Yesterday's Recap

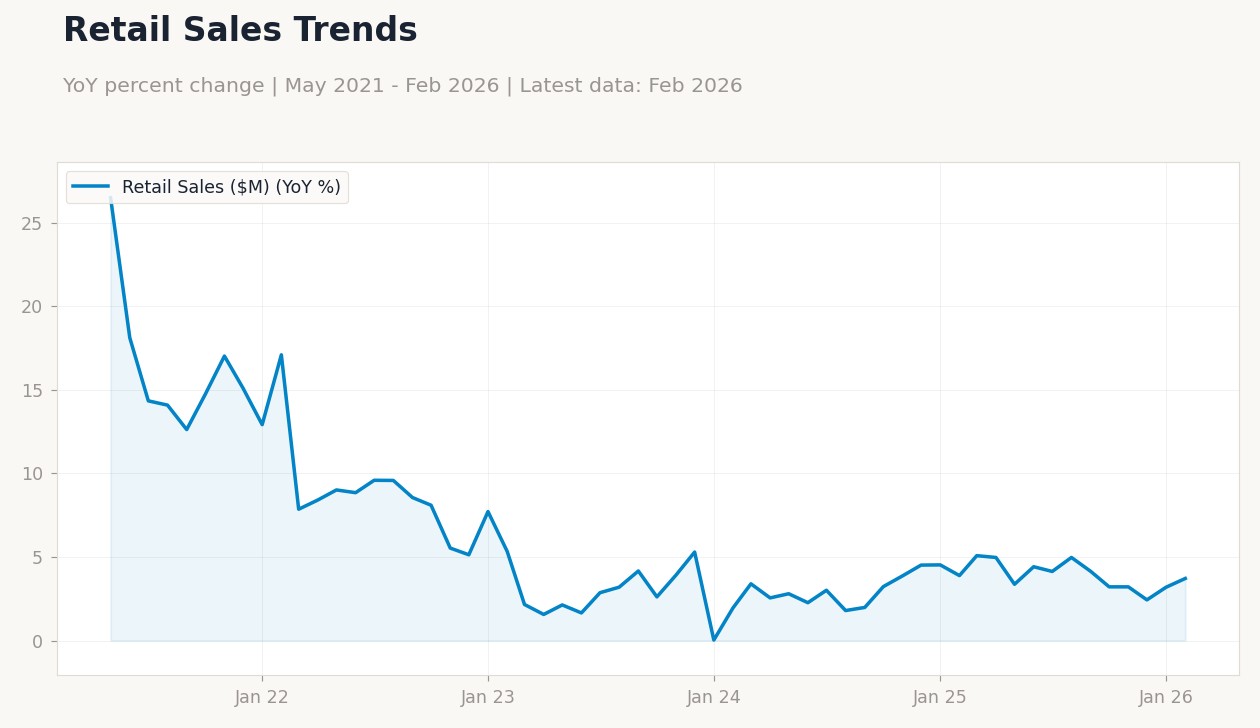

US retail sales advanced 0.6% month-over-month, exceeding the 0.5% consensus and reversing the prior -0.1%, highlighting resilient consumer spending amid elevated oil prices. Retail sales excluding autos rose 0.5% versus 0.3% expected, and the control group climbed 0.5% against 0.3% forecast, bolstering growth outlooks. ADP employment change registered 62,000, beating the 40,000 estimate but below the previous 66,000, suggesting moderated yet positive hiring.

JOLTs job openings totaled 6.882 million, just under the 6.92 million consensus and down from 7.24 million prior, indicating labor market cooling. Chicago PMI dropped to 52.8, missing the 55 expectation and falling from 57.7, signaling softer manufacturing. S&P/Case-Shiller home prices increased 1.2% year-over-year, below the 1.3% forecast and prior 1.4%, as MBA 30-year mortgage rates rose to 6.57% from 6.43%.

Consumer confidence edged up to 91.8 from 91.0. API crude stocks surged to 10.263 million barrels, far above the -1.3 million consensus draw. Equity markets soared: S&P 500 at 6,528.52 (+2.91%), Nasdaq 100 at 23,740.19 (+3.43%), Dow Jones at 46,341.51 (+2.49%), and Russell 2000 at 2,496.37 (+3.41%), driven by energy sector strength.

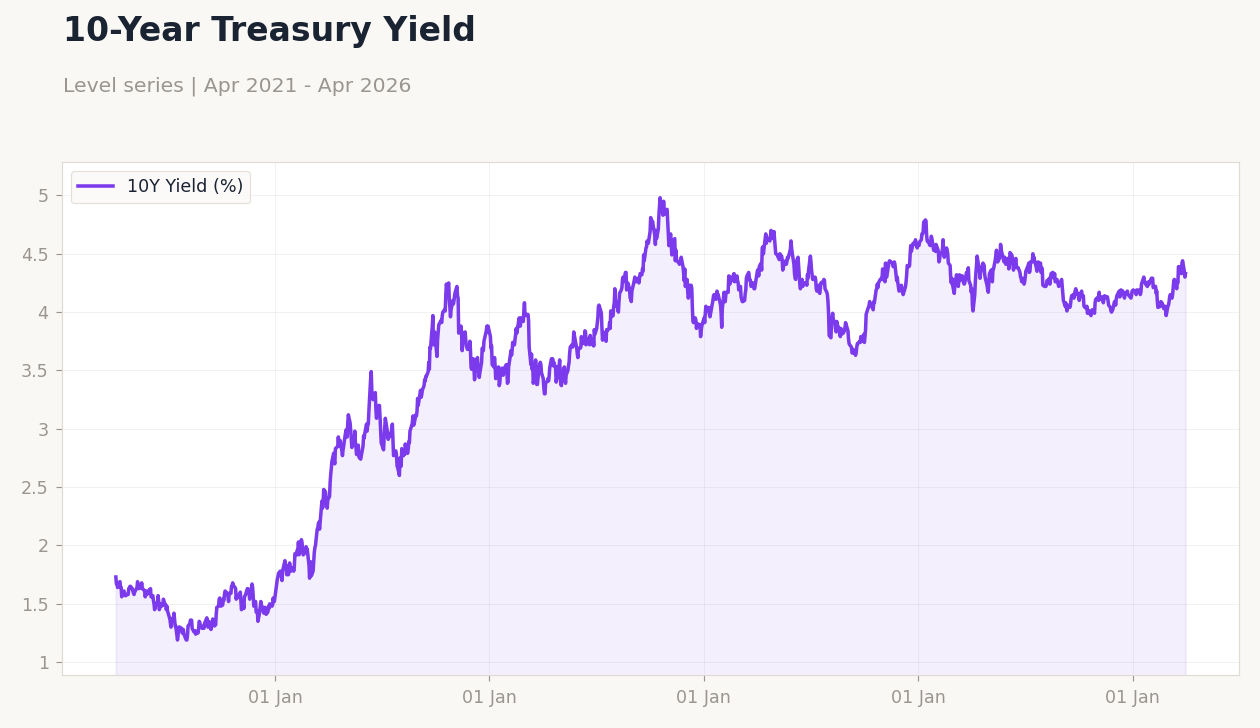

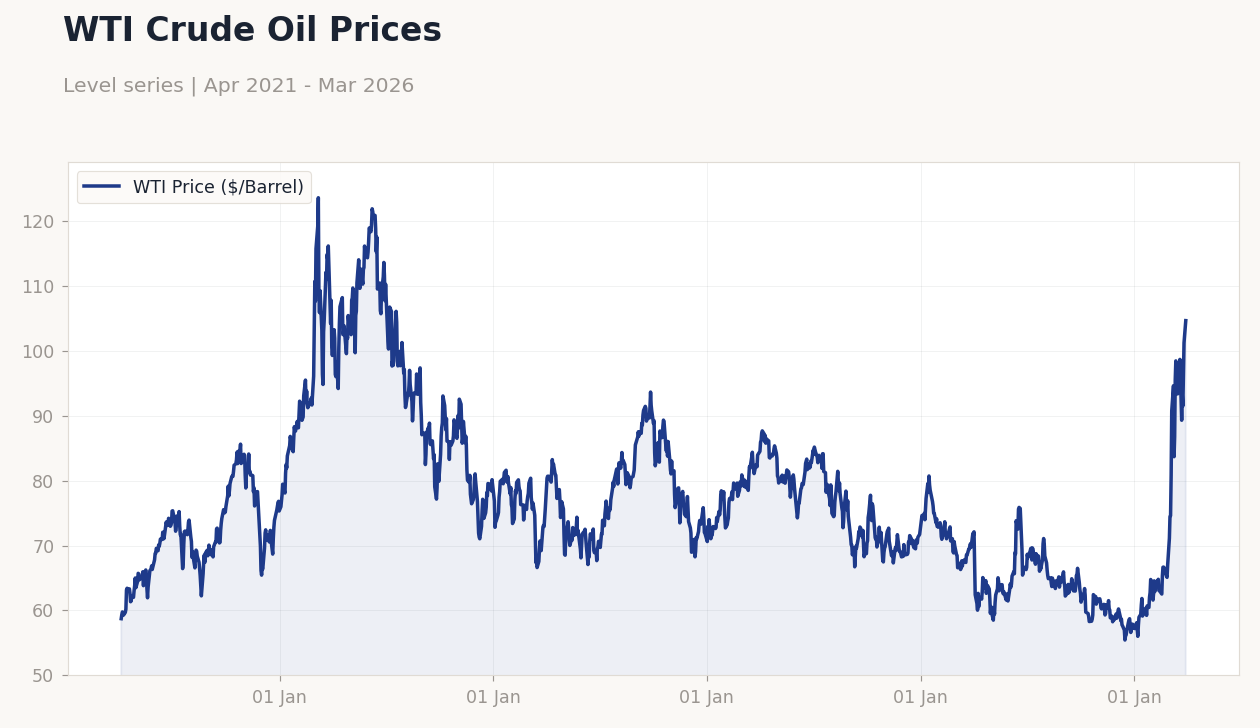

WTI crude jumped to $111.54 (+11.41%) on Middle East tensions. Treasury yields rose: 2-year to 3.81% (+0.53%), 10-year to 4.33% (+0.70%). USD/JPY climbed to 159.59 (+0.57%), while EUR/USD fell to 1.15 (-0.36%) and GBP/USD to 1.32 (-0.51%).

Gold declined to $4,651.50 (-2.75%), and Bitcoin held at $66,872.07 (-0.02%).

The Day Ahead

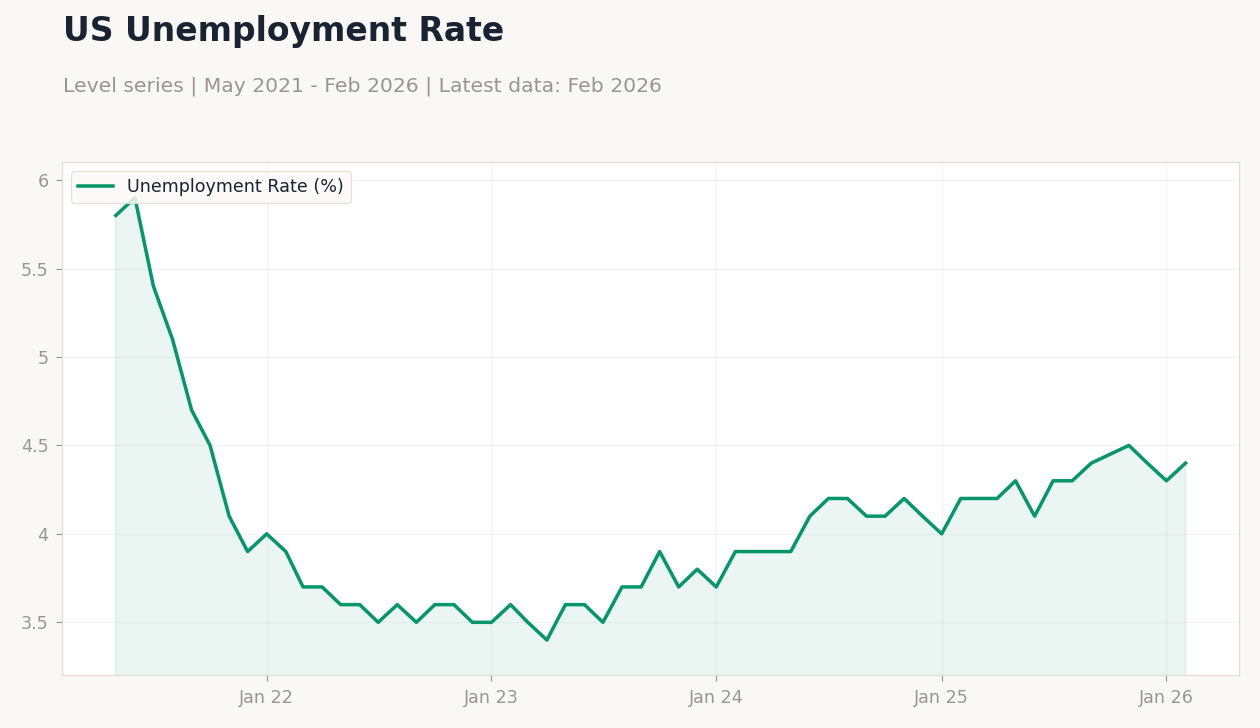

Headline unemployment rate releases at 4:30 ET, with consensus at 4.4% matching the prior, where a steady or lower print could reinforce labor resilience and limit Fed cut bets, while an uptick might fuel dovish repricing and equity volatility. Markets will scrutinize accompanying nonfarm payrolls and wage data for broader employment trends, potentially swaying USD and yields. No other major US data or Fed speeches are slated, shifting focus to geopolitical updates on Iran, which could amplify oil moves and risk sentiment.

Global eyes remain on Middle East developments, including Gulf pipeline talks, for impacts on energy prices and trade flows.

WTI Crude Oil Prices | Type: macro_line | WTI Price ($/Barrel): 104.7 (2026-03-30) | Range: 55.44–123.6 | Trend(6pt): 58.73,111.7,89.68,70.87,101.3,104.7

WTI Crude Oil Prices | Type: macro_line | WTI Price ($/Barrel): 104.7 (2026-03-30) | Range: 55.44–123.6 | Trend(6pt): 58.73,111.7,89.68,70.87,101.3,104.7