US Macro Daily(Beta Mode)

Services PMI Beats, Stocks Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,869.50 | +0.78% |

| Nasdaq 100 | 25,093.68 | +1.51% |

| Dow Jones | 48,739.41 | +0.49% |

| Russell 2000 | 2,636.01 | +1.06% |

| USD/JPY | 157.35 | -0.27% |

| EUR/USD | 1.16 | +0.02% |

| GBP/USD | 1.34 | +0.05% |

| Gold | 5,174.10 | +1.05% |

| WTI Crude | 76.94 | +3.05% |

| Bitcoin | 72,855.46 | +0.20% |

| US 2Y Treasury | 3.51% | +1.15% |

| US 10Y Treasury | 4.06% | +0.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ISM Manufacturing PMI | 52.60 | 51.80 | 52.40 |

| ISM Manufacturing Employment | 48.10 | - | 48.80 |

| Speech by Fed's Williams | - | - | - |

| Speech by Fed's Kashkari | - | - | - |

| API Weekly Crude Oil Stocks | 11.4m | 2.2m | 5.6m |

| MBA 30-Year Mortgage Rate | 6.09 | - | 6.09 |

| ADP Employment Change | 11,000 | 50,000 | 63,000 |

| Services Sector PMI | 53.80 | 53.50 | 56.10 |

| EIA Weekly Crude Oil Inventory | 16.0m | 2.3m | 3.5m |

| EIA Weekly Gasoline Inventory | -1.0m | -800,000 | -1.7m |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Export Prices Month-over-Month | 0.30 | 0.30 | 03:30 |

| Import Prices Month-over-Month | 0.10 | 0.20 | 03:30 |

| Nonfarm Productivity Quarter-over-Quarter Prel | 4.90 | 1.90 | 03:30 |

| Unit Labour Costs Quarter-over-Quarter Prel | -1.90 | 2 | 03:30 |

| Weekly Jobless Claims | 212,000 | 215,000 | 03:30 |

- US Services PMI surged to 56.1, beating consensus and signaling strong sector growth amid inflation worries.

- Equities advanced, Nasdaq up 1.51% on tech momentum, oil jumped 3.05% on Middle East risks.

- Fed speakers noted Iran war uncertainty, reducing odds of near-term rate cuts.

Yesterday's Recap

Yesterday's US data featured positive surprises, with Services Sector PMI at 56.1, topping consensus of 53.5 and prior 53.8, highlighting robust non-manufacturing expansion that may stoke inflation concerns. ADP Employment Change showed 63,000 jobs added, exceeding 50,000 forecast and 11,000 previous, pointing to labor market strength before official payrolls. EIA Crude Oil Inventory rose 3.475 million barrels, above 2.3 million expected and 15.989 million prior, while Gasoline Inventory fell -1.704 million versus -0.8 million consensus.

Despite inventory builds, WTI Crude climbed 3.05% to 76.94 amid geopolitical tensions. MBA 30-Year Mortgage Rate held at 6.09%, unchanged. Equity markets gained, with S&P 500 up 0.78% to 6,869.50, Nasdaq 100 +1.51% to 25,093.68, Dow Jones +0.49% to 48,739.41, and Russell 2000 +1.06% to 2,636.01.

Treasury yields rose slightly, US 10Y to 4.06% (+0.25%), US 2Y to 3.51% (+1.15%). USD/JPY dipped -0.27% to 157.35, EUR/USD +0.02% to 1.16, GBP/USD +0.05% to 1.34. Gold rose 1.05% to 5,174.10, Bitcoin +0.20% to 72,855.46.

The Day Ahead

Today's calendar includes medium-impact US data at 3:30 ET: Export Prices MoM expected at 0.3% (prev 0.3%), Import Prices MoM at 0.2% (prev 0.1%), offering clues on trade inflation. Nonfarm Productivity QoQ preliminary at 1.9% (prev 4.9%), Unit Labor Costs QoQ at 2% (prev -1.9%), which could shape views on wages and efficiency. Weekly Jobless Claims consensus 215,000 (prev 212,000), key for labor trends.

No high-impact events, but surprises may influence sentiment amid Middle East developments. Watch for unscheduled Fed comments or global news driving volatility.

Other Economic Notes

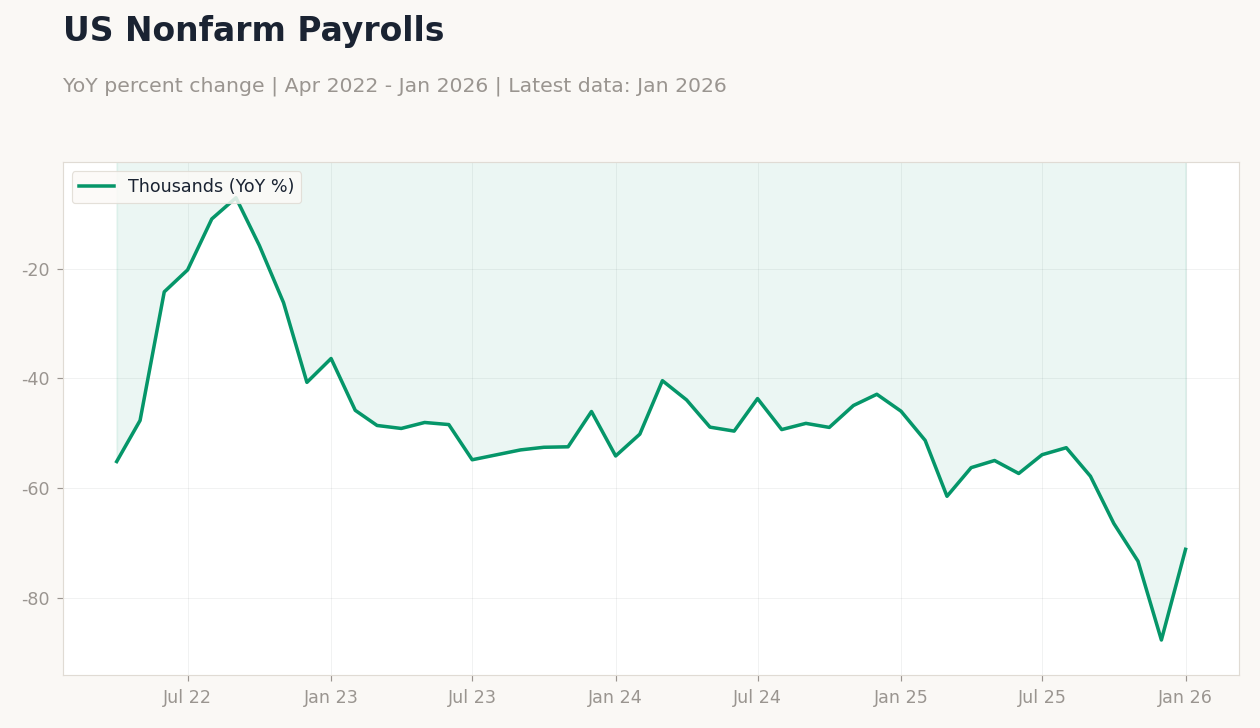

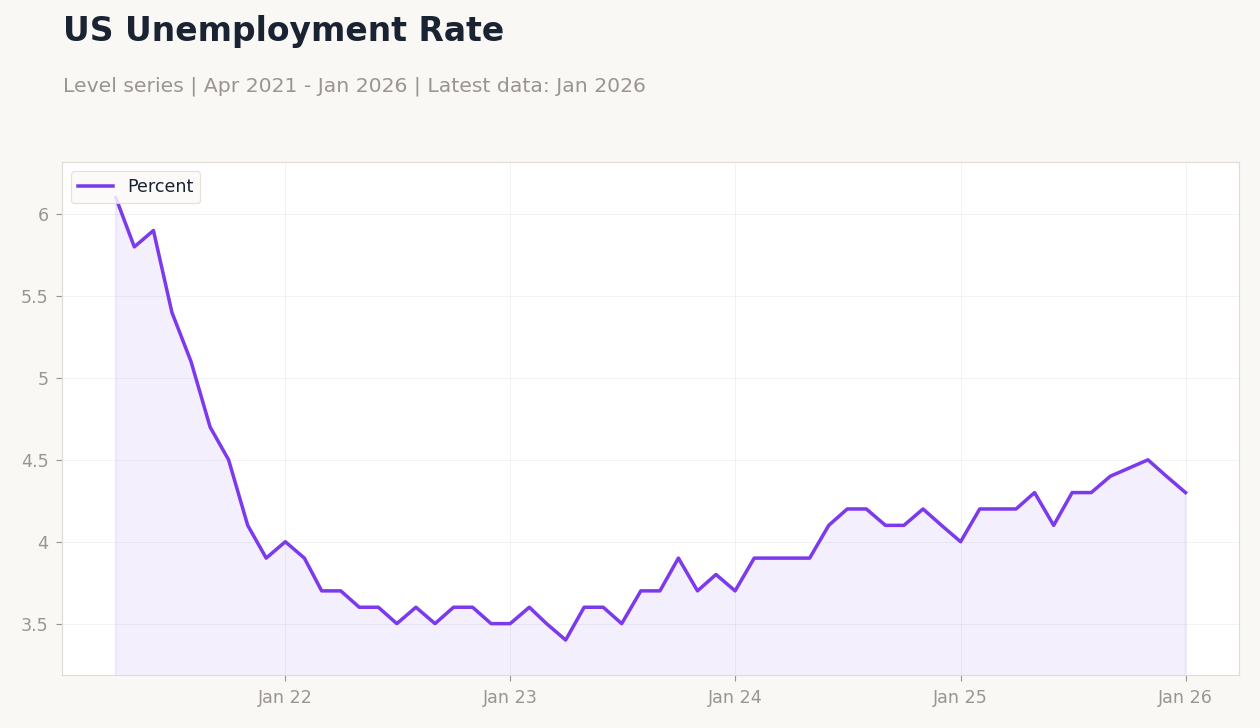

US economy shows resilience with inflation above target, as CPI YoY stands at 2.31%. Unemployment at 4.30% reflects a solid job market supporting spending but risking wage pressures. Middle East conflict raises energy costs, potentially disrupting supply chains and complicating Fed easing path.

Recent data like strong services activity underscores growth but highlights persistent price risks.