US Macro Daily(Beta Mode)

Stocks Mixed Amid Soft Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,908.86 | -0.54% |

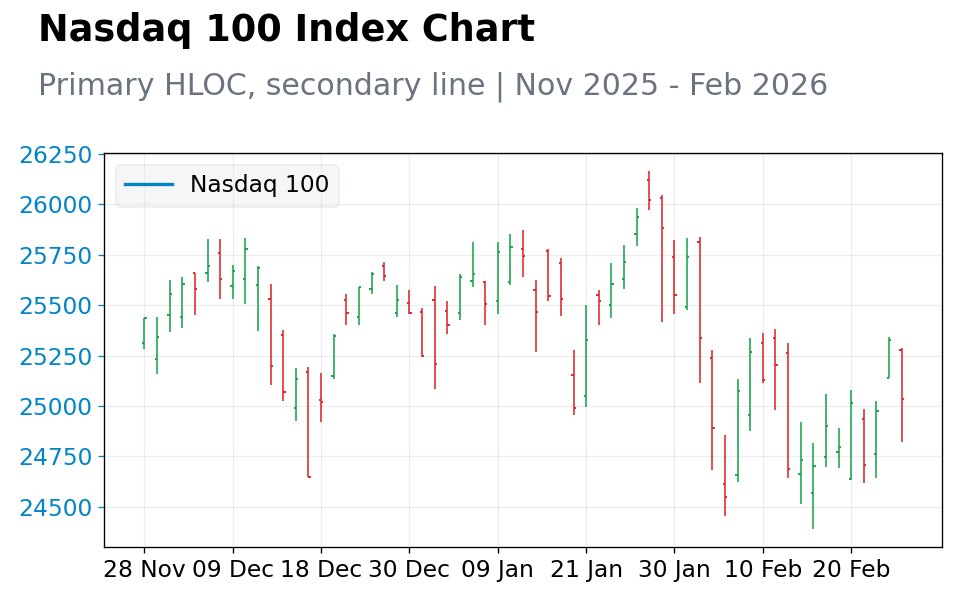

| Nasdaq 100 | 25,034.37 | -1.16% |

| Dow Jones | 49,499.20 | +0.03% |

| Russell 2000 | 2,677.29 | +0.52% |

| USD/JPY | 155.85 | -0.23% |

| EUR/USD | 1.18 | -0.05% |

| GBP/USD | 1.35 | -0.62% |

| Gold | 5,203.90 | +0.53% |

| WTI Crude | 66.80 | +2.44% |

| Bitcoin | 66,066.92 | -2.06% |

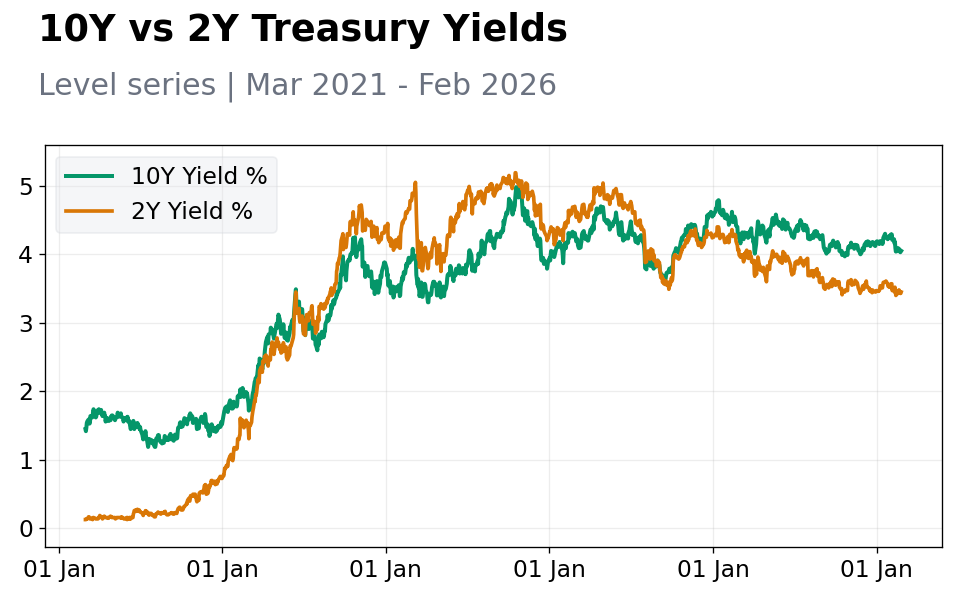

| US 2Y Treasury | 3.45% | +0.58% |

| US 10Y Treasury | 4.05% | +0.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Speech by Fed's Waller | - | - | - |

| Chicago Fed National Activity Index | -0.21 | - | 0.18 |

| Chicago Fed National Activity Index | -0.15 | - | -0.21 |

| Factory Orders Month-over-Month | 2.70 | -0.50 | -0.70 |

| Dallas Fed Manufacturing Index | -1.20 | - | 0.20 |

| Fed Golsbee Speech | - | - | - |

| ADP Employment Change Weekly | 11,500 | - | 12,750 |

| S&P/Case-Shiller Home Price Year-over-Year | 1.40 | 1.40 | 1.40 |

| Speech by Fed's Bostic | - | - | - |

| Speech by Fed's Collins | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

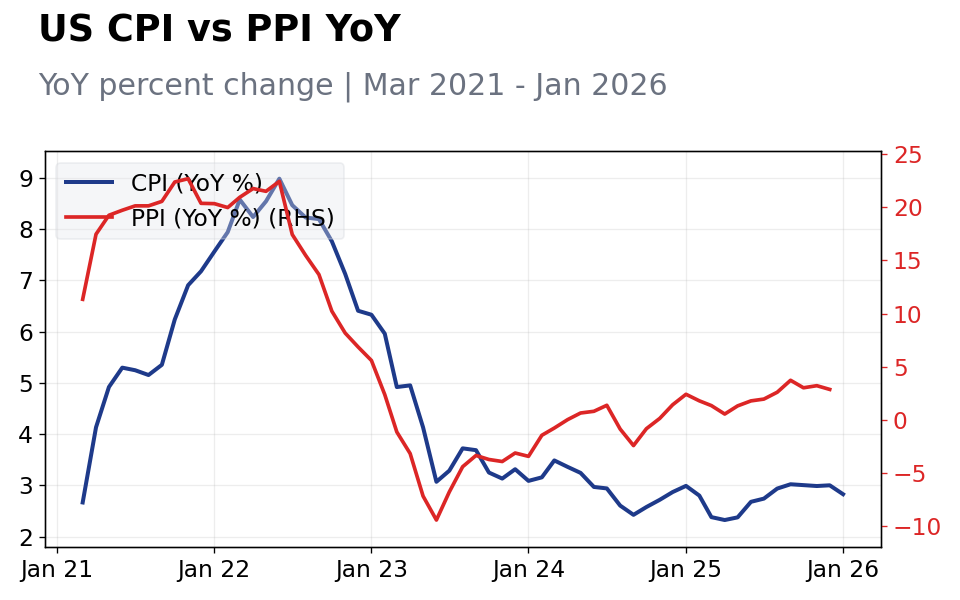

| Producer Price Index Month-over-Month | 0.50 | 0.30 | 03:30 |

| Core PPI Month-over-Month | 0.70 | 0.30 | 03:30 |

| Chicago PMI | 54 | 52.80 | 04:45 |

- US equities ended mixed, with Nasdaq lagging on tech weakness, while yields rose on resilient signals.

- Data showed softening factory orders and mixed manufacturing activity, offset by rising consumer confidence.

- Fed speakers maintained cautious tones, tempering rate cut expectations.

Yesterday's Recap

US markets closed mixed as the S&P 500 fell 0.54% to 6,908.86, pressured by tech declines, while the Dow Jones rose 0.03% to 49,499.20 on industrial gains. Nasdaq 100 dropped 1.16% to 25,034.37, amid profit-taking in growth stocks and higher yields. Russell 2000 gained 0.52% to 2,677.29, showing small-cap strength.

Treasury yields increased, with the 10-year up 0.25% to 4.05% and the 2-year up 0.58% to 3.45%, reflecting digestion of softer data. Factory orders fell 0.7% month-over-month, below consensus of -0.5% and previous 2.7%, indicating weaker industrial demand. Dallas Fed Manufacturing Index rose to 0.2 from -1.2, a positive note.

Chicago Fed National Activity Index was mixed, with readings of 0.18 and -0.21. S&P/Case-Shiller Home Price Index held at 1.4% year-over-year, matching consensus and prior. Consumer confidence improved to 91.2 from 89.0.

ADP Employment Change rose to 12,750 from 11,500. Currency moves were subdued: USD/JPY down 0.23% to 155.85, EUR/USD down 0.05% to 1.18, GBP/USD down 0.62% to 1.35. Gold rose 0.53% to 5,203.90 on safe-haven demand, WTI crude surged 2.44% to 66.80 amid tensions, and Bitcoin fell 2.06% to 66,066.92.

The Day Ahead

Focus shifts to Producer Price Index month-over-month at 3:30 ET, with consensus at 0.3% after previous 0.5%, potentially signaling inflation trends and affecting Fed cut odds. Core PPI month-over-month, also at 3:30 ET, carries medium impact and could highlight underlying pressures. Investors watch for any Fed speaker remarks, building on recent comments, to gauge policy direction.

Broader attention includes monitoring fiscal updates post-Trump's State of the Union, which touted economic strength but faced fact-checks on distortions. Expect equity and currency volatility as markets position for global risks.

Other Economic Notes

The US economy grew 2.2% in 2025 despite near-zero net job additions, widening inequality in a K-shaped recovery where asset owners thrive while others lag. Economists like Mark Zandi warn of market-economy decoupling driven by speculation, raising sell-off risks amid tariff and AI concerns. (cont...)