US Macro Daily(Beta Mode)

Stocks Tumble on Iran Tensions

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,672.62 | -1.52% |

| Nasdaq 100 | 24,533.58 | -1.73% |

| Dow Jones | 46,677.85 | -1.56% |

| Russell 2000 | 2,488.99 | -2.12% |

| USD/JPY | 159.38 | +0.19% |

| EUR/USD | 1.15 | -0.71% |

| GBP/USD | 1.33 | -0.90% |

| Gold | 5,099.60 | -0.32% |

| WTI Crude | 93.76 | -2.06% |

| Bitcoin | 72,425.18 | +2.74% |

| US 2Y Treasury | 3.64% | +1.96% |

| US 10Y Treasury | 4.21% | +1.45% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ADP Employment Change Weekly | 12,750 | - | 15,500 |

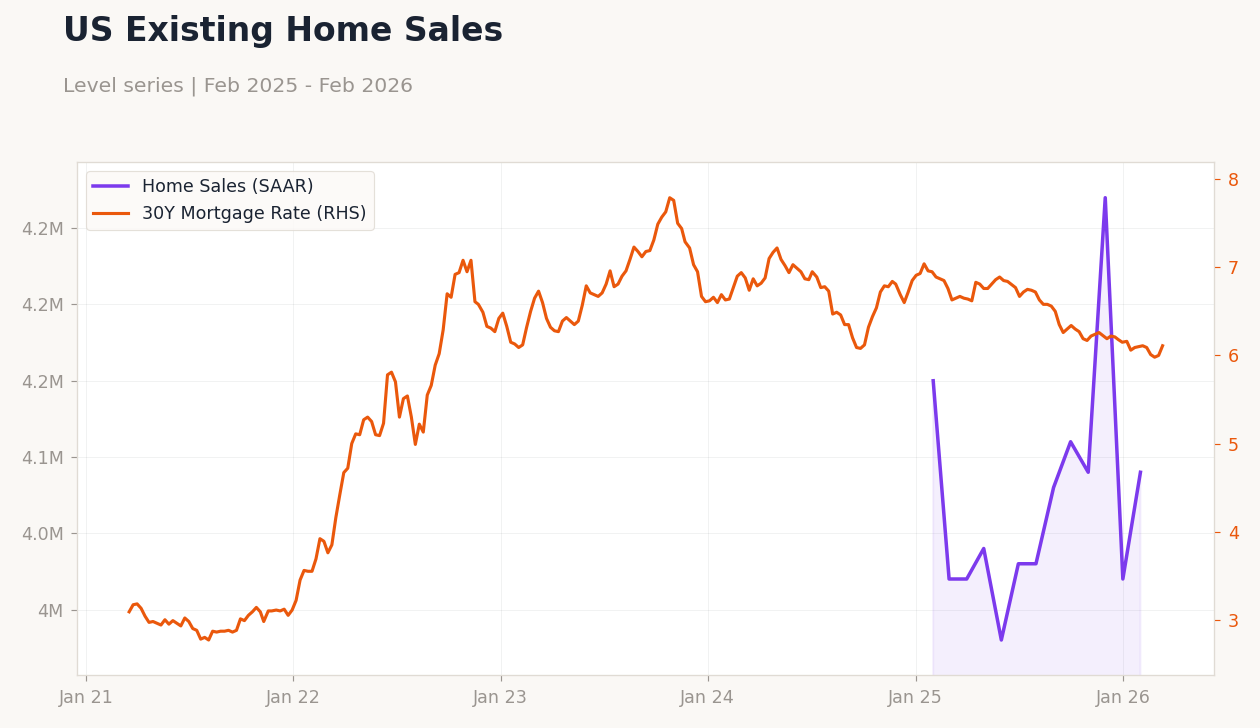

| Existing Home Sales | 4.0m | 3.9m | 4.1m |

| Existing Home Sales Month-over-Month | -8.40 | - | 1.70 |

| API Weekly Crude Oil Stocks | 5.6m | 1.4m | -1.7m |

| MBA 30-Year Mortgage Rate | 6.09 | - | 6.19 |

| Core Inflation Rate Month-over-Month | 0.30 | 0.20 | 0.20 |

| Core Inflation Rate Year-over-Year | 2.50 | 2.50 | 2.50 |

| Inflation Rate Month-over-Month | 0.20 | 0.30 | 0.30 |

| Inflation Rate Year-over-Year | 2.40 | 2.40 | 2.40 |

| Consumer Price Index | 325.25 | 326.79 | 326.79 |

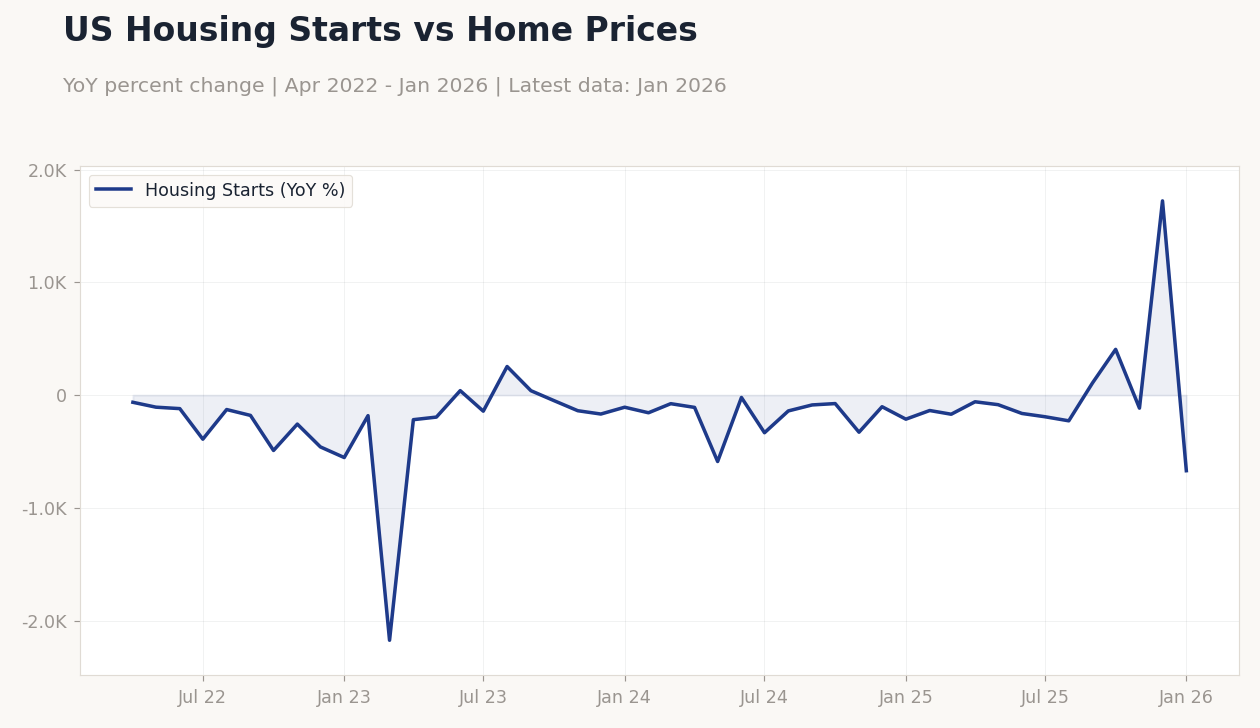

US Housing Starts vs Home Prices | Type: macro_line | Housing Starts: 9.499 (2026-01-01) | Range: -25.6–59.72 | Trend(6pt): 59.72,-6,-13.98,-1.17,-8.388,9.499

US Housing Starts vs Home Prices | Type: macro_line | Housing Starts: 9.499 (2026-01-01) | Range: -25.6–59.72 | Trend(6pt): 59.72,-6,-13.98,-1.17,-8.388,9.499

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Core PCE Price Index Month-over-Month | 0.40 | 0.40 | 04:30 |

| Durable Goods Orders Month-over-Month | -1.40 | 1.20 | 04:30 |

| GDP Growth Quarter-over-Quarter Second Estimate | 4.40 | 1.40 | 04:30 |

| Personal Income Month-over-Month | 0.30 | 0.50 | 04:30 |

| Personal Spending Month-over-Month | 0.40 | 0.30 | 04:30 |

| Durable Goods Orders Ex Transp Month-over-Month | 0.90 | 0.50 | 04:30 |

| GDP Price Index Quarter-over-Quarter 2nd Est | 3.70 | - | 04:30 |

| PCE Price Index Month-over-Month | 0.40 | 0.30 | 04:30 |

| PCE Price Index Year-over-Year | 2.90 | 2.90 | 04:30 |

| JOLTs Job Openings | 6.5m | 6.7m | 06:00 |

- US inflation met expectations at 2.4% YoY, with core steady at 2.5%, signaling stable prices.

- Existing home sales beat consensus at 4.09M units, up 1.7% MoM, despite rising mortgage rates.

- Equities dropped over 1.5%, hit by oil volatility and Middle East war risks.

Yesterday's Recap

US inflation data met forecasts, with YoY rate at 2.4% and core at 2.5%, while MoM figures were 0.3% and 0.2% respectively, supporting a balanced price outlook. Existing home sales exceeded expectations at 4.09 million units, rising 1.7% MoM versus consensus of 3.89 million, indicating strong housing demand even as MBA 30-year mortgage rates climbed to 6.19%. ADP employment change increased to 15,500 from 12,750 prior, reflecting solid job gains.

Oil data was mixed: API crude stocks fell unexpectedly by 1.7 million barrels against a 1.4 million build consensus, while EIA showed a 3.824 million barrel rise versus 1.1 million expected, pressuring WTI crude down 2.06% to $93.76. Equity indices declined sharply, with S&P 500 off 1.52% at 6,672.62, Nasdaq 100 down 1.73% at 24,533.58, Dow Jones falling 1.56% at 46,677.85, and Russell 2000 dropping 2.12% at 2,488.99, amid escalating geopolitical concerns. Treasury yields increased, with 2-year up 1.96% to 3.64% and 10-year rising 1.45% to 4.21%, driven by persistent inflation and safe-haven demand.

Currencies shifted: USD/JPY gained 0.19% to 159.38, while EUR/USD fell 0.71% to 1.15 and GBP/USD dropped 0.90% to 1.33, as the dollar benefited from risk aversion.

The Day Ahead

Focus shifts to Core PCE Price Index MoM, a key Fed inflation gauge, for clues on policy direction after steady CPI. Markets await updates on geopolitical tensions, which could sway energy prices and risk assets. Treasury auctions and any fiscal announcements may influence yields, while ongoing oil reserve releases could ease supply pressures.

Other Economic Notes

The US economy shows resilience with unemployment at 4.40%, but February's 92,000 job losses signal potential softening amid global disruptions. CPI YoY at 2.31% faces upside risks from energy price spikes due to Middle East conflicts, possibly delaying rate cuts. Housing remains robust per sales data, though 6.19% mortgage rates may curb future growth.

Stagflation concerns emerge as oil volatility weighs on activity, with Treasury predicting a strong 2026 despite challenges.