US Macro Daily(Beta Mode)

Tariff Threats Dampen Markets

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,946.60 | -0.09% |

| Nasdaq | 23,515.39 | -0.06% |

| Spot VIX | 20.17 | +27.18% |

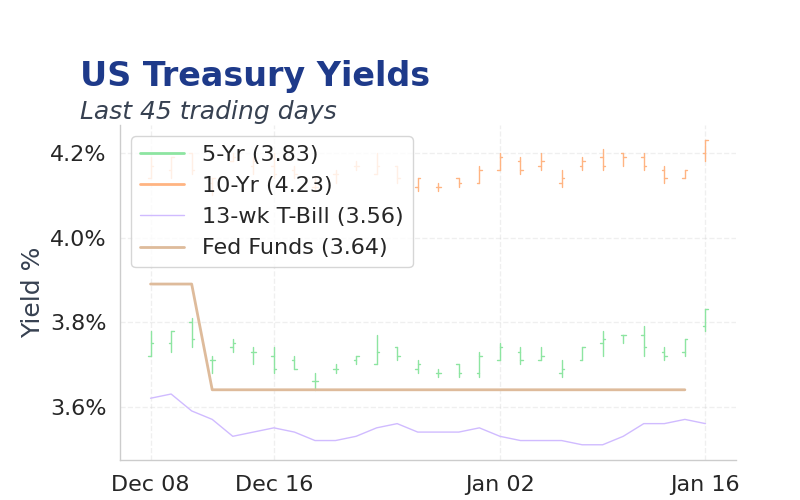

| 2 Year Bond Yield | 3.60 | -0 bps |

| 10 Year Bond Yield | 4.29 | +7 bps |

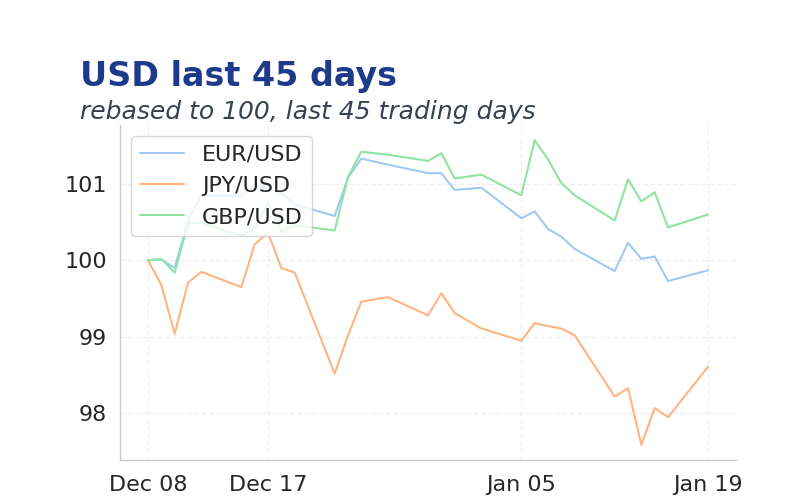

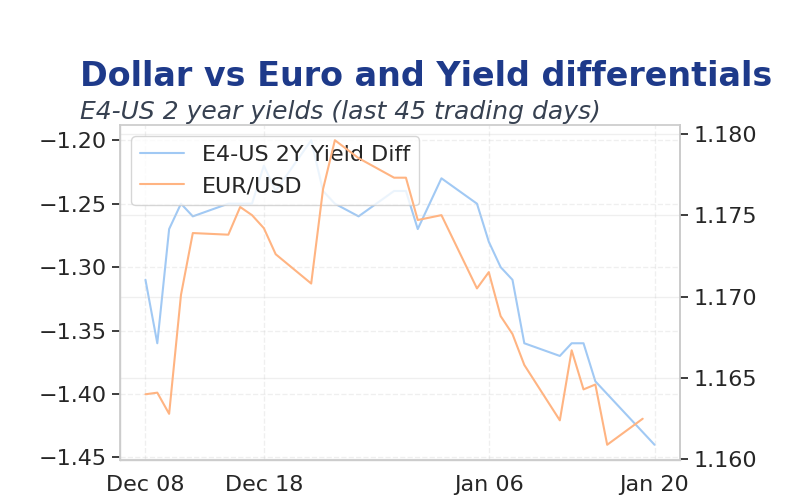

| EUR/USD | 1.1666 | +0.17% |

| USD/JPY | 158.24 | +0.07% |

| GBP/USD | 1.344 | +0.10% |

| WTI Oil | 59.19 | 0.00% |

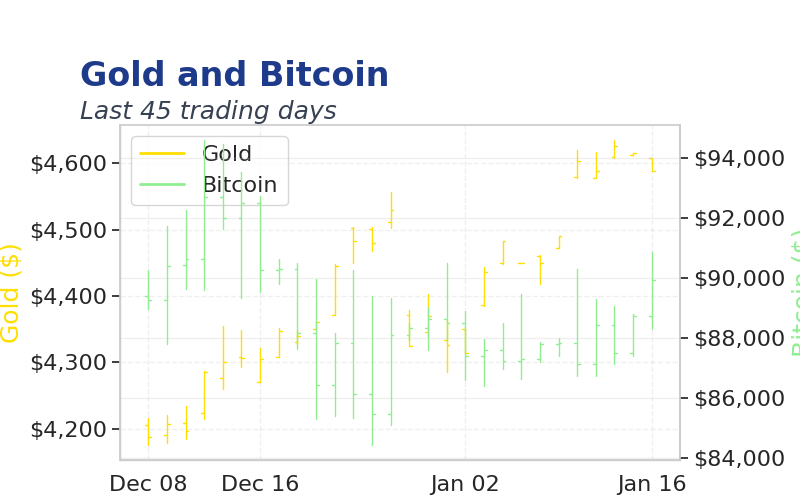

| Gold | 4,727.68 | +1.07% |

| Bitcoin | 90,995.28 | -1.69% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ADP Employment Change Weekly | 11,750 | - | 08:15 |

| API Weekly Crude Oil Stocks | 5.3m | - | 16:30 |

| MBA 30-Year Mortgage Rate | 6.18 | - | 07:00 |

| Pending Home Sales Month-over-Month | 3.30 | -2.60 | 10:00 |

| Pending Home Sales Year-over-Year | 2.60 | - | 10:00 |

- Trump's proposed tariffs on European nations over Greenland sparked global market declines and boosted safe-haven assets like gold.

- US labor market data showed mixed resilience, with ADP employment beating expectations but broader economic concerns lingering.

- Geopolitical shifts in Syria and rising inequality highlighted evolving global risks for investors.

Yesterday's Recap

ADP employment change rose to 11,750, surpassing consensus and signaling persistent labor market strength despite ongoing rate cuts.

API weekly crude oil stocks showed a draw of 5.27 million barrels, aligning with expectations and stabilizing oil prices around $59 per barrel.

Markets traded calmly, with the S&P 500 dipping 0.1% to 6946.60 and Nasdaq down 0.1% to 23515.39, while VIX edged up to 20.17 reflecting mild volatility.

Bond yields rose modestly, with the 2-year up to 3.60% and 10-year to 4.29%, amid Fed chair uncertainty.

The USD firmed against the euro at 1.1666 and yen at 158.24, while gold climbed to 4727.68 and Bitcoin held at 90995.28.

No major Fed speeches yesterday, but prior comments reinforced data-dependent easing. (cont...)