US Macro Daily(Beta Mode)

Home Sales Beat, Stocks Dip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,781.48 | -0.21% |

| Nasdaq 100 | 24,956.47 | -0.04% |

| Dow Jones | 47,706.51 | -0.07% |

| Russell 2000 | 2,548.08 | -0.22% |

| USD/JPY | 158.27 | +0.27% |

| EUR/USD | 1.16 | -0.06% |

| GBP/USD | 1.34 | +0.16% |

| Gold | 5,196.20 | -0.64% |

| WTI Crude | 85.60 | +2.58% |

| Bitcoin | 69,603.27 | -0.46% |

| US 2Y Treasury | 3.56% | +0.00% |

| US 10Y Treasury | 4.12% | -0.72% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ADP Employment Change Weekly | 12,750 | - | 15,500 |

| Existing Home Sales | 4.0m | 3.9m | 4.1m |

| Existing Home Sales Month-over-Month | -8.40 | - | 1.70 |

| API Weekly Crude Oil Stocks | 5.6m | 1.4m | -1.7m |

| MBA 30-Year Mortgage Rate | 6.09 | - | - |

US Existing Home Sales | Type: macro_line | Home Sales (SAAR): 4.09e+06 (2026-02-01) | Range: 3.98e+06–4.27e+06 | Trend(5pt): 4.15e+06,4.04e+06,4.03e+06,4.09e+06,4.09e+06

US Existing Home Sales | Type: macro_line | Home Sales (SAAR): 4.09e+06 (2026-02-01) | Range: 3.98e+06–4.27e+06 | Trend(5pt): 4.15e+06,4.04e+06,4.03e+06,4.09e+06,4.09e+06

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Core Inflation Rate Month-over-Month | 0.30 | 0.20 | 04:30 |

| Core Inflation Rate Year-over-Year | 2.50 | 2.50 | 04:30 |

| Inflation Rate Month-over-Month | 0.20 | 0.30 | 04:30 |

| Inflation Rate Year-over-Year | 2.40 | 2.40 | 04:30 |

| Consumer Price Index | 325.25 | 326.79 | 04:30 |

| Consumer Price Index SA | 326.59 | - | 04:30 |

| Speech by Fed's Bowman | - | - | 04:30 |

| EIA Weekly Crude Oil Inventory | 3.5m | 2.8m | 06:30 |

| EIA Weekly Gasoline Inventory | -1.7m | - | 06:30 |

| Monthly Budget Statement | -95,000m | -75,850m | 10:00 |

- Existing home sales topped forecasts, showing housing strength despite rates.

- Equities closed slightly lower amid geopolitical worries.

- Oil stocks drew down, lifting crude prices.

Yesterday's Recap

US existing home sales surprised higher at 4.09 million units annually, beating consensus of 3.89 million, with a month-over-month rise of 1.7% after January's -8.4% decline. ADP weekly employment change increased to 15,500 from 12,750 prior, pointing to labor market vigor. API crude oil stocks dropped by 1.7 million barrels, against expectations of a 1.4 million build and prior 5.6 million gain, helping WTI crude climb 2.58% to $85.60.

MBA 30-year mortgage rate was unreleased, holding at prior 6.09%. Markets ended modestly down: S&P 500 -0.21% to 6,781.48, Nasdaq 100 -0.04% to 24,956.47, Dow Jones -0.07% to 47,706.51, Russell 2000 -0.22% to 2,548.08. Treasury yields fell, with 10-year down 0.72% to 4.12% and 2-year flat at 3.56%, on safe-haven bids.

USD/JPY rose 0.27% to 158.27, EUR/USD dipped 0.06% to 1.16, GBP/USD gained 0.16% to 1.34. Gold fell 0.64% to 5,196.20, Bitcoin slipped 0.46% to 69,603.27.

The Day Ahead

Core inflation month-over-month expected at 0.2% vs prior 0.3%, year-over-year steady at 2.5%. Headline inflation month-over-month at 0.3% from 0.2%, year-over-year at 2.4%. Consumer Price Index forecast at 326.79 from 325.25.

Fed's Bowman speaks at 04:30 ET, possibly on policy outlook. EIA crude oil inventory eyed for 2.8 million barrel build after prior 3.475 million, plus gasoline stocks. Monthly budget statement consensus at -75.85 billion vs prior -95 billion.

Other Economic Notes

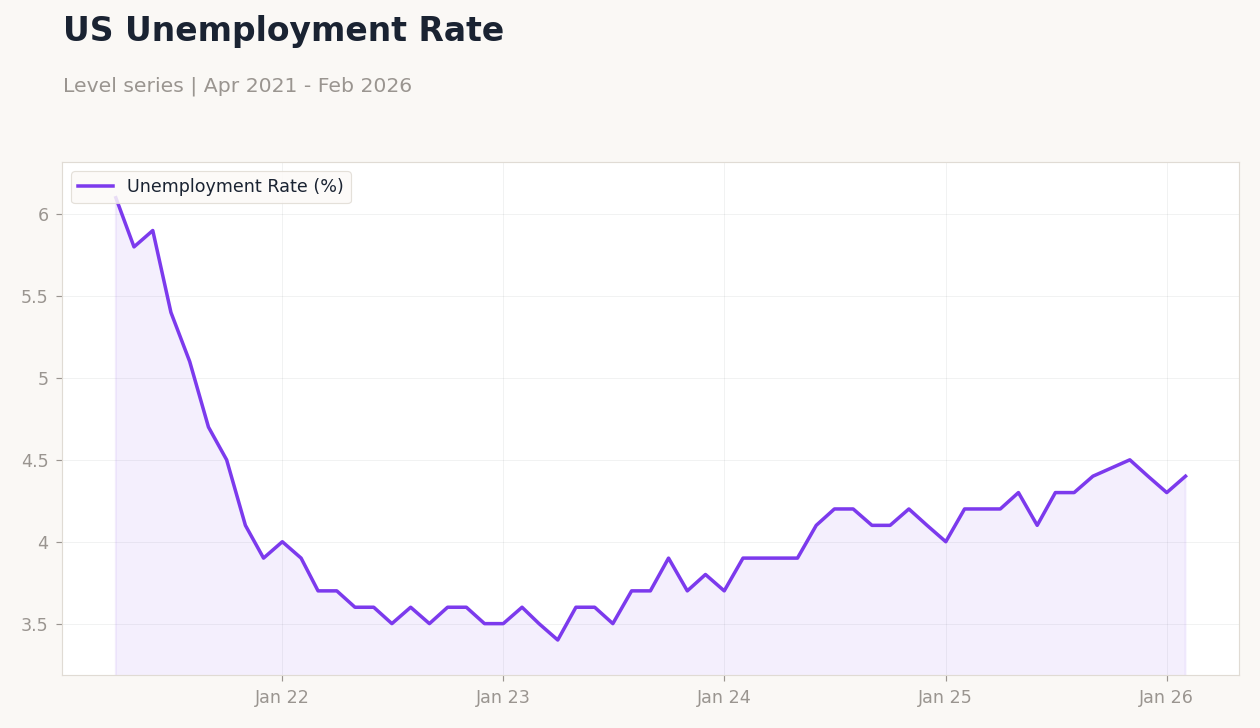

Housing resilience evident in sales beat despite mortgage rates near 6%, aiding economic stability. Labor data like ADP gain aligns with unemployment at 4.40% as of February, bolstering soft-landing views but monitoring wage effects. Climate reports highlight worsening allergies from warming, posing health and economic risks.

Global Macro News

Iran war tensions disrupt markets, spiking energy and commodity prices, risking food shortages in vulnerable nations. Oil prices swung, with WTI up 2.58% yesterday but easing below $90 after Trump's remark that the war seems nearly over, boosting Asian shares. Wall Street mixed amid volatility, with Dow, S&P 500, Nasdaq lower on war signals.

(cont...)