US Macro Daily(Beta Mode)

GDP Surge Fuels Optimism

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,919.60 | +0.53% |

| Nasdaq | 23,436.02 | +0.91% |

| Spot VIX | 15.82 | +1.15% |

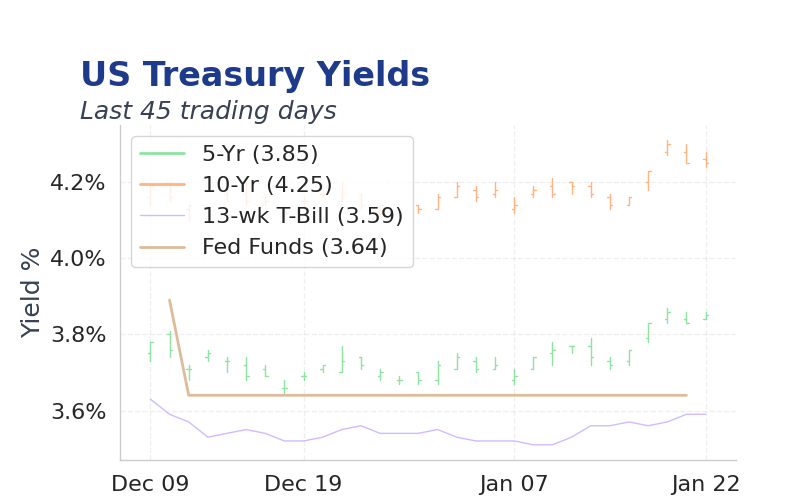

| 2 Year Bond Yield | 3.62 | 0 bps |

| 10 Year Bond Yield | 4.24 | -0 bps |

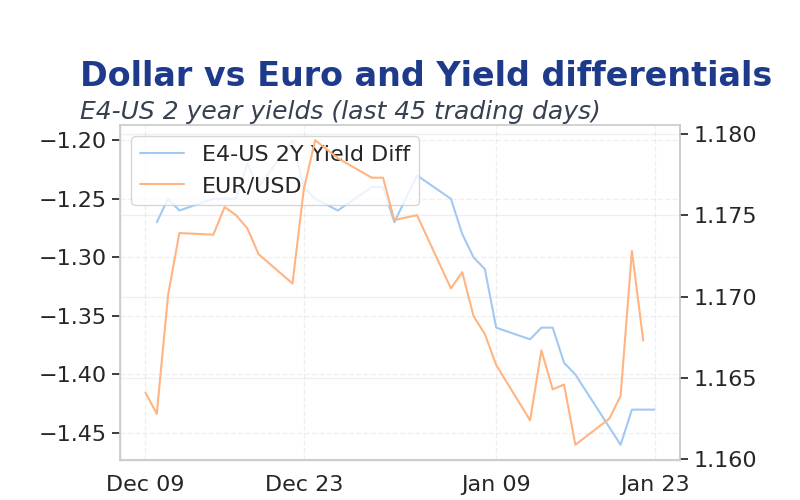

| EUR/USD | 1.1737 | -0.10% |

| USD/JPY | 158.29 | -0.09% |

| GBP/USD | 1.353 | +0.21% |

| WTI Oil | 60.62 | +0.46% |

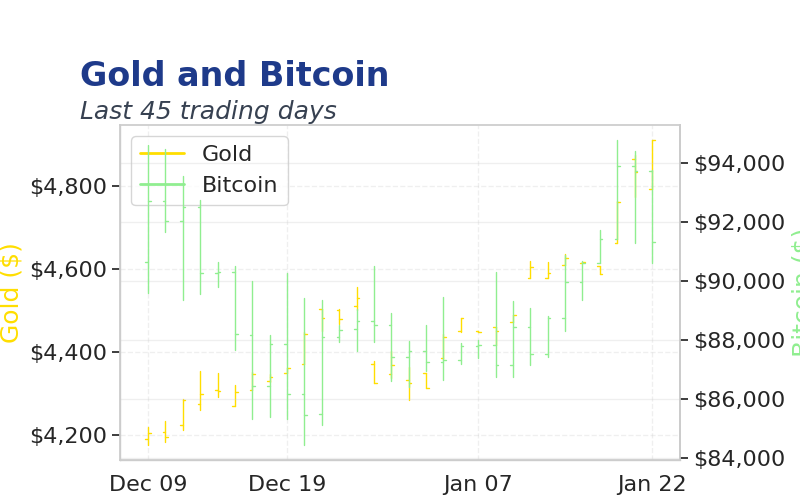

| Gold | 4,921.07 | -0.29% |

| Bitcoin | 89,118.31 | -0.38% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter Final Estimate | 3.80 | 4.30 | 4.40 |

| GDP Price Index Quarter-over-Quarter Final | 2.10 | - | 3.70 |

| Weekly Jobless Claims | 199,000 | 212,000 | 200,000 |

| Core PCE Price Index Month-over-Month | 0.20 | 0.20 | 0.20 |

| Core PCE Price Index Month-over-Month | 0.20 | - | 0.20 |

| Personal Income Month-over-Month | 0.40 | - | 0.10 |

| Personal Income Month-over-Month | 0.10 | 0.40 | 0.30 |

| Personal Spending Month-over-Month | 0.50 | 0.50 | 0.50 |

| Personal Spending Month-over-Month | 0.40 | - | 0.50 |

| PCE Price Index Month-over-Month | 0.20 | 0.20 | 0.20 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Composite PMI Flash | 52.70 | - | 09:45 |

| S&P Global Manufacturing PMI Flash | 51.80 | 52 | 09:45 |

| S&P Global Services PMI Flash | 52.50 | 52.80 | 09:45 |

| Michigan Consumer Sentiment Final | 52.90 | 54 | 10:00 |

- US GDP growth accelerated to 4.4% in Q3, surpassing expectations and signaling robust economic momentum.

- Weekly jobless claims dipped to 200,000, beating forecasts and highlighting labor market resilience.

- Gold neared $5,000 amid geopolitical tensions, while crude oil inventories built despite price stability.

Yesterday's Recap

US GDP growth revised up to 4.4% quarter-over-quarter, exceeding the 4.3% consensus and driven by strong consumer spending.

Weekly jobless claims fell to 200,000 from 212,000 expected, indicating ongoing labor market strength.

Core PCE inflation held steady at 0.2% month-over-month, in line with forecasts, while personal income and spending showed mixed results with income missing expectations.

Markets traded calmly with VIX at 15.82, S&P 500 at 6919.60, and Nasdaq at 23436.02, as bond yields ticked up modestly to 3.62% for 2-year and 4.24% for 10-year.

Gold climbed to 4921.07, Bitcoin held at 89118.31, and WTI oil eased to 60.62 amid inventory builds.

The Day Ahead

S&P Global Composite PMI at 09:45 is expected at 52.7, providing early signals on manufacturing and services activity.

S&P Global Manufacturing PMI at 09:45, forecasted at 52.0, will gauge industrial momentum.

Michigan Consumer Sentiment at 10:00, expected at 54.0, may reflect consumer confidence trends.