US Macro Daily(Beta Mode)

Stocks Dip on War Jitters

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,632.19 | -0.61% |

| Nasdaq 100 | 24,380.73 | -0.62% |

| Dow Jones | 46,558.47 | -0.26% |

| Russell 2000 | 2,480.05 | -0.36% |

| USD/JPY | 159.23 | +0.01% |

| EUR/USD | 1.15 | -0.38% |

| GBP/USD | 1.33 | -0.60% |

| Gold | 4,999.20 | -1.05% |

| WTI Crude | 97.23 | -1.50% |

| Bitcoin | 73,680.74 | +1.22% |

| US 2Y Treasury | 3.76% | +3.30% |

| US 10Y Treasury | 4.27% | +1.43% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

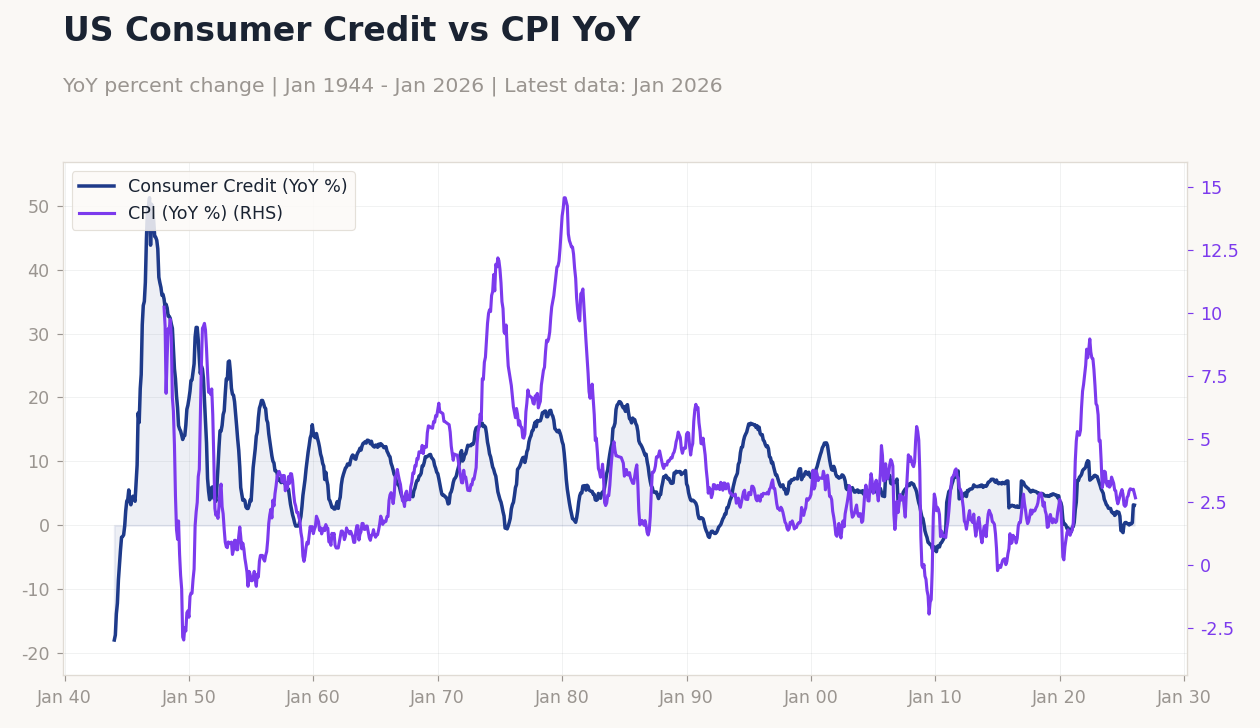

US Consumer Credit vs CPI YoY | Type: macro_line | Consumer Credit: 3.161 (2026-01-01) | Range: -1.135–10.11 | Trend(6pt): 2.456,7.07,4.071,2.047,3.205,3.161 | CPI: 2.665 (2026-02-01) | Range: 2.325–8.979 | Trend(6pt): 4.133,8.979,3.723,2.579,2.829,2.665

US Consumer Credit vs CPI YoY | Type: macro_line | Consumer Credit: 3.161 (2026-01-01) | Range: -1.135–10.11 | Trend(6pt): 2.456,7.07,4.071,2.047,3.205,3.161 | CPI: 2.665 (2026-02-01) | Range: 2.325–8.979 | Trend(6pt): 4.133,8.979,3.723,2.579,2.829,2.665

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| NY Empire State Manufacturing Index | 7.10 | 3.80 | 04:30 |

| Industrial Production Month-over-Month | 0.70 | 0.20 | 05:15 |

| NAHB Housing Market Index | 36 | 37 | 06:00 |

| Tuesday (2026-03-17) | |||

| ADP Employment Change Weekly | 15,500 | - | 04:15 |

| Pending Home Sales Month-over-Month | -0.80 | -1 | 06:00 |

| Pending Home Sales Year-over-Year | -0.40 | - | 06:00 |

| API Weekly Crude Oil Stocks | -1.7m | - | 12:30 |

| Wednesday (2026-03-18) | |||

| MBA 30-Year Mortgage Rate | 6.19 | - | 03:00 |

- US stocks fell amid US-Iran war tensions, with S&P 500 down 0.61%.

- Treasury yields climbed as markets eyed Fed caution on inflation.

- Oil dropped 1.50% despite US reserve release, easing supply fears.

Yesterday's Recap

US markets closed lower on March 15, with the S&P 500 dropping 0.61% to 6,632.19 amid heightened geopolitical tensions from the ongoing US-Iran war. The Nasdaq 100 fell 0.62% to 24,380.73, pressured by tech sector weakness, while the Dow Jones eased 0.26% to 46,558.47 and Russell 2000 declined 0.36% to 2,480.05. Treasury yields climbed, with the 2-year rising 3 basis points to 3.76% and 10-year up 1 basis point to 4.27%, as investors braced for persistent inflation from elevated oil prices.

Currency markets saw EUR/USD weaken 0.38% to 1.15 and GBP/USD drop 0.60% to 1.33, while USD/JPY edged up 0.01% to 159.23. Gold prices slipped 1.05% to 4,999.20, diverging from safe-haven trends, and WTI crude fell 1.50% to 97.23 despite supply disruption fears. Bitcoin rose 1.22% to 73,680.74 on institutional demand.

No major data releases occurred, but lingering concerns over February's job losses of 92,000 fueled risk aversion.

The Day Ahead

Today's US calendar features the NY Empire State Manufacturing Index at 4:30 ET, with consensus at 3.8 versus previous 7.10, potentially signaling regional factory activity slowdown. Industrial Production MoM follows at 5:15 ET, expected at 0.2% after 0.7%, offering insights into manufacturing health amid energy cost pressures. The NAHB Housing Market Index at 6:00 ET is forecasted at 37 from 36, reflecting builder sentiment in a high-rate environment.

Tomorrow brings ADP Employment Change Weekly at 4:15 ET, with no consensus but previous at 15,500, alongside Pending Home Sales MoM at 6:00 ET expected at -1% from -0.8%. API Weekly Crude Oil Stocks at 12:30 ET will gauge inventory shifts amid war-related volatility. Wednesday includes high-impact Producer Price Index MoM at 4:30 ET, consensus 0.3% from 0.5%, which could influence Fed rate expectations.

Other Economic Notes

Broader US economic themes highlight resilience in unemployment at 4.40% as of February, supporting consumer spending despite inflationary pressures from the US-Iran conflict. CPI YoY stands at 2.31%, underscoring moderating price growth but with risks from rising energy costs potentially reigniting upward trends. Commercial real estate faces heightened risks, as noted by Deutsche Bank, amid tighter credit conditions and office vacancy pressures.