US Macro Daily(Beta Mode)

Fed Holds Steady Amid Iran Tensions

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,506.48 | -1.51% |

| Nasdaq 100 | 23,898.15 | -1.88% |

| Dow Jones | 45,577.47 | -0.96% |

| Russell 2000 | 2,438.45 | -2.26% |

| USD/JPY | 159.22 | +0.82% |

| EUR/USD | 1.16 | +0.97% |

| GBP/USD | 1.33 | -0.63% |

| Gold | 4,574.90 | -0.56% |

| WTI Crude | 98.23 | +2.17% |

| Bitcoin | 70,276.18 | -0.35% |

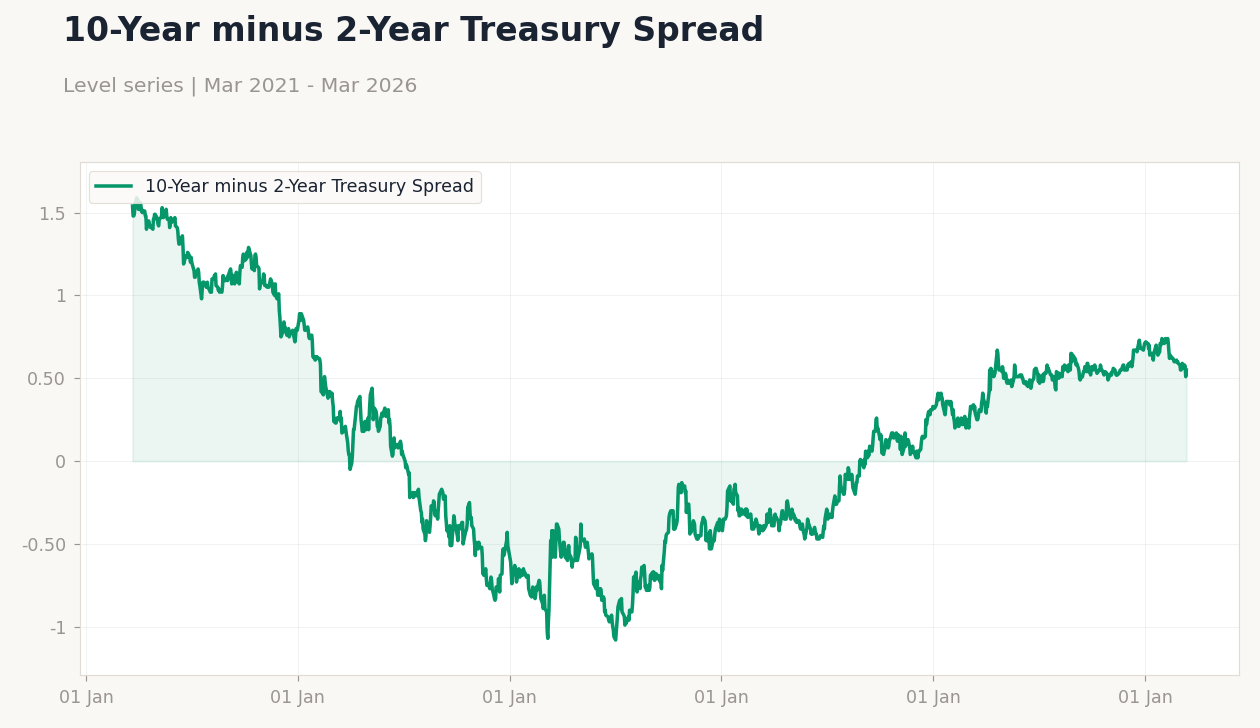

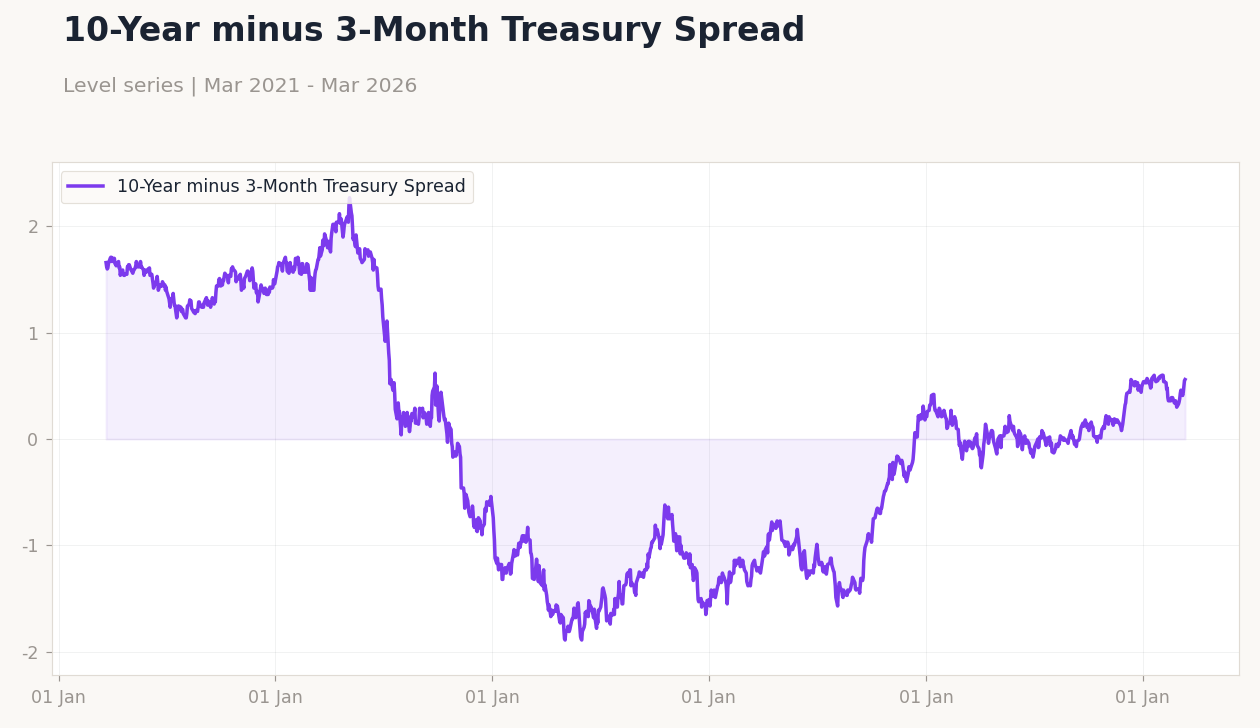

| US 2Y Treasury | 3.79% | +0.80% |

| US 10Y Treasury | 4.25% | -0.23% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Speech by Fed's Chair Powell | - | - | - |

US Fed Funds Rate | Type: macro_line | Effective Federal Funds Rate (%): 3.64 (2026-02-01) | Range: 0.06–5.33 | Trend(6pt): 0.07,1.21,5.33,4.83,3.72,3.64

US Fed Funds Rate | Type: macro_line | Effective Federal Funds Rate (%): 3.64 (2026-02-01) | Range: 0.06–5.33 | Trend(6pt): 0.07,1.21,5.33,4.83,3.72,3.64

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Monday (2026-03-23) | |||

| Chicago Fed National Activity Index | 0.18 | - | 08:30 |

| Tuesday (2026-03-24) | |||

| ADP Employment Change Weekly | 9,000 | - | 08:15 |

| S&P Global Composite PMI Flash | 51.90 | - | 09:45 |

| S&P Global Manufacturing PMI Flash | 51.60 | - | 09:45 |

| S&P Global Services PMI Flash | 51.70 | - | 09:45 |

| API Weekly Crude Oil Stocks | 6.6m | - | 16:30 |

| Speech by Fed's Barr | - | - | 18:30 |

| Wednesday (2026-03-25) | |||

- Federal Reserve keeps rates unchanged, projects one cut this year amid economic uncertainty and Iran conflict.

- US stocks tumble on weak GDP data and escalating Middle East tensions, with oil surging.

- Treasuries mixed as markets weigh safe-haven flows against inflation and war risks.

Yesterday's Recap

US markets closed sharply lower yesterday amid weak GDP figures and heightened geopolitical risks from the Iran conflict. The S&P 500 fell 1.51% to 6,506.48, pressured by broad risk aversion. The Nasdaq 100 dropped 1.88% to 23,898.15, hit by tech sector weakness, while the Dow Jones declined 0.96% to 45,577.47 and the Russell 2000 slid 2.26% to 2,438.45.

Treasury yields diverged, with the US 2Y rising 0.80% to 3.79% on inflation concerns, and the US 10Y easing 0.23% to 4.25% due to safe-haven demand. In currencies, USD/JPY gained 0.82% to 159.22 on yield spreads, EUR/USD advanced 0.97% to 1.16, and GBP/USD fell 0.63% to 1.33. Commodities showed splits: WTI Crude rose 2.17% to 98.23 on supply disruption fears, Gold dipped 0.56% to 4,574.90, and Bitcoin edged down 0.35% to 70,276.18.

News highlighted US GDP growth of just 0.7% last quarter, raising slowdown worries amid the war. The Federal Reserve held rates steady for the third straight meeting, with Chair Powell's speech noting data dependence and conflict uncertainties.

The Day Ahead

Key events this week include the Chicago Fed National Activity Index on Monday at 08:30 ET, following its prior 0.18 reading, offering early economic signals. Tuesday features ADP Employment Change Weekly at 08:15 ET after last week's 9,000, plus S&P Global PMI Flash for composite (prior 51.9), manufacturing (51.6), and services (51.7) at 09:45 ET. API Weekly Crude Oil Stocks arrive at 16:30 ET post a 6.6 million barrel build, with Fed's Barr speaking at 18:30 ET on policy amid tensions.

Wednesday brings MBA 30-Year Mortgage Rate at 07:00 ET after 6.3%, Current Account Balance at 08:30 ET following -226.4 billion, Export Prices MoM (prior 0.6%), and Import Prices MoM (prior 0.2%, consensus 0.2%). EIA Crude Oil Inventory (prior 6.156 million) and Gasoline Inventory (prior -5.436 million) release at 10:30 ET, critical for energy markets.

Other Economic Notes

US inflation trends show moderation with CPI YoY at 2.31%, yet above the Fed's 2% target, influencing policy caution. Unemployment holds at 4.40%, indicating labor strength that may sustain spending but could weaken under geopolitical strains. (cont...)