-over-Month | 2.40 | 1 | 3.30 |

| Pending Home Sales Year-over-Year | -0.40 | - | 2.60 |

| Dallas Fed Manufacturing Index | -10.40 | - | -10.90 |

| EIA Weekly Crude Oil Inventory | -1.3m | -2.4m | - |

| EIA Weekly Gasoline Inventory | 4.8m | 1.1m | - |

| EIA Weekly Crude Oil Inventory | -1.3m | -2.4m | - |

| EIA Weekly Gasoline Inventory | 4.8m | 1.1m | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P/Case-Shiller Home Price Year-over-Year | 1.40 | 1.10 | 09:00 |

| Chicago PMI | 36.30 | 39.50 | 09:45 |

| Dallas Fed Services Index | -2.30 | - | 10:30 |

| Dallas Fed Services Revenues Index | -2.50 | - | 10:30 |

| FOMC Meeting Minutes | - | - | 14:00 |

| API Weekly Crude Oil Stocks | 2.4m | - | 16:30 |

| MBA 30-Year Mortgage Rate | 6.31 | - | 07:00 |

| Weekly Jobless Claims | 214,000 | 220,000 | 08:30 |

| EIA Weekly Crude Oil Inventory | 405,000 | -2m | 10:30 |

| EIA Weekly Gasoline Inventory | 2.9m | 1.1m | 10:30 |

- Pending home sales surged 3.3% in November, well above consensus, signaling housing resilience despite affordability strains.

- Global tensions over Venezuela's oil disruptions boosted gold to record highs, reflecting safe-haven demand.

- FOMC minutes today may clarify rate cut timing, with markets pricing slower easing in 2025.

Yesterday's Recap

Pending home sales climbed to 3.3% month-over-month, beating the 1.0% consensus and underscoring housing market strength amid stable mortgage rates.

Dallas Fed manufacturing index slipped to -10.9, worsening from -10.4 and highlighting ongoing factory challenges.

EIA crude oil inventories data was inconclusive, with gasoline stocks also showing mixed signals, contributing to subdued commodity volatility.

Markets traded calmly with VIX at 14.58, S&P 500 holding at 6909.10, and bond yields stable at 4.12% for 10-year Treasuries.

FX showed EUR/USD at 1.1773 and USD/JPY at 155.87, while gold rose to 4389.19 and WTI oil at 56.74.

Bitcoin edged up to 87811.25 in low-volatility conditions.

The Day Ahead

S&P/Case-Shiller home price index at 9:00 AM ET may confirm housing trends, with consensus at 1.1% year-over-year.

Chicago PMI at 9:45 AM ET, expected at 39.5, could gauge manufacturing recovery amid global trade pressures.

FOMC meeting minutes at 2:00 PM ET will reveal Fed views on rate cut pace, potentially influencing yield expectations.

EIA weekly inventories at 10:30 AM ET, forecasted at -2.0 million barrels, may drive oil prices higher. (cont...)