US Macro Daily(Beta Mode)

Fed Eyes Cuts Amid Mixed Data

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,876.80 | -0.24% |

| Nasdaq | 22,682.73 | -0.31% |

| Spot VIX | 20.57 | +1.68% |

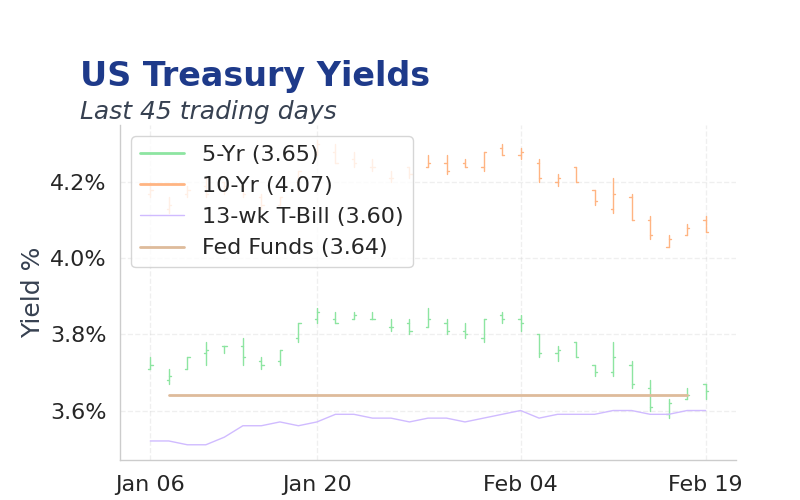

| 2 Year Bond Yield | 3.48 | +2 bps |

| 10 Year Bond Yield | 4.08 | -0 bps |

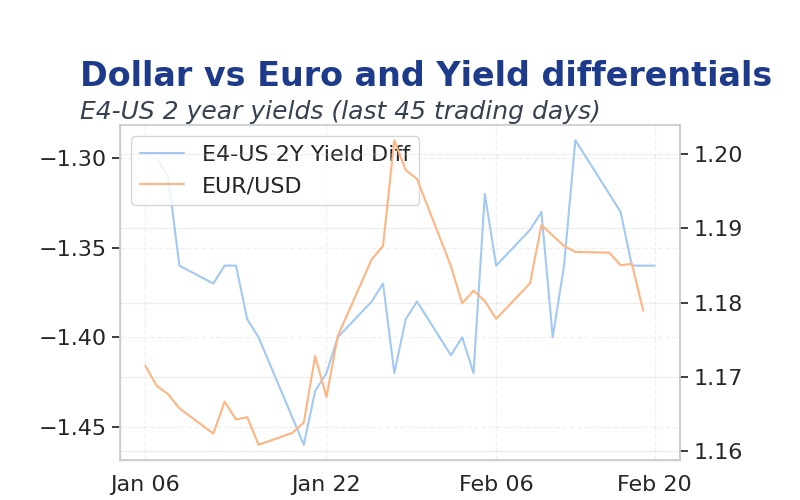

| EUR/USD | 1.1767 | -0.02% |

| USD/JPY | 155.31 | +0.15% |

| GBP/USD | 1.348 | +0.13% |

| WTI Oil | 66.09 | -0.46% |

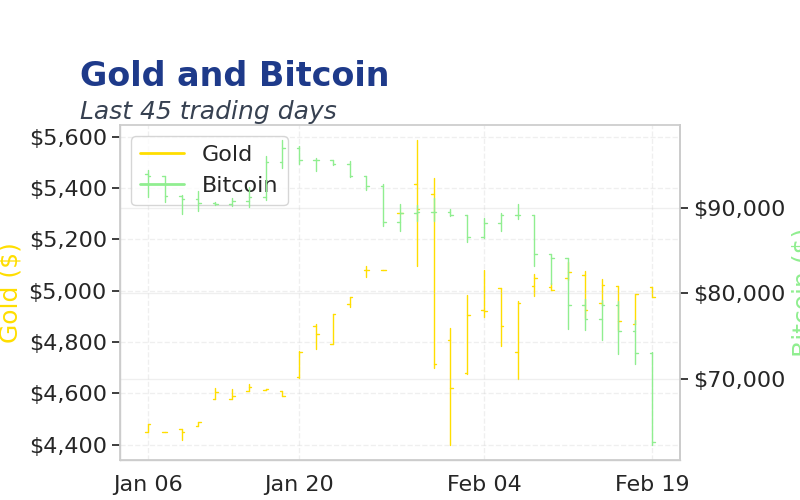

| Gold | 5,027.18 | +0.59% |

| Bitcoin | 68,162.55 | +1.78% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Speech by Fed's Bostic | - | - | - |

| Trade Balance | -53m | -55.5m | -70.3m |

| Exports Level | 292.3m | - | 287.3m |

| Speech by Fed's Bowman | - | - | - |

| Goods Trade Balance Adv | -82.8m | -86m | -98.5m |

| Imports Level | 345.3m | - | 357.6m |

| Weekly Jobless Claims | 229,000 | 225,000 | 206,000 |

| Philadelphia Fed Manufacturing Index | 12.60 | 8.50 | 16.30 |

| Retail Inventories Ex Autos Month-over-Month Adv | -0.20 | - | 0.20 |

| Wholesale Inventories Month-over-Month Adv | 0.20 | 0.20 | 0.20 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Core PCE Price Index Month-over-Month | 0.20 | 0.30 | 08:30 |

| GDP Growth Quarter-over-Quarter Advance Estimate | 4.40 | 3 | 08:30 |

| Personal Income Month-over-Month | 0.30 | 0.30 | 08:30 |

| Personal Spending Month-over-Month | 0.50 | 0.40 | 08:30 |

| GDP Price Index Quarter-over-Quarter Adv | 3.70 | - | 08:30 |

| PCE Price Index Month-over-Month | 0.20 | 0.30 | 08:30 |

| PCE Price Index Year-over-Year | 2.80 | 2.80 | 08:30 |

| Speech by Fed's Bostic | - | - | 09:45 |

| S&P Global Composite PMI Flash | 53 | - | 09:45 |

| S&P Global Manufacturing PMI Flash | 52.40 | 52.60 | 09:45 |

- US trade deficit widened unexpectedly, signaling persistent import pressures and potential inflationary risks.

- Weekly jobless claims fell below consensus, hinting at labor market resilience despite broader economic slowdowns.

- Markets remained stable with equities holding gains, but bond yields edged higher on hawkish data surprises.

Yesterday's Recap

The US trade balance deteriorated sharply to a deficit of $70.3 billion, worse than expected $55.5 billion, driven by weaker exports and higher imports.

Weekly jobless claims improved to 206,000, beating consensus of 225,000, while the Philadelphia Fed Manufacturing Index surged to 16.3 from 8.5, indicating robust factory activity.

Retail inventories rose 0.2%, aligning with consensus, amid mixed signals from Fed speeches on Bostic and Bowman that emphasized data dependence.

The Day Ahead

Core PCE is expected at 0.3% m/m, up from previous 0.2%, potentially signaling persistent inflationary pressures for Fed watchers.

GDP growth advance estimate forecasts 3% quarterly, contrasting with prior 4.4%, while personal spending consensus holds at 0.4% m/m.

Fed's Bostic speech at 9:45am and S&P Global PMI flashes may offer fresh policy clues ahead of key inflation data.