US Macro Daily(Beta Mode)

Markets Steady Amid Data Calm

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,946.60 | -0.09% |

| Nasdaq | 23,515.39 | -0.06% |

| Spot VIX | 19.29 | +21.63% |

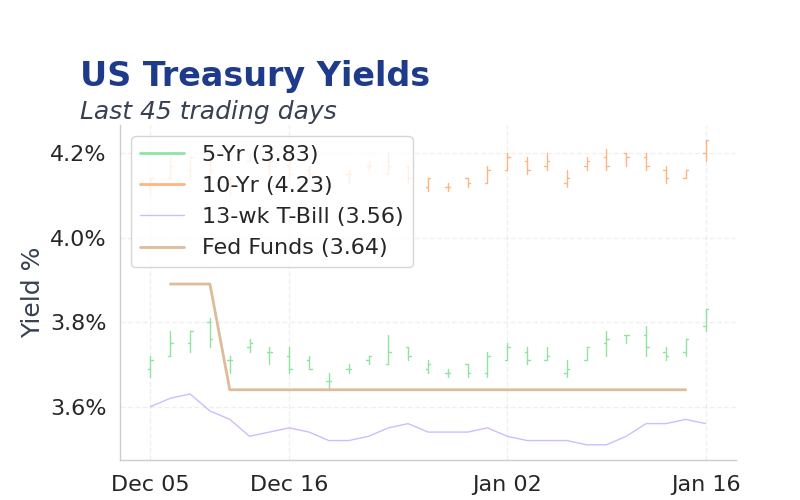

| 2 Year Bond Yield | 3.59 | +2 bps |

| 10 Year Bond Yield | 4.23 | +5 bps |

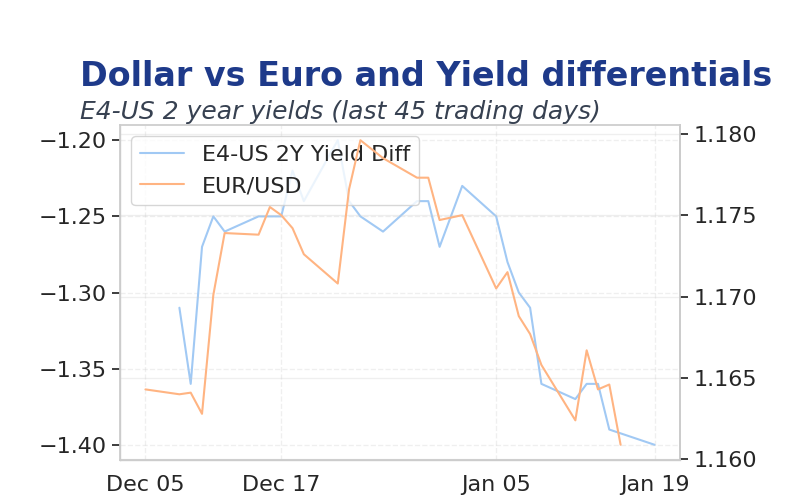

| EUR/USD | 1.1622 | +0.19% |

| USD/JPY | 157.99 | -0.06% |

| GBP/USD | 1.341 | +0.19% |

| WTI Oil | 59.19 | -4.56% |

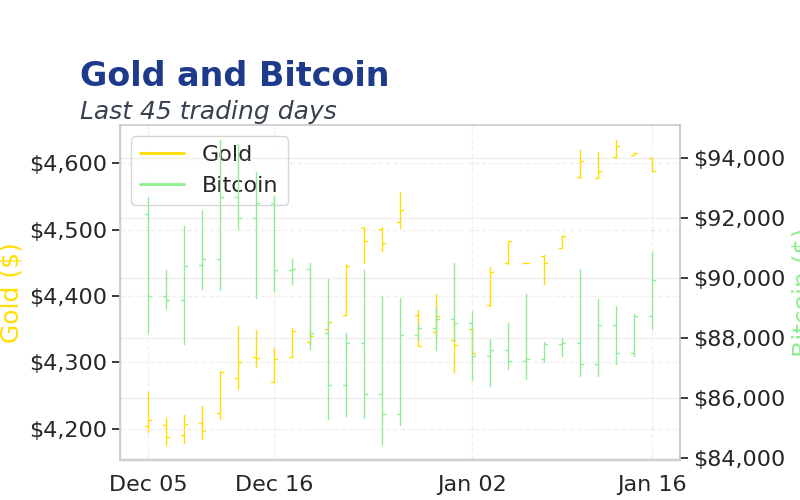

| Gold | 4,665.64 | +1.54% |

| Bitcoin | 93,051.19 | -0.62% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ADP Employment Change Weekly | 11,750 | - | 08:15 |

| API Weekly Crude Oil Stocks | 5.3m | - | 16:30 |

- ADP employment rose to 11,750, surpassing expectations and signaling labor market resilience.

- Geopolitical tensions in Iran and Venezuela eased, stabilizing oil prices below $60.

- Yields edged higher as Fed chair uncertainty lingered, with VIX at 19.29 reflecting mild volatility.

Friday's Recap

ADP employment change came in at 11,750, beating the consensus estimate, indicating continued strength in the labor market despite ongoing rate cuts.

API weekly crude oil stocks data showed a draw of 5.27M barrels, aligning with expectations and supporting steady oil prices around $59.

Markets traded calmly overall, with the S&P 500 dipping 0.1% to 6946.60 and Nasdaq down 0.1% to 23515.39, as investors digested mixed economic signals.

Bond yields rose modestly, with the 2-year up to 3.59% and 10-year to 4.23%, amid Fed chair speculation.

The USD firmed against the euro at 1.1622 and yen at 157.99, while gold climbed to 4665.64 and Bitcoin held at 93051.19.

No major Fed speeches yesterday, but prior comments reinforced data-dependent easing. (cont...)