Yesterday's Recap

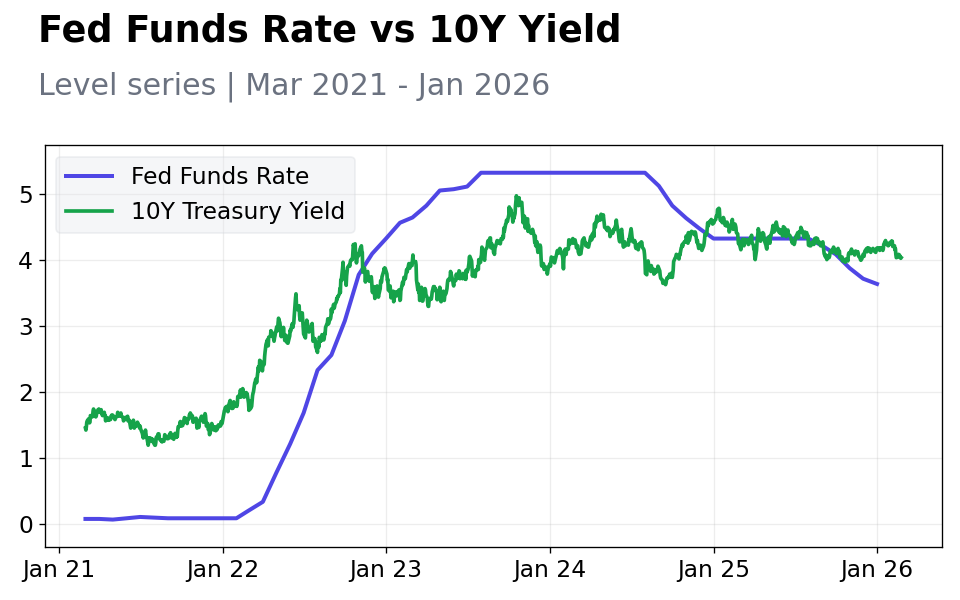

US markets closed higher on February 25, with the S&P 500 rising 0.81% to 6,946.13, driven by gains in technology and consumer sectors despite softer manufacturing data. The Nasdaq 100 surged 1.41% to 25,329.04, buoyed by AI-related enthusiasm, while the Dow Jones added 0.63% to 49,482.15 and the Russell 2000 gained 0.41% to 2,663.33. Treasury yields ticked up modestly, with the 10-year note climbing 0.25% to 4.04%, reflecting ongoing inflation concerns from recent Fed commentary.

Factory orders fell 0.7% month-over-month, missing the consensus of -0.5%, pressured by transportation weakness, though the Chicago Fed National Activity Index improved to 0.18 from -0.21. Consumer confidence edged up to 91.2 from 89.0, supported by stable labor market views, while the Dallas Fed Manufacturing Index rose to 0.2 from -1.2, indicating modest regional recovery. ADP employment change showed a slight uptick to 12,750 from 11,500, but currency markets remained subdued with USD/JPY up 0.09% to 156.02 and EUR/USD gaining 0.25% to 1.18.

Overall, equities shrugged off commodity declines, with WTI crude dropping 1.59% to 64.38 and gold slipping 0.30% to 5,191.00, as investors focused on Fed speeches hinting at cautious easing.

The Day Ahead

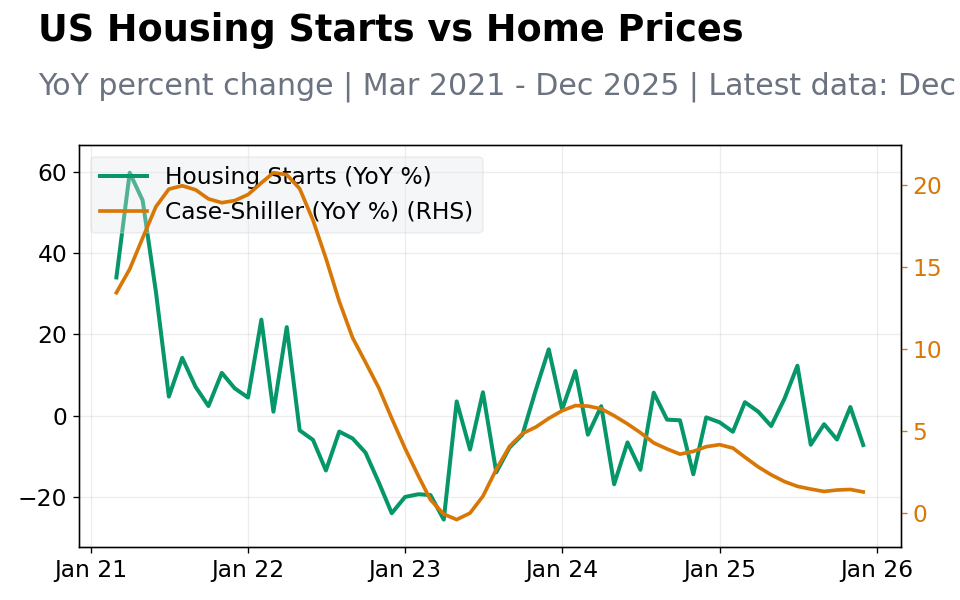

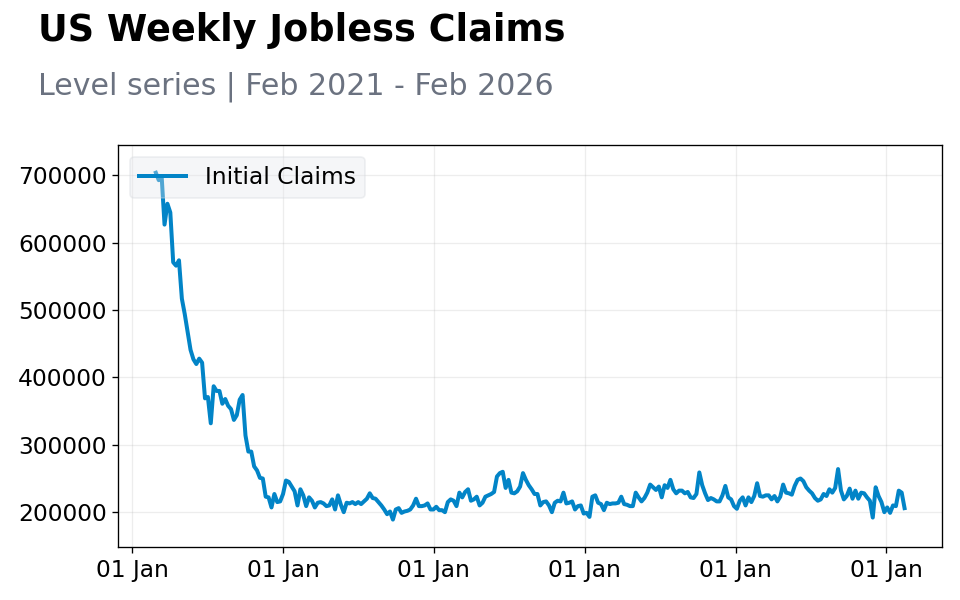

Weekly jobless claims data, due at 8:30 ET on February 26, will provide fresh insights into labor market health, with consensus expecting 215,000 initial claims amid ongoing hiring stagnation. The advance goods trade balance and wholesale inventories releases at 8:30 ET could influence GDP revisions, potentially highlighting export weakness from tariff uncertainties. Pending home sales for January, out at 10:00 ET, may reflect housing sector pressures from elevated mortgage rates, with forecasts pointing to a 1.0% monthly increase.

A speech by Fed's Bowman is scheduled, which could offer further policy clues, allowing markets to digest prior commentary, though any surprises in data could shift Treasury yield trajectories. Attention will also turn to corporate earnings from key retailers, which might underscore consumer spending trends.