US Macro Daily(Beta Mode)

Equities Rally, Yields Ease

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,890.07 | +0.77% |

| Nasdaq 100 | 24,977.04 | +1.09% |

| Dow Jones | 49,174.50 | +0.76% |

| Russell 2000 | 2,652.33 | +1.20% |

| USD/JPY | 156.79 | +1.40% |

| EUR/USD | 1.18 | -0.16% |

| GBP/USD | 1.35 | -0.03% |

| Gold | 5,180.00 | +0.47% |

| WTI Crude | 65.86 | +0.35% |

| Bitcoin | 65,362.78 | +2.00% |

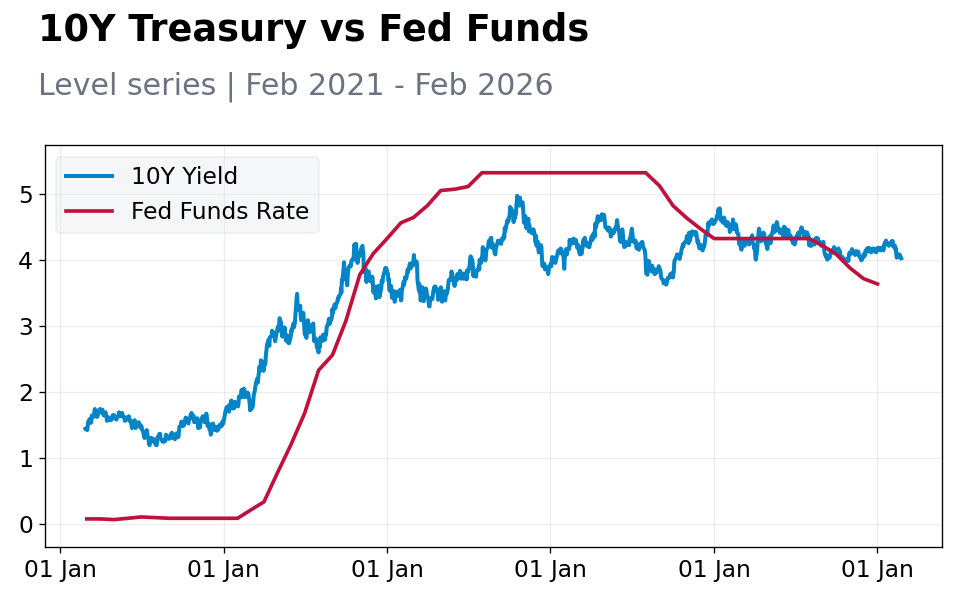

| US 2Y Treasury | 3.43% | -1.44% |

| US 10Y Treasury | 4.03% | -1.23% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Speech by Fed's Waller | - | - | - |

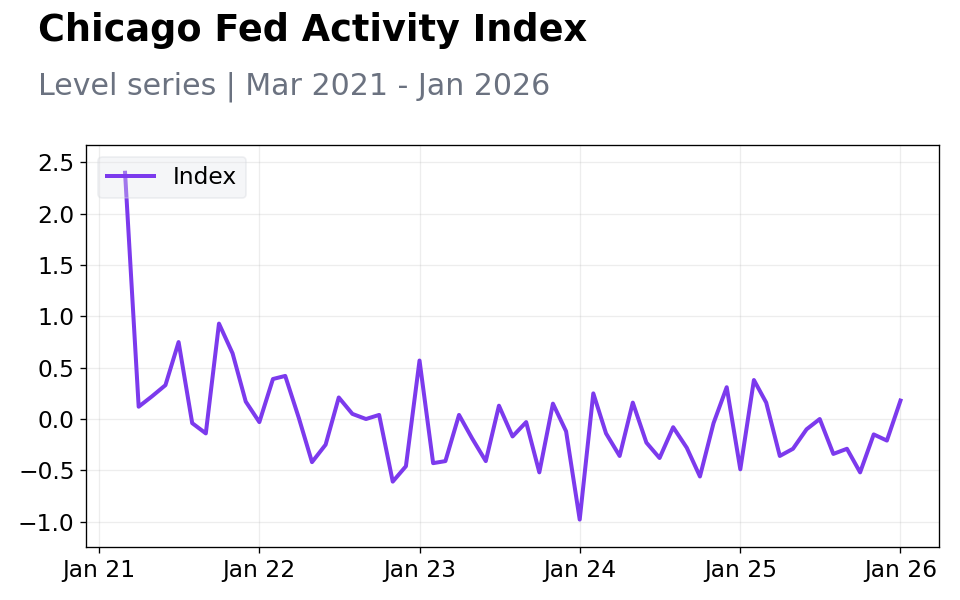

| Chicago Fed National Activity Index | -0.21 | - | 0.18 |

| Chicago Fed National Activity Index | -0.15 | - | -0.21 |

| Factory Orders Month-over-Month | 2.70 | -0.50 | -0.70 |

| Dallas Fed Manufacturing Index | -1.20 | - | 0.20 |

| Fed Golsbee Speech | - | - | - |

| ADP Employment Change Weekly | 11,500 | - | 12,750 |

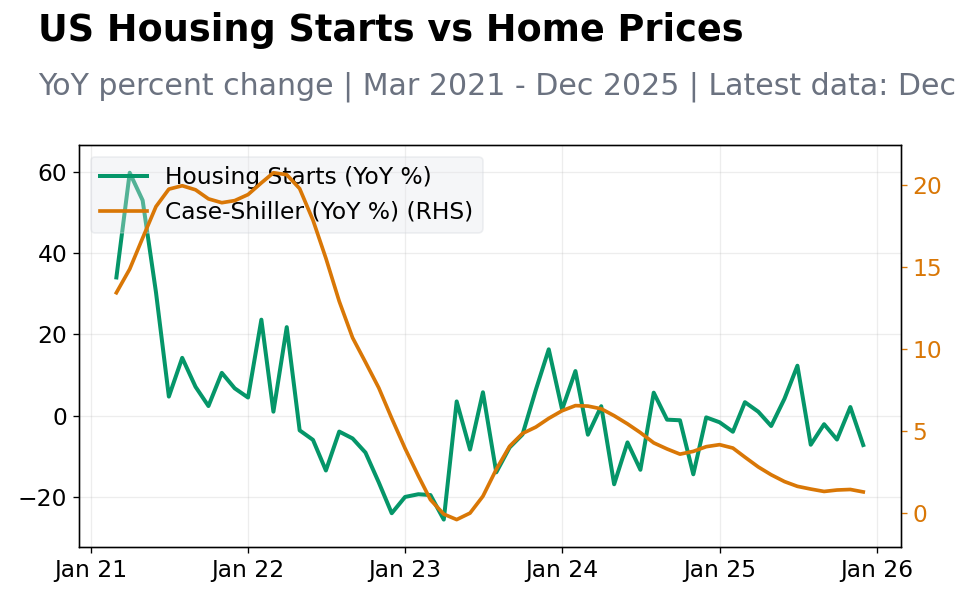

| S&P/Case-Shiller Home Price Year-over-Year | 1.40 | 1.40 | 1.40 |

| Speech by Fed's Bostic | - | - | - |

| Speech by Fed's Collins | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| MBA 30-Year Mortgage Rate | 6.17 | - | 02:00 |

| Speech by Fed's Barkin | - | - | 04:35 |

| EIA Weekly Crude Oil Inventory | -9.0m | 1.8m | 05:30 |

| EIA Weekly Gasoline Inventory | -3.2m | - | 05:30 |

| Speech by Fed's Musalem | - | - | 08:20 |

- US stocks climbed on upbeat consumer data and Fed remarks, with S&P 500 up 0.77% amid tech-led gains.

- Treasury yields declined as factory orders undershot, fueling rate-cut bets despite mixed activity signals.

- Multiple Fed speeches underscored data-driven caution, supporting sentiment in housing and jobs.

Yesterday's Recap

US markets ended higher on February 24, with the S&P 500 advancing 0.77% to 6,890.07, propelled by tech and consumer strength after solid confidence figures. The Nasdaq 100 gained 1.09% to 24,977.04 on AI enthusiasm, the Dow Jones rose 0.76% to 49,174.50, and Russell 2000 jumped 1.20% to 2,652.33, showing widespread optimism. Treasury yields slipped, with the 2-year down 1.44% to 3.43% and 10-year off 1.23% to 4.03%, as weak factory data spurred easing expectations.

Chicago Fed National Activity Index showed mixed revisions: one reading improved to 0.18 from -0.21, while another adjusted to -0.21 from -0.15, suggesting patchy economic momentum. Factory orders dropped 0.7% MoM against consensus -0.5% and previous 2.7%, weighing on industrials. Dallas Fed Manufacturing Index exceeded forecasts at 0.2 from -1.2, indicating regional upturn.

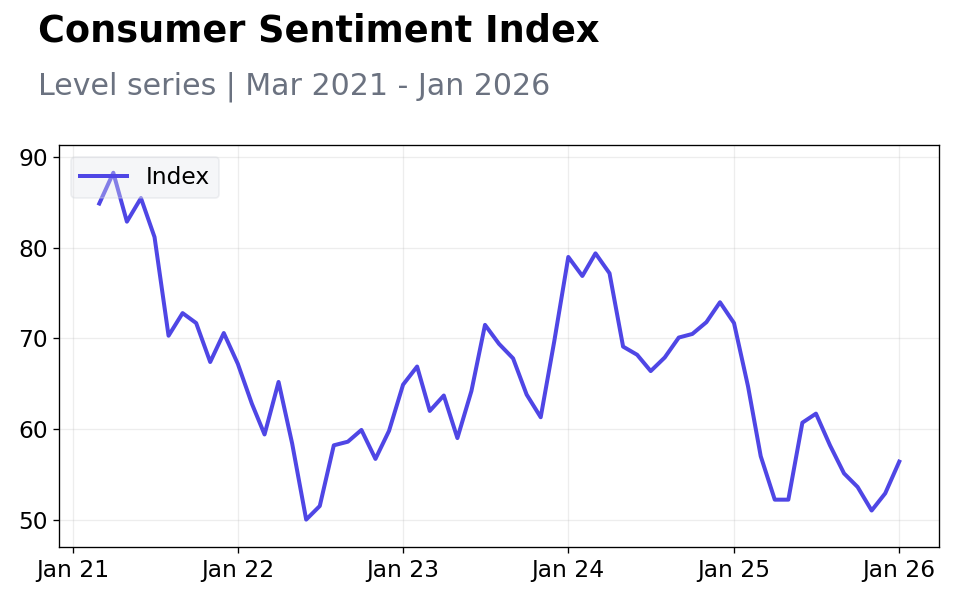

S&P/Case-Shiller home prices met expectations at 1.4% YoY, unchanged from prior. CB Consumer Confidence improved to 91.2 from 89.0, lifting mood, while ADP weekly employment rose to 12,750 from 11,500, hinting at gradual hiring. Currencies shifted with USD/JPY up 1.40% to 156.79 on yield spreads, EUR/USD down 0.16% to 1.18, and GBP/USD near flat at 1.35 with a -0.03% dip.

The Day Ahead

Focus shifts to the MBA 30-Year Mortgage Rate at 02:00 ET on February 25, potentially affecting housing views given stable prices. Fed's Barkin speaks at 04:35 ET, offering insights on policy amid recent data. With a light calendar, markets may react to any unscheduled news or global cues, while eyeing durable goods later in the week.

Volatility could rise from month-end positioning, especially in bonds and stocks, as traders assess geopolitical risks.

Other Economic Notes

Warnings emerge of market-economy decoupling, with speculation inflating assets despite weak fundamentals, per economist Mark Zandi, raising sell-off risks. The 2025 economy expanded 2.2% amid near-zero net job growth, deepening inequality in a K-shaped setup where high earners thrive while others lag. Resilient spending props up growth, but manufacturing dips and housing steadiness reveal imbalances, urging caution on overvalued markets.