US Macro Daily(Beta Mode)

Tariffs Boost Safe-Haven Assets

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,883.20 | +1.13% |

| Nasdaq | 23,224.82 | +1.18% |

| Spot VIX | 16.04 | -5.09% |

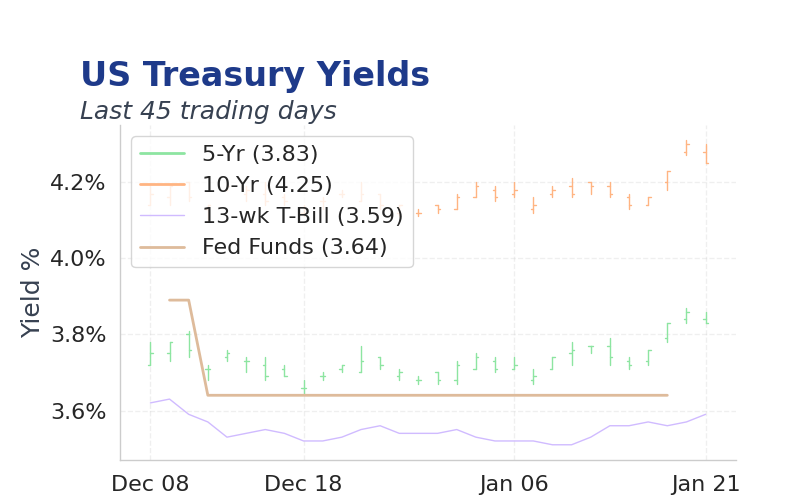

| 2 Year Bond Yield | 3.60 | 0 bps |

| 10 Year Bond Yield | 4.25 | +1 bps |

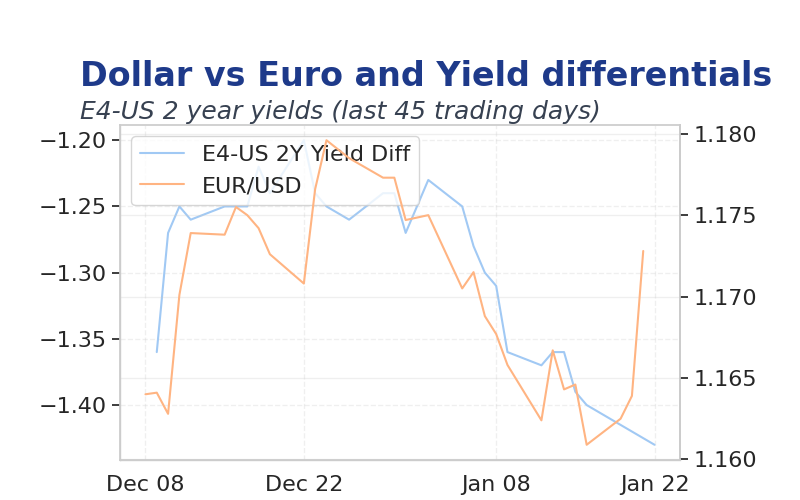

| EUR/USD | 1.1697 | +0.09% |

| USD/JPY | 158.66 | +0.18% |

| GBP/USD | 1.342 | -0.04% |

| WTI Oil | 60.34 | 0.00% |

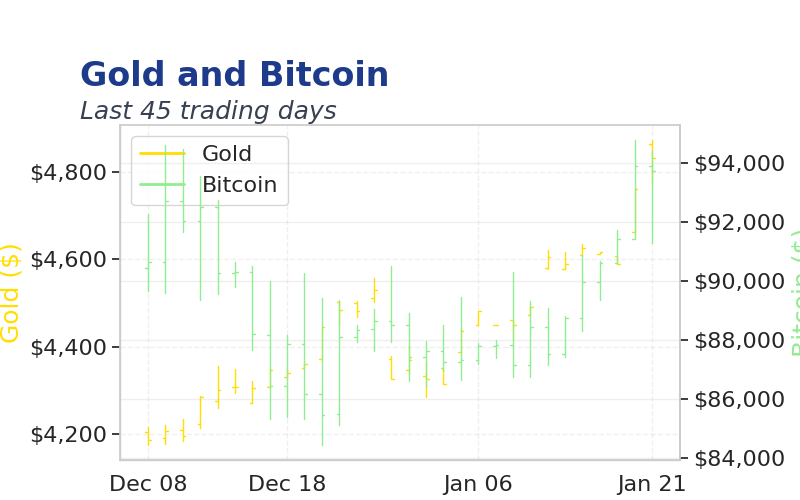

| Gold | 4,828.13 | -0.05% |

| Bitcoin | 89,866.61 | +0.56% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| MBA 30-Year Mortgage Rate | 6.18 | - | 6.16 |

| Us President Trump Speech | - | - | - |

| Pending Home Sales Month-over-Month | 3.30 | -0.30 | -9.30 |

| Pending Home Sales Year-over-Year | 2.60 | - | -3 |

| API Weekly Crude Oil Stocks | 5.3m | - | 3.0m |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter Final Estimate | 3.80 | 4.30 | 08:30 |

| GDP Price Index Quarter-over-Quarter Final | 2.10 | - | 08:30 |

| Weekly Jobless Claims | 198,000 | 212,000 | 08:30 |

| Core PCE Price Index Month-over-Month | 0.20 | - | 10:00 |

| Core PCE Price Index Month-over-Month | - | 0.20 | 10:00 |

| Personal Income Month-over-Month | 0.40 | - | 10:00 |

| Personal Income Month-over-Month | - | 0.40 | 10:00 |

| Personal Spending Month-over-Month | 0.30 | - | 10:00 |

| Personal Spending Month-over-Month | - | 0.50 | 10:00 |

| PCE Price Index Month-over-Month | 0.30 | - | 10:00 |

- Pending home sales plunged 9.3% month-over-month, signaling housing market weakness amid tariff-induced economic pressures.

- Today's GDP final estimate at 4.3% and core PCE inflation data will test growth and price stability narratives.

- Geopolitical tensions over Greenland drove gold prices higher, highlighting investor flight to safe assets.

Yesterday's Recap

Pending home sales dropped 9.3% month-over-month and 3.0% year-over-year, missing expectations and reflecting cooling demand in the housing sector.

API crude oil inventories rose by 3.04 million barrels, surpassing forecasts and exerting downward pressure on oil prices.

Markets remained calm, with VIX at 16.04 indicating low volatility, as investors digested mixed economic signals.

Bond yields edged lower, with the 2-year at 3.60% and 10-year at 4.25%, amid easing inflation concerns.

Gold surged to 4828.13 amid Greenland disputes, while bitcoin traded at 89866.61.

No major Fed speeches occurred, but prior comments underscored data-dependent policy.

The Day Ahead

The GDP growth final estimate at 08:30 is expected at 4.3%, potentially confirming robust economic expansion.

Core PCE inflation at 10:00, forecasted at 0.2% month-over-month, will gauge price pressures influencing Fed decisions.

Weekly jobless claims at 08:30, consensus at 212,000, may reveal labor market trends.