US Macro Daily(Beta Mode)

Fed Holds, PPI Beats

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,606.49 | -0.27% |

| Nasdaq 100 | 24,355.28 | -0.29% |

| Dow Jones | 46,021.43 | -0.44% |

| Russell 2000 | 2,494.71 | +0.65% |

| USD/JPY | 158.72 | -0.67% |

| EUR/USD | 1.16 | +0.86% |

| GBP/USD | 1.34 | +0.86% |

| Gold | 4,653.80 | +1.15% |

| WTI Crude | 95.90 | -0.25% |

| Bitcoin | 70,585.95 | +0.96% |

| US 2Y Treasury | 3.76% | +2.17% |

| US 10Y Treasury | 4.26% | +1.43% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| NY Empire State Manufacturing Index | 7.10 | 3.20 | -0.20 |

| Industrial Production Month-over-Month | 0.70 | 0.10 | 0.20 |

| NAHB Housing Market Index | 37 | 37 | 38 |

| ADP Employment Change Weekly | 14,750 | - | 9,000 |

| Pending Home Sales Month-over-Month | -1 | -0.50 | 1.80 |

| Pending Home Sales Year-over-Year | -0.40 | - | -0.80 |

| API Weekly Crude Oil Stocks | -1.7m | -600,000 | 6.6m |

| MBA 30-Year Mortgage Rate | 6.19 | - | 6.30 |

| Producer Price Index Month-over-Month | 0.50 | 0.30 | 0.70 |

| Core Producer Price Index Month-over-Month | 0.80 | 0.30 | 0.50 |

US PPI Monthly Growth | Type: macro_line | PPI MoM %: 3.218 (2026-02-01) | Range: -9.417–22.69 | Trend(6pt): 17.47,22.43,-4.402,-0.8272,2.998,3.218

US PPI Monthly Growth | Type: macro_line | PPI MoM %: 3.218 (2026-02-01) | Range: -9.417–22.69 | Trend(6pt): 17.47,22.43,-4.402,-0.8272,2.998,3.218

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Saturday (2026-03-21) | |||

| Speech by Fed's Chair Powell | - | - | 09:30 |

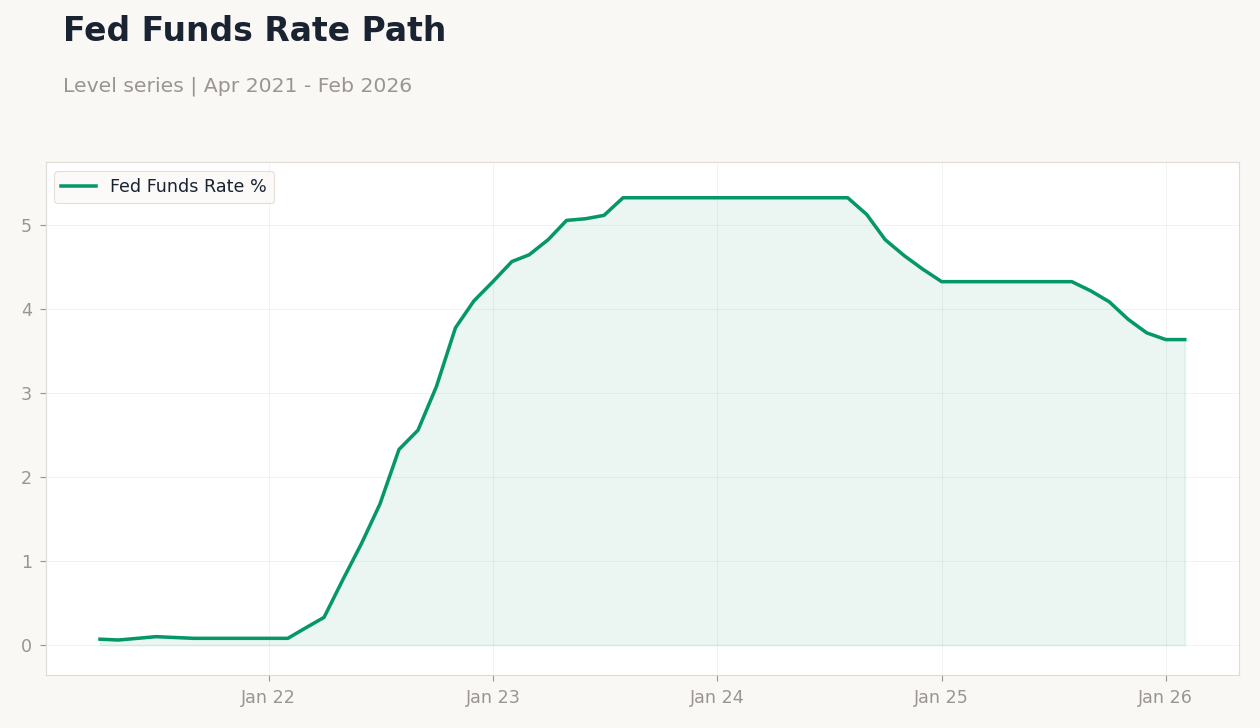

- Fed maintains rates at 3.75% amid sticky inflation, with projections signaling caution on cuts.

- PPI surges to 0.7% MoM, exceeding consensus, pressuring yields higher.

- Equities dip modestly, oil inventories build, signaling mixed economic signals.

Yesterday's Recap

US economic data released over the past few days showed mixed signals, with the NY Empire State Manufacturing Index dropping to -0.20, missing the consensus of 3.2 and indicating contraction in regional activity. Industrial Production edged up 0.2% MoM, slightly above the 0.1% forecast, reflecting modest factory output growth. The NAHB Housing Market Index ticked up to 38, beating expectations of 37, suggesting slight improvement in builder sentiment.

ADP Employment Change came in at 9000, lower than the previous 14750, pointing to softening labor trends, while Pending Home Sales rose 1.8% MoM, surpassing the -0.5% consensus and offering a positive note for housing. Producer Price Index jumped 0.7% MoM, hotter than the 0.3% expected, with Core PPI at 0.5% versus 0.3%, fueling inflation concerns. Oil inventories built significantly, with API Crude at 6.6 million barrels and EIA at 6.156 million, against draws expected, contributing to WTI's -0.25% dip to $95.90.

Markets reacted with S&P 500 down 0.27% to 6,606.49, Nasdaq 100 off 0.29% to 24,355.28, while Treasury yields rose, with 10Y at 4.26% up 1.43%.

The Day Ahead

Investors eye upcoming weekly jobless claims data, expected around 220K, which could reinforce labor market resilience amid the 4.40% unemployment rate. Building permits and housing starts for February are due, with consensus for slight declines, potentially impacting sentiment given recent Pending Home Sales strength. Philadelphia Fed Manufacturing Index may provide regional insights, forecasted at 4.0, following the Empire State's miss.

No major Fed speeches are scheduled, allowing markets to digest yesterday's hold decision. Attention turns to any updates on fiscal policy amid ongoing shutdown complications. Overall, these releases could influence rate cut odds if they signal cooling inflation or growth.

Other Economic Notes

Broader US themes highlight persistent inflation pressures, with CPI YoY at 2.31% and recent PPI beats suggesting supply chain strains amid geopolitical tensions. Labor market softness emerges, as Fed Chair Powell noted job creation nearing zero, aligning with 4.40% unemployment and lower ADP figures. Housing shows resilience in sales but faces headwinds from rising mortgage rates at 6.3%, potentially curbing demand.