US Macro Daily(Beta Mode)

February 17, 2026

robomacro.com

CPI Softens, Cuts Advance

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,847.60 | +0.06% |

| Nasdaq | 22,546.67 | -0.22% |

| Spot VIX | 22.10 | +7.28% |

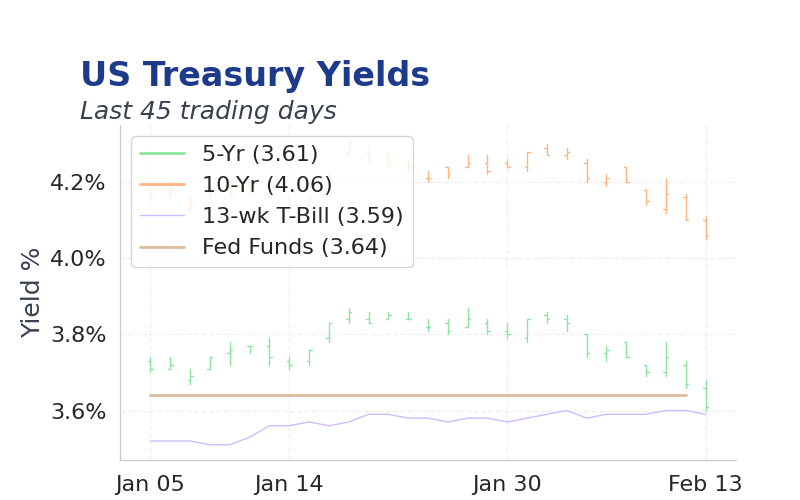

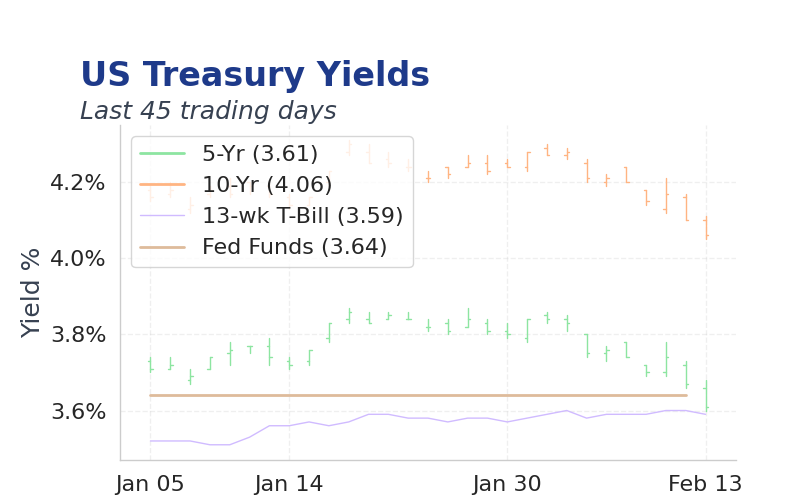

| 2 Year Bond Yield | 3.41 | -1 bps |

| 10 Year Bond Yield | 4.03 | -2 bps |

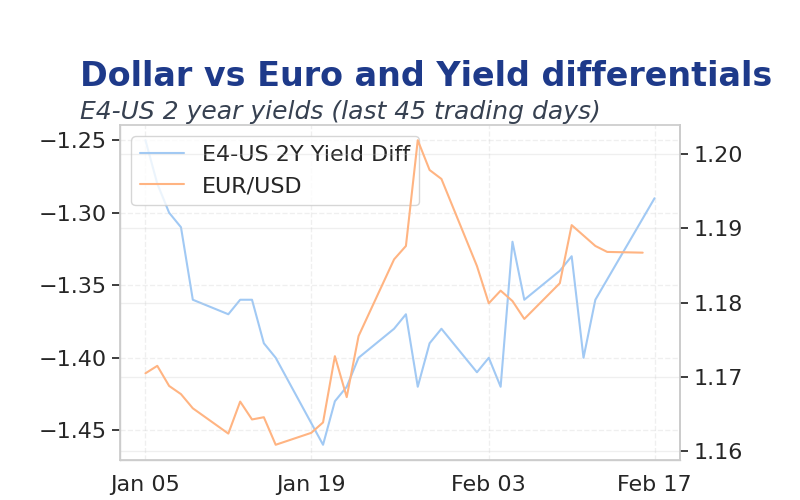

| EUR/USD | 1.1843 | -0.09% |

| USD/JPY | 152.98 | -0.34% |

| GBP/USD | 1.359 | -0.32% |

| WTI Oil | 63.80 | +0.03% |

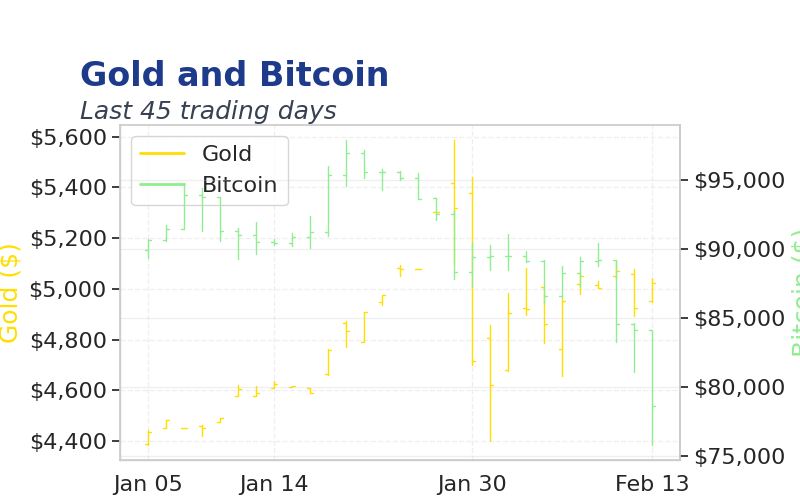

| Gold | 4,928.52 | -1.25% |

| Bitcoin | 67,795.42 | -1.55% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Speech by Fed's Bowman | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ADP Employment Change Weekly | 6,500 | - | 08:15 |

| NY Empire State Manufacturing Index | 7.70 | 6 | 08:30 |

| NAHB Housing Market Index | 37 | 38 | 10:00 |

| Speech by Fed's Barr | - | - | 12:45 |

| Fed Daly Speech | - | - | 14:30 |

| MBA 30-Year Mortgage Rate | 6.21 | - | 07:00 |

| Building Permits Prel | 1.4m | - | 08:30 |

| Building Permits Prel | - | 1.4m | 08:30 |

| Durable Goods Orders Month-over-Month | 5.30 | -2 | 08:30 |

| Housing Starts Level | 1.2m | - | 08:30 |

- January CPI rose 0.2% m/m and 2.4% y/y, below consensus, easing inflation fears and supporting Fed rate cuts.

- US-Iran nuclear talks resumed, with Trump signaling optimism but warning of escalation if no deal emerges.

- Markets calmed post-holiday, with S&P 500 futures flat and VIX at 22.10, as investors digest data.

Yesterday's Recap

January CPI climbed 0.2% month-over-month and 2.4% year-over-year, missing consensus forecasts of 0.3% and 2.5%, with core measures cooling to 0.3% m/m and 2.5% y/y.

Equities closed mixed, S&P 500 up 0.05% to 6836.17 and Nasdaq down 0.22% to 22546.67, while utilities and real estate led gains.

Bond yields edged lower, 2-year Treasury down 6bps to 3.41% and 10-year down 7bps to 4.03%, reflecting dovish inflation signals.

FX remained steady, EUR/USD at 1.1843 and GBP/USD at 1.359, with USD/JPY up slightly to 152.98.

Commodities saw gold rise 1.29% to 4926.51 and oil climb 0.62% to 63.14, amid geopolitical tensions; Bitcoin fell 1.26% to 67795.42.

Fed Governor Bowman spoke on labor markets, but no major policy shifts emerged. (cont...)

Page 1