US Macro Daily(Beta Mode)

Manufacturing Dips, Oil Surges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 6,343.72 | -0.39% |

| Nasdaq 100 | 22,953.38 | -0.78% |

| Dow Jones | 45,216.14 | +0.11% |

| Russell 2000 | 2,414.01 | -1.46% |

| USD/JPY | 159.72 | -0.32% |

| EUR/USD | 1.15 | -0.26% |

| GBP/USD | 1.32 | -0.30% |

| Gold | 4,571.50 | +1.01% |

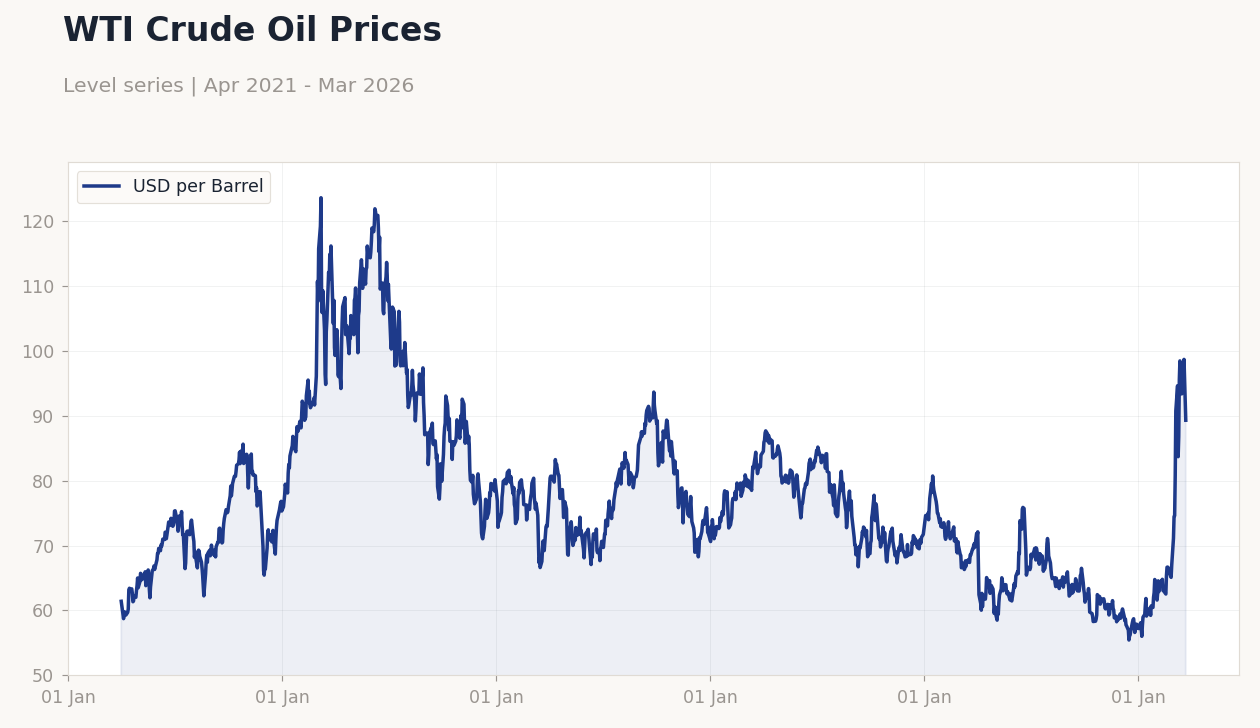

| WTI Crude | 104.80 | +1.87% |

| Bitcoin | 66,339.30 | -0.53% |

| US 2Y Treasury | 3.88% | -2.02% |

| US 10Y Treasury | 4.44% | +0.45% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Dallas Fed Manufacturing Index | 0.20 | - | -0.20 |

| Speech by Fed's Chair Powell | - | - | - |

| Speech by Fed's Williams | - | - | - |

WTI Crude Oil Prices | Type: macro_line | USD per Barrel: 89.33 (2026-03-23) | Range: 55.44–123.6 | Trend(6pt): 61.41,111.4,89.2,70.8,98.71,89.33

WTI Crude Oil Prices | Type: macro_line | USD per Barrel: 89.33 (2026-03-23) | Range: 55.44–123.6 | Trend(6pt): 61.41,111.4,89.2,70.8,98.71,89.33

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

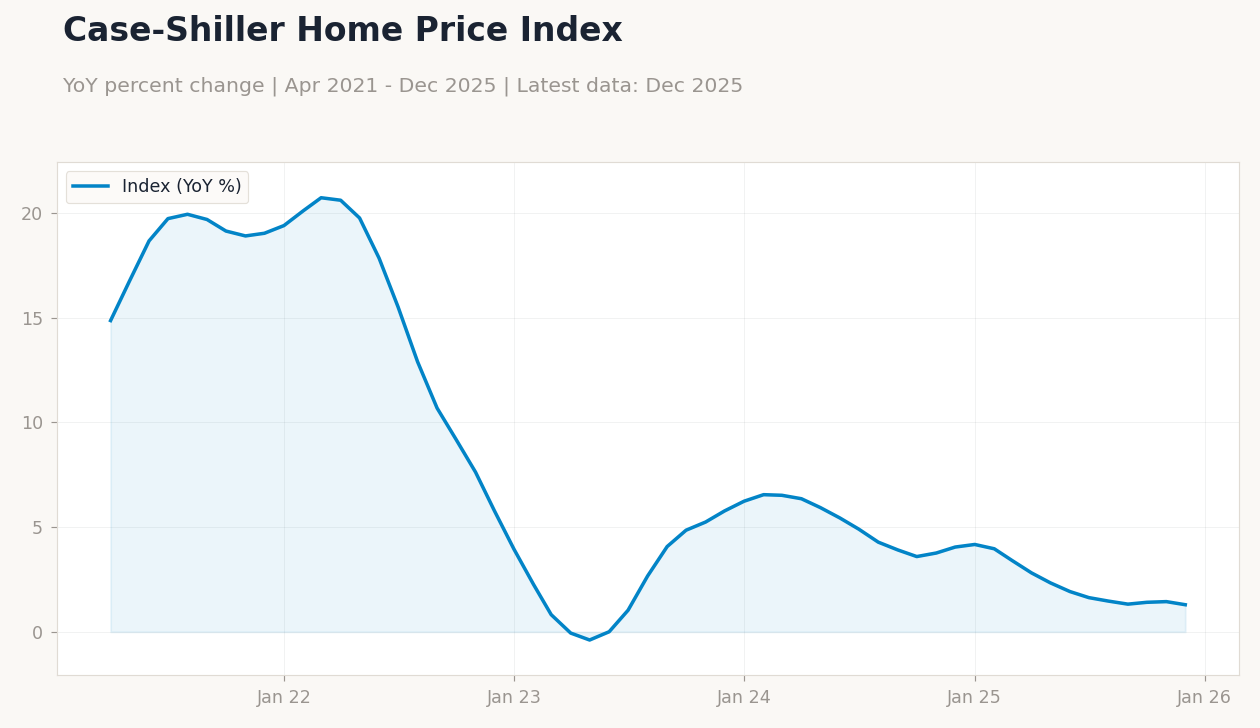

| S&P/Case-Shiller Home Price Year-over-Year | 1.40 | 1.30 | 05:00 |

| Chicago PMI | 57.70 | 55.80 | 05:45 |

| JOLTs Job Openings | 6.9m | 6.9m | 06:00 |

| Cb Consumer Confidence | 91.20 | - | 06:00 |

| Fed Goolsbee Speech | - | - | 08:00 |

| Speech by Fed's Barr | - | - | 11:00 |

| API Weekly Crude Oil Stocks | 2.3m | - | 12:30 |

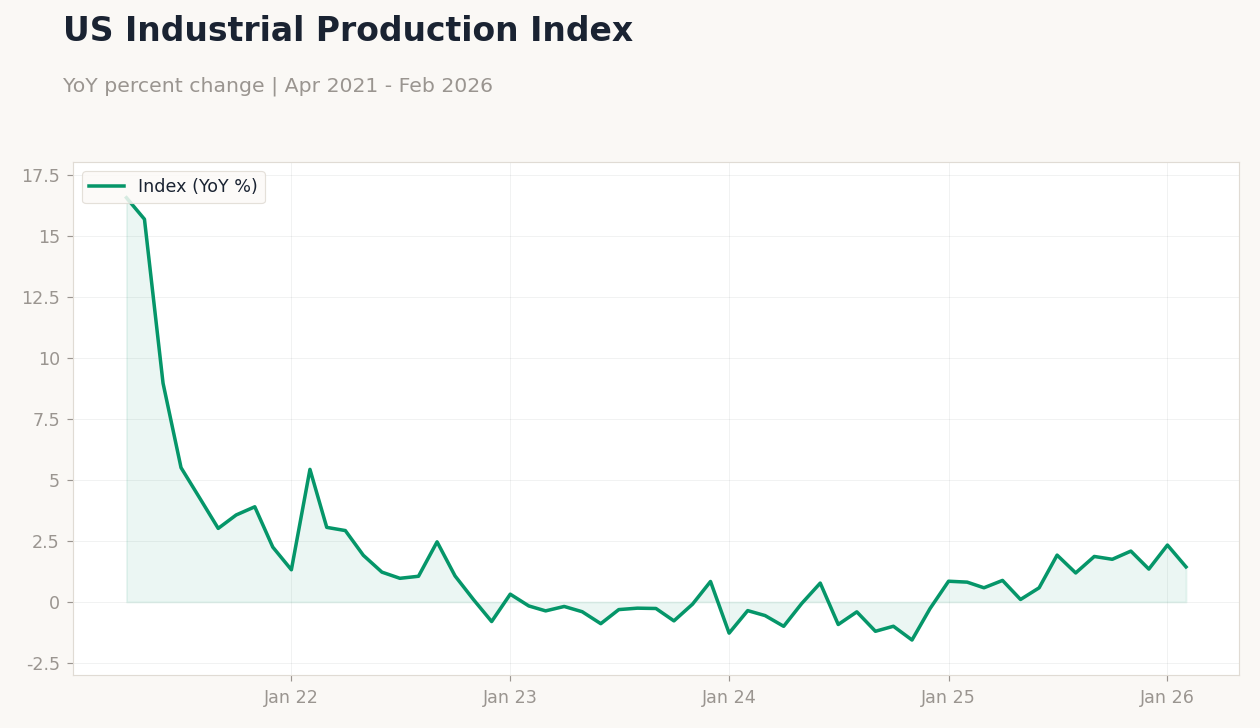

- Dallas Fed Manufacturing Index fell to -0.2, signaling slight contraction amid ongoing economic pressures.

- US equities declined, with S&P 500 down 0.39% and Nasdaq 100 off 0.78%, as Iran war fears boosted oil prices.

- Treasury yields mixed; 10Y rose 0.45% while 2Y fell 2.02%, reflecting inflation concerns from energy costs.

Yesterday's Recap

The Dallas Fed Manufacturing Index dropped to -0.2 in March from 0.2 previously, indicating a modest slowdown in regional factory activity and raising questions about broader manufacturing health. Fed Chair Powell delivered a speech emphasizing steady policy amid geopolitical risks, while New York Fed President Williams discussed inflation dynamics without signaling immediate rate changes. US equities closed lower, with the S&P 500 at 6,343.72 after a 0.39% decline, Nasdaq 100 at 22,953.38 down 0.78%, and Russell 2000 falling 1.46%, driven by war-related uncertainty.

The Dow Jones edged up 0.11% to 45,216.14, buoyed by defensive sectors. Oil prices climbed, with WTI Crude at $104.80 up 1.87%, as Middle East tensions escalated; gold rose 1.01% to $4,571.50 as a safe haven. Currency markets saw USD/JPY at 159.72 down 0.32%, EUR/USD at 1.15 off 0.26%, and GBP/USD at 1.32 down 0.30%, with the dollar weakening slightly.

Treasury yields diverged, as the 10Y increased to 4.44% while the 2Y dropped to 3.88%, amid bets on Fed caution.

The Day Ahead

Key releases include S&P/Case-Shiller Home Price YoY at 5:00 ET, expected at 1.3% from 1.4% prior, offering insights into housing market resilience. Chicago PMI follows at 5:45 ET, forecasted at 55.8 versus 57.7 last, potentially signaling manufacturing trends. High-impact JOLTs Job Openings at 6:00 ET are projected at 6.87 million from 6.946 million, alongside CB Consumer Confidence, which could influence labor market views.

Fed's Goolsbee speaks at 8:00 ET and Barr at 11:00 ET, with focus on rate path commentary. API Weekly Crude Oil Stocks at 12:30 ET may drive energy prices amid war volatility. Markets will watch for any dovish Fed signals amid elevated oil costs.

Other Economic Notes

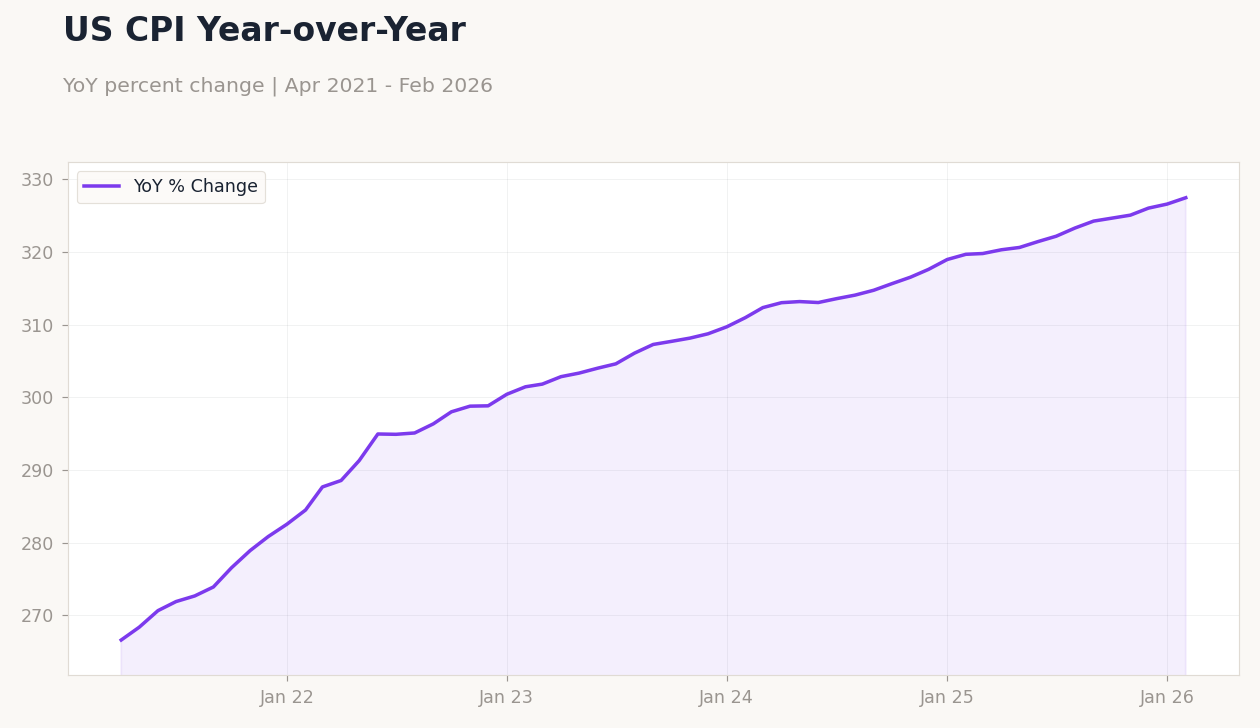

Broader US economic themes center on inflation risks from soaring oil prices due to the Iran conflict, with CPI YoY at 2.31% facing upward pressure that could delay rate cuts. Unemployment stands at 4.40%, supporting a soft landing narrative, but persistent geopolitical tensions threaten consumer spending and business investment. Housing affordability remains strained, as evidenced by upcoming home price data, while corporate debt concerns rise with buy-now-pay-later trends exacerbating financial decisions.