US Macro Daily(Beta Mode)

Data Tilts Hawkish on Cuts

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,953.20 | +0.26% |

| Nasdaq | 23,530.02 | +0.25% |

| Spot VIX | 15.50 | -2.15% |

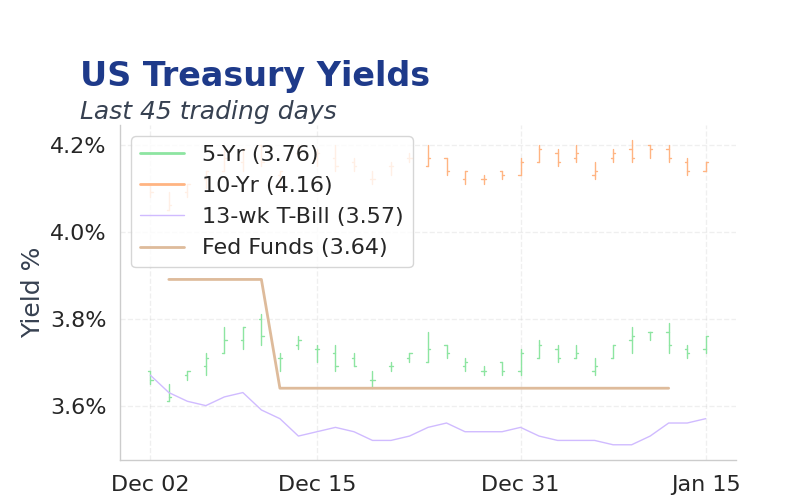

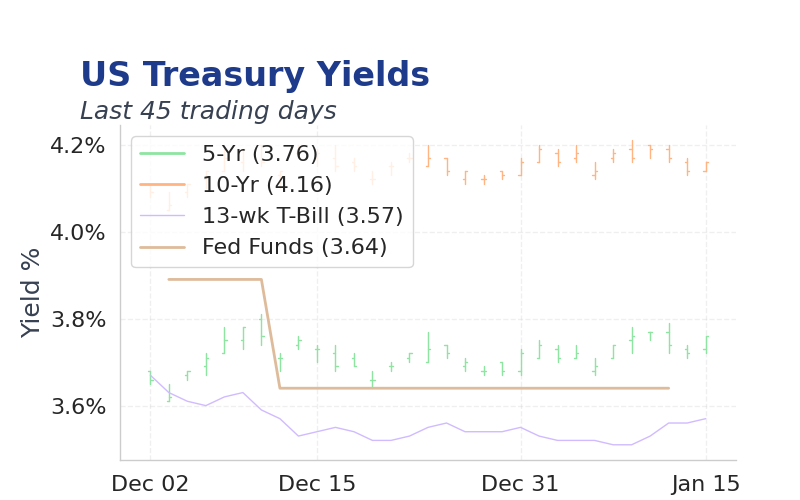

| 2 Year Bond Yield | 3.57 | -0 bps |

| 10 Year Bond Yield | 4.17 | -0 bps |

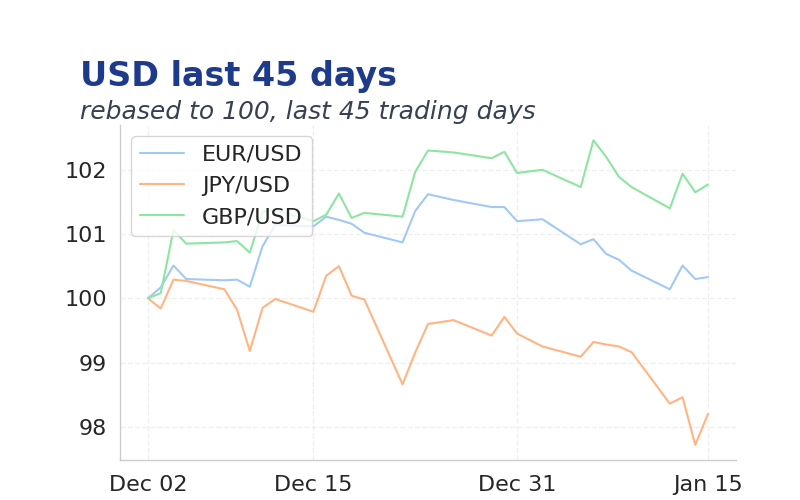

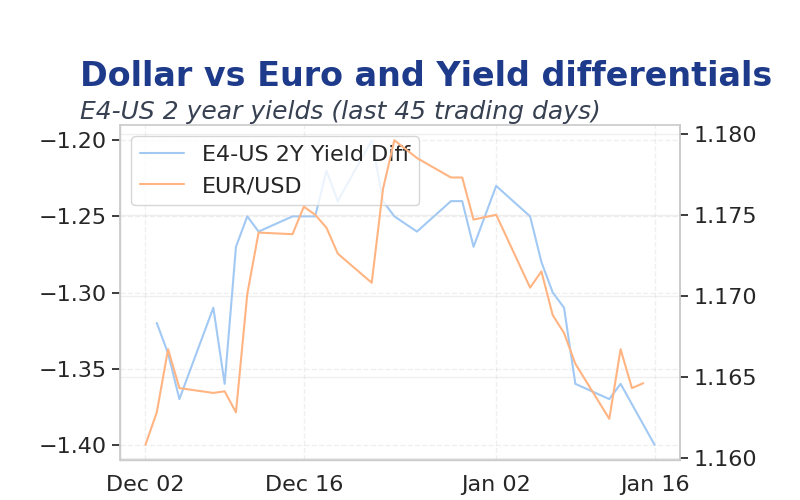

| EUR/USD | 1.1620 | +0.14% |

| USD/JPY | 158.09 | -0.35% |

| GBP/USD | 1.341 | +0.23% |

| WTI Oil | 62.02 | +1.42% |

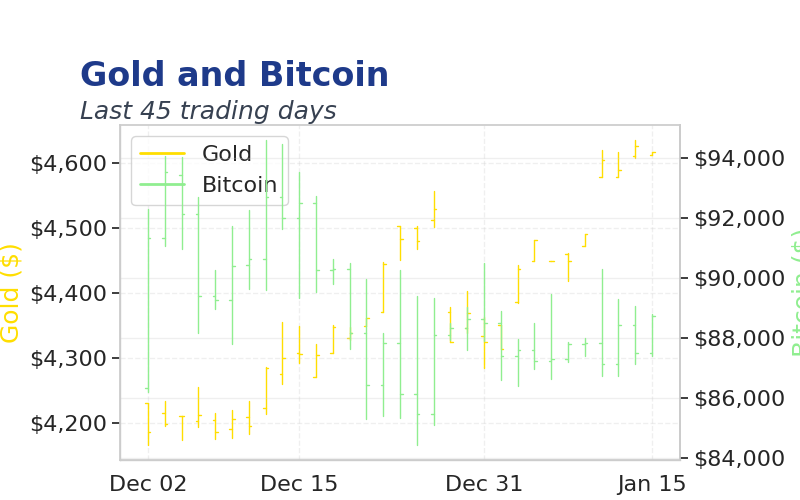

| Gold | 4,609.92 | -0.12% |

| Bitcoin | 95,283.74 | -0.31% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NY Fed Services Activity Index | -20 | - | 08:30 |

| Industrial Production Month-over-Month | 0.20 | 0.10 | 09:15 |

| NAHB Housing Market Index | 39 | 40 | 10:00 |

| Speech by Fed's Bowman | - | - | 11:00 |

| Speech by Fed's Jefferson | - | - | 15:30 |

- Retail sales beat expectations with 0.6% m/m rise, signaling resilient consumer demand despite high rates.

- Cathie Wood forecasts US economic boom in 2026, citing deregulation and productivity gains.

- Oil prices steadied below $60 amid easing Iran tensions, while Bitcoin slipped on regulatory hurdles.

Yesterday's Recap

Retail sales surged 0.6% m/m, exceeding the 0.4% consensus and highlighting robust consumer spending across ex-autos and control groups.

Producer prices moderated, with PPI at 0.1% and core PPI flat, easing upstream inflation pressures.

The current account deficit narrowed to -$226.4B from -$249.2B, better than the -$238.4B estimate, reflecting stronger trade balances.

Fed's Paulson reiterated data-dependent policy, offering no new rate cues amid mixed economic signals.

Markets traded calmly, with the S&P 500 up 0.26% to 6944.47, VIX at 15.50, and 10-year yields steady at 4.17%.

The Day Ahead

NY Fed Services Activity Index at 8:30am is expected to show modest improvement, with consensus at -20.0.

Industrial Production at 9:15am may rise 0.1% m/m, matching forecasts at 0.1%, gauging manufacturing momentum.

Fed's Bowman and Jefferson speak at 11:00am and 3:30pm respectively, potentially clarifying data influences on rate paths.