US Macro Daily(Beta Mode)

Retail Slump Fuels Cut Hopes

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,951.50 | -0.28% |

| Nasdaq | 23,102.47 | -0.59% |

| Spot VIX | 18.11 | +1.80% |

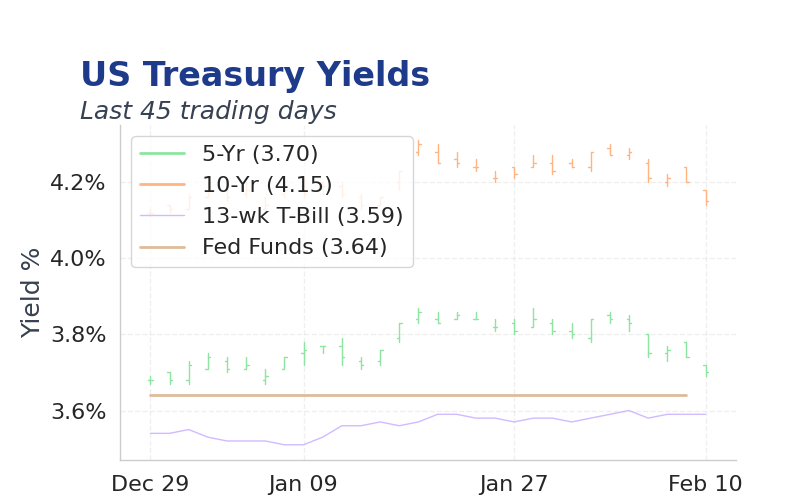

| 2 Year Bond Yield | 3.46 | -1 bps |

| 10 Year Bond Yield | 4.14 | -1 bps |

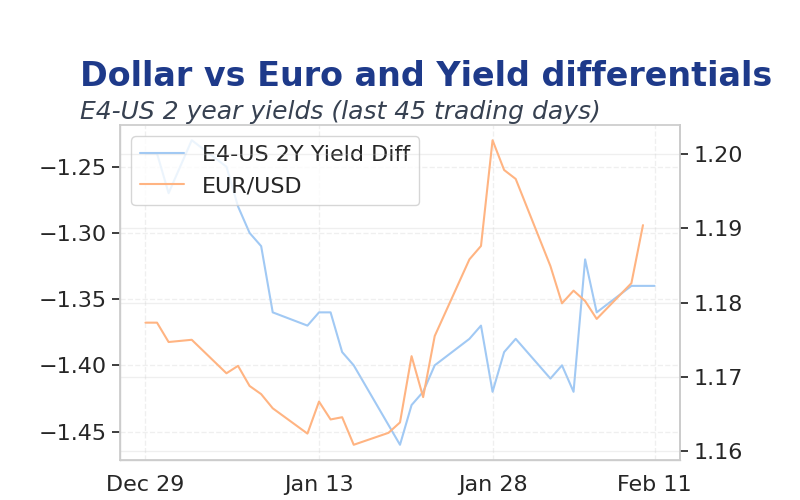

| EUR/USD | 1.1912 | +0.14% |

| USD/JPY | 153.35 | -0.64% |

| GBP/USD | 1.369 | +0.31% |

| WTI Oil | 64.36 | +1.27% |

| Gold | 5,101.24 | +1.54% |

| Bitcoin | 66,834.49 | -2.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ADP Employment Change Weekly | 5,000 | - | 6,500 |

| Retail Sales Month-over-Month | 0.60 | 0.40 | 0 |

| Employment Cost - Benefits Quarter-over-Quarter | 0.80 | - | 0.70 |

| Employment Cost - Wages Quarter-over-Quarter | 0.80 | - | 0.70 |

| Employment Cost Index Quarter-over-Quarter | 0.80 | 0.80 | 0.70 |

| Export Prices Month-over-Month | - | 0.10 | 0.30 |

| Import Prices Month-over-Month | - | 0.10 | 0.10 |

| Retail Sales Control Group Month-over-Month | 0.20 | 0.40 | -0.10 |

| Retail Sales Excluding Autos Month-over-Month | 0.40 | 0.30 | 0 |

| Ny Fed Bill Purchases 1 To 4 Months | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| MBA 30-Year Mortgage Rate | 6.21 | - | 07:00 |

| Payroll Jobs Growth | 50,000 | 70,000 | 08:30 |

| Headline Unemployment Rate | 4.40 | 4.40 | 08:30 |

| Monthly Wage Growth | 0.30 | 0.30 | 08:30 |

| Annual Wage Growth | 3.80 | 3.60 | 08:30 |

| Labor Force Participation | 62.40 | - | 08:30 |

| Speech by Fed's Bowman | - | - | 10:15 |

| EIA Weekly Crude Oil Inventory | -3.5m | -200,000 | 10:30 |

| EIA Weekly Gasoline Inventory | 685,000 | - | 10:30 |

| Monthly Budget Statement | -145m | -86.5m | 14:00 |

- Retail sales flat, missing expectations, signaling cooling consumer demand amid job market strains.

- ADP payrolls beat consensus, but revisions may slash prior gains, clouding labor outlook.

- Oil inventories rise, pressuring prices as geopolitical tensions linger.

Yesterday's Recap

ADP employment change surged to 6,500, exceeding the prior 5,000 but below consensus, reflecting uneven labor recovery.

Retail sales remained flat, disappointing against a 0.4% expected gain and prior 0.6%, with control group contracting 0.1%, indicating consumer caution.

Employment cost index edged down to 0.7%, matching consensus, while export prices rose 0.3% versus 0.1% expected.

Markets calmed, VIX at 18.11, as S&P 500 held at 6,951.50; bond yields dipped modestly with 10-year at 4.14%, and WTI oil fell to 64.36 on inventory builds.

The Day Ahead

Investors eye nonfarm payrolls at 70,000 consensus, up from 50,000 prior, for labor market clarity.

Unemployment rate expected steady at 4.4%, with wage growth data probing inflation pressures.

Fed's Bowman speech at 10:15 may address easing pace, while EIA crude inventory and budget statement could sway commodities.